In the Same League as GE? There’s a Silver Lining

In the Same League as GE? There’s a Silver Lining

(Bloomberg Opinion) -- No rational person would put General Electric Co. and Honeywell International Inc. in the same league right now. But Moody's Investors Service Inc. and Standard & Poor's have done just that.

Honeywell and GE have the same credit rating from both firms, the only difference being that Moody's and S&P have a negative outlook on GE and a stable view on Honeywell. This doesn’t make sense. On the one hand, it suggests an excessively lenient attitude toward GE as it attempts to execute its highly uncertain plan to overhaul itself. On the other, it suggests Honeywell has grounds for much more aggressive financial policies, including big deals.

To help illustrate what polar opposites these two companies are right now, here is a quick recap. Honeywell increased its 2018 earnings guidance in April and all of its main businesses are expected to see organic growth and improvements in already high margins. GE's heavily reduced 2018 guidance still looks overly optimistic. It's attempting a breakup whose success depends on favorable markets in a volatile environment, an eventual recovery in its troubled power unit and continued strength in an aviation business that's already running hot. Oh, and GE is pumping $3 billion into GE Capital after previously saying it wouldn't need to.

GE says its plan to spin off its health-care unit and sell its stake in Baker Hughes will help unlock $60 billion in resources that it can draw on to pay down $25 billion of its net debt and pension burden. That was good enough for Moody's, which affirmed GE's credit rating immediately after the portfolio shakeup announcement. This is despite the fact that the very same report straight up says that GE's metrics don't align with its credit rating and won't for a while. S&P at least docked GE for becoming less diversified (a key tenet of past ratings justifications) and said its base case is a one-notch downgrade to A- post-split, but it's unclear why it waited so long.

Now compare that to the ratings firms' attitudes toward Honeywell. In October, after Honeywell's announcement that it would spin off its turbochargers division and consumer-facing building-products business, Moody's cited the "uncertainty" posed by a likely need to replace the profits lost via those moves with acquisitions. It expects the company to find deals that can be financed with only a modest amount of debt, preventing further increase to leverage it viewed then as "relatively high" for the A2 rating level. For the record, Moody's at the time sized Honeywell's leverage at about 2.5. This week it estimated GE was closer to 4.

GE and Moody's speak a different language sometimes. GE finally included its pension deficit in its debt calculations, but it's using net debt, whereas Moody's looks at gross debt. So while Moody's target of a 2.5 debt to Ebitda ratio looks on the surface to be the same as GE's goal for 2020 leverage, in fact they aren’t. JPMorgan Chase & Co. analyst Steve Tusa estimates GE deleveraging targets still imply a gross debt to Ebitda ratio of more than 3.5 in 2020.

Honeywell, by contrast, has always played by the credit-rating firms' rules and definitions. But should the company want to, its treasurer has grounds to push back a bit more, says Bloomberg Intelligence analyst Joel Levington. If GE can get this much of an extension on lowering its leverage, Honeywell should be shown the same amount of patience in the event of a big deal that balloons its debt. Arguably, it deserves more benefit of the doubt as its free-cash-flow generation prospects are clearer and more stable.

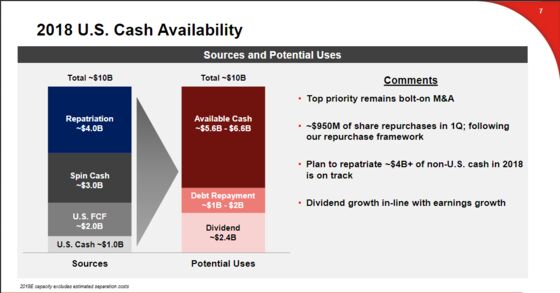

There are signs this is already taking place to some extent. Honeywell in May lowered its debt repayment target for 2018 by $1 billion, effectively shifting more of its $10 billion in 2018 cash sources to the "available" bucket.

The biggest question is whether Honeywell CEO Darius Adamczyk has the appetite for a big deal, and how investors would respond to one. To his credit, Adamczyk is intent on staying disciplined and avoiding overpaying. That said, he will likely need to do something soon to offset the dilution from the spinoffs. Rockwell Automation Inc., a company that has long been speculated as a potential target for Honeywell, recently made a $1 billion investment in industrial Internet-of-Things company PTC Inc. That's raised questions about whether Honeywell would want to make an in-kind software acquisition, where the growth prospects could offset the sting of a pricey multiple.

At least from a credit perspective, Honeywell seems to have more of a green light to think bigger.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.