Mexico Election Has Global Market Implications

Mexico Election Has Global Market Implications

(Bloomberg Opinion) -- Sunday’s elections for the Mexican presidency and both houses of Congress have the potential to have significant implications for global equities and fixed-income markets. Mexico’s history of turbulence during presidential transitions as well as the peso’s standing as one of the most traded emerging-market currencies should put investors on notice.

Mexico’s announcement in August 1982, a month after the presidential election, that it could not service debt to foreign commercial banks marked the beginning of a decade-long Latin American debt crisis. Capital flight again gathered steam during the presidential transition in the second half of 1994, ending in a massive devaluation of the peso that December. That was also a precursor of the Asian debt crisis in 1997, and of the Russian devaluation and default in 1998.

The risk in this year’s election is heightened by the likelihood of populist candidate Andrés Manuel López Obrador — generally known by the nickname “Amlo,” who is far from the political mainstream — becoming president for the first time in modern Mexican history and achieving a congressional majority.

During the presidential campaign, Amlo hit out against a “rapacious minority” of private-sector executives who oppose his election, while his opponents compared him with the late president Hugo Chávez of Venezuela and suggested that his administration would ruin the Mexican economy. The risk for investors comes from the uncertainty over whether Amlo truly wishes to work with businesses to boost private-sector investment, helping local equities and the peso to rally this month, or has merely softened his edges in recent weeks in order to get elected.

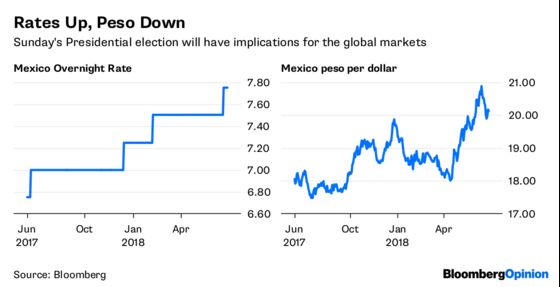

The initial market reaction is likely to be revealed by movements in the peso during the week following elections. Despite the gains this month, the currency has weakened significantly over the past year even in the face of interest-rate increases by the Bank of Mexico. U.S. President Donald Trump’s threat to build a wall on the U.S. southern border and uncertainty about the future of the North American Free Trade Agreement were factors in the peso’s depreciation, investor concerns about an Amlo victory also prompted capital outflows.

There are three developments that investors should monitor in deciding whether the next administration would be favorable for Mexico's financial markets.

First, if Amlo wins and extends an olive branch to private industry groups such as the Mexico Business Council while seeking their support to boost economic growth, expect the peso to appreciate and U.S. equity holders to breathe a sigh of relief. But if victory emboldens Amlo to suggest restricting private investments in the energy sector — a position he has taken in the past — consider that to be a major negative.

Second, a decision to reverse energy reforms would also be negative for foreign direct investment flows that are considered to be sticky and provide long-term stability to a country’s foreign-exchange resources. Mexico has enjoyed sizable FDI flows during the current administration, with an estimated investment of $29.7 billion in 2017, an increase of 11 percent from 2016. A shift to the negative in this variable would remove an important underpinning for investors to achieve attractive returns on their portfolio investments.

Third, while Amlo is expected to be a tougher negotiator with Trump on Nafta than the current Mexican administration has been, investors will judge the new government by its willingness to find common ground with its much larger neighbor to the north. A decision by Mexico to simply walk away from the three-country treaty would be negative for both Mexican and U.S. equities.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

©2018 Bloomberg L.P.