Bond Traders Can Stop Blaming the Banks

Bond Traders Can Stop Blaming the Banks

(Bloomberg Opinion) -- Investment-bank dealers have been painted lately as the villains in some of the biggest bouts of volatility in global markets.

When Italian bond yields spiked last month, traders complained that dealers refused to offer quotes, meaning investors couldn’t exit their positions as losses piled up. A study this month from the U.K.’s Financial Conduct Authority found that during the pound’s flash crash in October 2016, the inter-dealer part of the market “collapsed almost completely,” falling to 2 percent of all transactions from the usual 61 percent. Dealers may have reacted similarly during a brief, sharp rally in Treasuries on June 7.

To some, this is bad behavior on the part of banks. Their role as middlemen between buyers and sellers means they can serve as a buffer during times of panic. If selling is rampant, these dealers can step in as bond buyers, stash the securities in their inventories and then offload them back into the market when things settle down.

But really, why should dealers be the ones taking on substantial risk? Particularly at the precise moment that markets are the most volatile?

After all, the financial crisis, at its core, was an international banking meltdown. That’s why Wall Street now faces strict stress tests from the Federal Reserve that assess how much capital lenders would have left after enduring financial shocks. All 35 banks examined cleared the first hurdle last week, though Thursday’s release of results from the 2018 Comprehensive Capital Analysis and Review will be even more critical.

Asset managers, on the other hand, have no such obligations. And they’re far less important to the underpinnings of the global economy than the world’s biggest banks. As my colleague Matt Levine put it recently: “Prices are always going to move; the point is not to minimize those moves but to build a financial system that is robust to them.” Thus, the stress tests.

Moreover, there’s reason to think that banks’ shrinking corporate-bond holdings are at least in part a statistical mirage. Primary dealer positions in the securities tumbled to about $23 billion as of June 6 from around $265 billion in 2007, according to New York Fed data. But as Sally Bakewell and Vildana Hajric of Bloomberg News reported last week, that’s not exactly a fair comparison. Instead, the consulting firm Tabb Group found the decline was more in the range of 35 percent to 50 percent between 2007 and 2014.

So for those fretting about smaller balance sheets, that’s some relief. Then again, is it really so bad for banks to have leaner bond inventories? Here’s part of Tabb’s findings, summarized by Bloomberg:

What money managers care about is a bank’s capacity to buy securities, and the bigger a dealer’s inventory, the less ability it has to buy more. The average capacity at the six biggest U.S. banks for corporate bond underwriting fell just 16 percent between 2006 and 2017, according to Tabb, and most of the banks can take on even more risk if there’s a valid business reason to do so.

That last part is crucial. It’s not necessarily in banks’ best interest to provide ample bond-market liquidity during times of stress. They simply don’t have the massive balance sheets they once did. And that’s by design.

Bond fund managers, for their part, understand that the risk has effectively been passed on to them. “In today's market, the shock absorber when there is a speed bump or disruption becomes price,” Tony Rodriguez, head of taxable fixed-income at Nuveen Asset Management, said in an interview.

“That should also create opportunity,” he said, which is why Nuveen’s bond portfolios haven’t made any outsized bets lately. “You'll make money over the next 12 to 18 months by being able to respond to the next dislocation.”

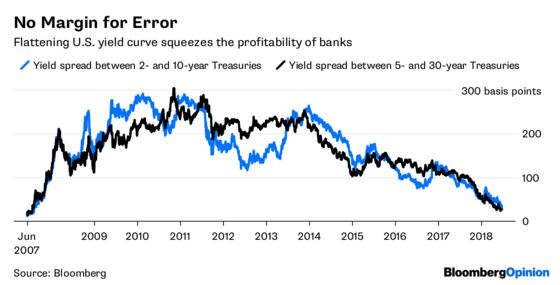

The flattening U.S. yield curve, meanwhile, is squeezing banks’ money-making operations. They prefer it to be steeper because they generate income from the spread between long-dated loans and deposits that are priced on shorter-term rates. With that gap shrinking, the S&P 500 Financials Index suffered its longest losing streak on record. On top of that, the Fed’s CCAR stress tests on Thursday will make or break banks’ plans to return money to shareholders through higher dividends and share buybacks.

Of course, healthier banks don’t necessarily mean much for how bonds will perform in the next crisis. About $9 trillion of U.S. corporate bonds were outstanding at the end of March, an increase of about 85 percent from the end of 2006, according to the Securities Industry and Financial Markets Association.

More debt and fewer buyers willing to step in strikes some as a dangerous combination. JPMorgan Chase & Co. CEO Jamie Dimon called October 2014’s flash rally in Treasuries a “warning shot,” partially blaming regulations that led dealers to step back from making markets.

Still, the 10-year Treasury yield opened at 2.2 percent the day of that 37-basis-point swing. One week later, it closed at 2.22 percent. It’s hard to call that broken. Sure, corporate bond traders may take longer than those dealing in government securities to find their footing. But markets, as they always do, will find an equilibrium.

Maybe that’ll happen because bond dealers assume their traditional shock-absorber role. Or maybe not, and fund managers who get caught in large offsides bets are the ones shouldering substantial losses. Either way, banks are not the bad guys in the bond market’s liquidity story. It’s worth withstanding a flash crash every now and then if it helps prevent another systemic one.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.