Loans Could Be the New Flight to Safety

Loans Could Be the New Flight to Safety

(Bloomberg) -- If you’re looking for safe port in a possible oncoming financial storm, forget bonds. Leveraged loans are what you’re looking for.

That’s right, with interest rates and geopolitical risks rising, investors are being driven to floating rate, secured assets as a form of protection amid market volatility. And leveraged loans -- called “dangerous” by some, likened to subprime mortgages by others -- have become a top pick among global credit investors.

“We maintain our position of being overweight high-yield bank loans and CLO tranches relative to high-yield [bonds],” said James Keenan, managing director and co-head of global credit for BlackRock Inc., who oversees $87 billion for the firm.

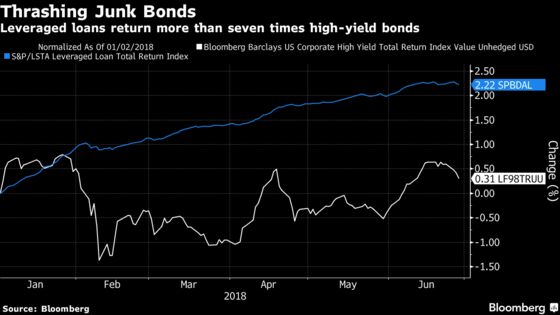

Keenan likes loans because of inflation risk, since junk bonds are susceptible to volatility in growth and earnings. The market seems to agree, as the benchmark S&P/LSTA Leveraged Loan Index has gained 2.2 percent this year, while the Bloomberg Barclays US Corporate High Yield Bond Index has returned just 0.3 percent.

“If you can go from an unsecured piece of paper to a secured piece of paper, or high-yield to bank loans, you should do that,” Keenan said. “Now is the point in the cycle that you want to buy some downside protection.”

“Loans have emerged as an all-weather asset class, providing protection against duration risk in rising rate environments, and structural protections as a senior secured instrument in periods of economic stress,” John Popp, global head and chief investment officer of the Credit Investments Group at Credit Suisse Asset Management, wrote in an email. The division managed $50.3 billion as of March 31.

“Bank loans definitely come out on top in today’s market because of that risk-return,” said Chris Remington, portfolio manager at Eaton Vance. “The rational investor -- he who wants the most return for least risk -- would naturally gravitate towards loans.” Eaton Vance manages $100 billion in fixed income assets, including $45 billion in bank loans and $15 billion in high-yield bonds.

As bond and loan spreads converge, Krishna Memani, chief investment officer at OppenheimerFunds Inc., agrees. "Given where spreads are, the upside in high yield is limited. Given where we are in the cycle, I would rather have seniority," said Memani, whose firm managed $250 billion in assets as of May.

Loan funds have seen $10.9 billion of inflows compared with $31.8 high-yield bond outflows year to date, according to Wells Fargo Securities. In addition, CLOs -- which buy about 60 percent of U.S. leveraged loans --may be on pace for record sales this year.

“CLO demand will continue to be strong in part because the rating-adjusted spreads are still as attractive as anything that people can find out there and it’s a floating rate obligation,” said Rachel Golder, co-head of high yield and bank loans at Goldman Sachs Asset Management, which manages $20 billion in high yield and $7 billion in loans. “People are liking that as there still is a view that rates are likely to go up.”

GSAM has been “constructive on loans” since the fourth quarter of 2017 based on its rates outlook. “We did think interest rates were going to start moving up more rapidly and that’s really the key driver for loans to outperform,” said Golder. “We expect to continue to see that going forward.”

Covenant Concerns

Intense demand for bank loans from CLOs and mutual funds this year has put pressure on the yield spreads and caused more loans to come to market with fewer covenants and other protections for investors. This could be a potential pressure point in the future.

“In the near term, you’re a little bit concerned of yields coming lower and lower,” said Mike Terwilliger, portfolio manager at Resource Liquid Alternatives. “Over the long term, the concern is if we have the next default environment, lack of covenants will potentially limit the potential recovery on those loans.”

Terwilliger said he expects loans to be the preferred asset class through 2018 and into 2019, but the tide could turn. “Now we are not at a point where we are tilting our allocation away from floating into fixed,” he said. “But we are sort of at a point where we are close to the inflection point because of the denigration of returns in the floating-rate market place.”

Terwilliger’s Resource Credit income fund manages $151.5m, of which 75 percent is floating rate and the rest is predominantly high-yield.

To contact the reporter on this story: Shelly Hagan in New York at shagan9@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, ;Christopher DeReza at cdereza1@bloomberg.net, Eric J. Weiner

©2018 Bloomberg L.P.