Record Canadian Stocks a Blip in Long History of U.S. Domination

Record Canadian Stocks a Blip in Long History of U.S. Domination

(Bloomberg) -- Canadian investors could be forgiven for getting a little excited. The country’s stock market just hit a record, surpassing a January high before its bigger, brasher U.S. cousin.

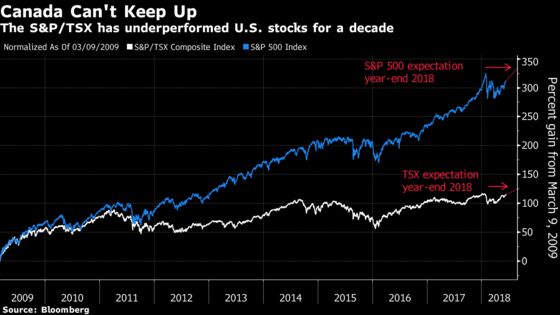

But look at the longer-term picture and there’s less to get fired up about. Since the financial-crisis low of March 9, 2009, the S&P/TSX Composite Index has gained 117 percent compared with an increase of 309 percent for the S&P 500 Index. And Canada is expected to lag again in 2018, with strategists forecasting a full-year gain of about 5 percent versus 10 percent for the S&P 500.

The Canadian index fell 0.2 percent to 16,392.90 at 9:31 a.m. in Toronto.

It’s no secret that Canada’s stock market suffers from a lack of diversification, with too much exposure to cyclical commodity stocks and not enough to growth drivers like technology and health care. But some of the country’s business leaders say the reasons for its long-term underperformance go deeper than that: a lack of risk capital, too few independent investment dealers, and uncompetitive tax policy.

In Canada, it’s not so easy to bring new companies to market.

Nearly 50 independent investment dealers have closed shop in the past five years due to higher operating costs and weak commodity markets, and consolidation will only accelerate over the next several years, said Ian Russell, president of the Investment Industry Association of Canada.

That means fewer options for companies that want to go public, pushing them to other sources of funding like private equity and venture capital, or to acquisitions by larger competitors. Investors are then left with fewer opportunities to diversify into underrepresented, high-growth sectors like technology -- the real standout of U.S. markets.

‘Not Healthy’

There were 14 initial public offerings worth more than $75 million on the Toronto Stock Exchange last year and four so far this year, down from 30 in 2007 when commodities were booming, according to data compiled by Bloomberg.

“There’s a fundamental issue with the lack of people like ourselves to help entrepreneurial companies raise money and to help small-cap IPOs happen,” Dan Daviau, chief executive officer of independent dealer Canaccord Genuity Group Inc., said in an interview at Bloomberg’s Toronto office earlier this year. “That to me is not healthy for the Canadian capital markets. In the U.S. we would have 30 competitors that could do different flavors of what we do.”

Those that are listed have a harder time raising equity capital for acquisitions and growth, keeping stock prices depressed, according to Russell. There have been seven secondary share offerings in Canada worth a total of $756 million year-to-date versus 23 worth $2.2 billion in 2007, according to Bloomberg data.

As the investment dealers have shrunk, the banks have stepped in, but they tend to ignore the smallest companies, Russell said. Canada’s five largest banks accounted for about two-thirds of equity and equity-linked issuances in 2017 compared with less than half in 2008, the data show.

Take the cannabis sector. Canaccord has led equity financings in the industry, which the big banks were loathe to touch. Now that the industry is well established and Canada is legalizing pot for recreational use, the big banks are beginning to elbow in.

Tom Caldwell, chairman of Caldwell Financial Ltd. and CEO of Urbana Corp., is blunt about the implications of Canada’s shrinking pool of independent dealers and the creeping influence of banks.

“They acquire, absorb and obliterate,” Caldwell said. “I think it’s going to have a tremendous impact on job creation, economic growth and innovation.”

Canada’s tax regime also stunts corporate investment through special tax breaks and subsidies that are only available to small businesses, discouraging them from growing past a certain size, said David Rosenberg, chief economist and strategist at Gluskin Sheff & Associates Inc., calling the system “absolutely perverse.” Finance Minister Bill Morneau last year tried to crack down on the use of private corporations, a structure small-business owners frequently use to reduce taxes, but a backlash prompted him to retreat.

“When you have a system in Canada where you reward small, you stay small,” Rosenberg said.

To be sure, the burgeoning marijuana sector has created a new stable of publicly traded companies, which helped lead the S&P/TSX to a record high Wednesday after Canada’s upper house voted to approve the legalization of recreational pot. Canopy Growth Corp. rose 6.7 percent to C$45.36, a record high, giving it a market value of C$9 billion ($6.8 billion).

Canada has also produced some successful, innovative firms like Shopify Inc. In fact, the tech sector, which accounts for just 4 percent of the Canadian benchmark, is leading its peers by a long shot, up 31 percent year-to-date.

Managers Needed

Canada actually ranks fifth out of 54 countries in the Global Entrepreneurship Monitor for perceived opportunities for entrepreneurs -- but it’s not good at turning that innovation into commercial success, said Jos Schmitt, CEO of Aequitas Innovations Inc., which runs a Toronto-based stock exchange.

Schmitt blames a lack of risk capital and too few Canadians with the right managerial and commercialization skills. He suggests making it easier for U.S. broker-dealers to access the Canadian market and providing more support to publicly traded companies. Without that, Canada’s stock market is doomed to continue its underperformance, he said.

“A lack of risk capital either leads companies to go somewhere else -- and that is often the U.S. where they can find the private risk capital, where they can find the talent they need. Or it leads them to go public too quickly,” he said. “Neither of those two solutions is a good one ultimately for our economy.”

--With assistance from Scott Deveau.

To contact the reporter on this story: Kristine Owram in Toronto at kowram@bloomberg.net

To contact the editors responsible for this story: Jacqueline Thorpe at jthorpe23@bloomberg.net, ;Courtney Dentch at cdentch1@bloomberg.net, ;David Scanlan at dscanlan@bloomberg.net, Steven Frank

©2018 Bloomberg L.P.