Good Stress Test Grades Don’t Impress Bank Investors

Good Stress Test Grades Don’t Impress Bank Investors

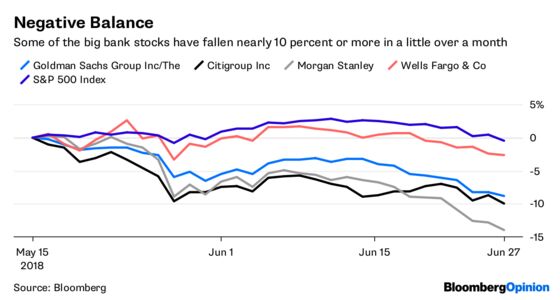

(Bloomberg Opinion) -- Bank investors seem more stressed out than they have been in a while. Shares of the big banks are down an average of 9.3 percent this year, compared with a gain of nearly 1 percent for the S&P 500 Index.

The results last week of the first half of the Federal Reserve’s stress tests, in which every bank passed, haven’t lifted the mood at all. As of Wednesday evening, the S&P 500 Financials Index had fallen 13 consecutive days — the last four since the results came out. The results of the second half of the test, which dictates how much banks can pay out in dividends and spend on buybacks, comes out Thursday afternoon. But don’t expect this round, even if the banks do similarly well, to be any more calming.

The issue has to do with how the bank’s armor themselves against losses and what the stress test measures.

Banks generally have two ways to absorb losses — loan loss reserves, or provisions, and capital. While banks separate the accounts on their financial statements and in regulatory filings, the money in them is really the same. People often think of provisions, and capital, as money the bank has stashed away to cover losses, in a safe somewhere, not to be touched. In reality, nothing is truly put aside; all of that money sloshes around the bank. The big difference has do to with accounting. Banks book provisions as losses and record capital as excess earnings. But the lines can blur. In fact, to not dissuade banks from taking provisions, they can count them toward regulatory capital in some instances.

Nonetheless, the stress tests — indeed the entire post-financial crisis regulatory regime — put a lot of emphasis on capital. There’s a reason for this. Capital is more flexible and can be applied to any of the bank’s losses. Provisions have to designated, not just for loan losses but for the specific types of potentially bad loans they have been set aside to cover.

That emphasis has had its desired effect. Banks have a lot more capital then they did before the financial crisis. Provision accounts, on the other hand, are just as shallow as they were before the crisis. Accounting rules may also limit how much banks can take in provisions.

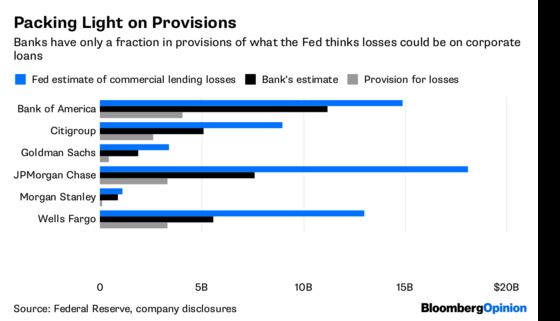

An unintended consequence is that while the stress tests have made the banks safer in general, they may be making their earnings more uncertain for investors. Just look at this year’s stress test. It was, by all accounts, more strenuous than in past years. But overall, six big banks — Bank of America Corp., Citigroup Inc., Goldman Sachs Group Inc. Morgan Stanley and Wells Fargo & Co. — did just as good a job at spotting potential loan losses. The banks’ internal stress tests anticipated 71 percent of the losses that the Fed expected they would have in a severe economic downturn, about the same percentage as last year.

But they disagreed about where the losses would be. The Fed estimated that corporate loans would result in $60 billion in losses, about double the $32 billion that the six banks predicted. The banks were more pessimistic about credit cards, forecasting $62.8 billion in losses compared with the Fed’s $58.7 billion.

This isn’t a problem for capital, but it is for provisions. The big banks have allocated just $13.9 billion of their reserves to cover commercial loan losses, which, again, the Fed has estimated could total nearly $60 billion in a severe recession. That’s a big gap. It’s not a problem for stability because the banks have the resources to cover the gap. But it is a problem for earnings. Once banks drain their provisions for a certain type of loan, or look as if they will, they have to refill the account and take another loss, which reduces profit. They can’t just say, “Well, we set aside more than we needed for credit cards, so we’ll take from that pile.”

Bank stocks are ailing for a lot of reasons. A flattening yield curve is squeezing lending profits. Higher interest rates may quell loan demand. Banks, more than other industries, are tied to the performance of the market, which has been rocky this year. Add to the list the realization that the stress tests, while making the banks less risky, have done little to protect their bottom lines. Passing grades, and higher payouts, can only lower investors’ blood pressure so much.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.