Four Months of Nothing Give Life to Bond Bulls

Four Months of Nothing Give Life to Bond Bulls

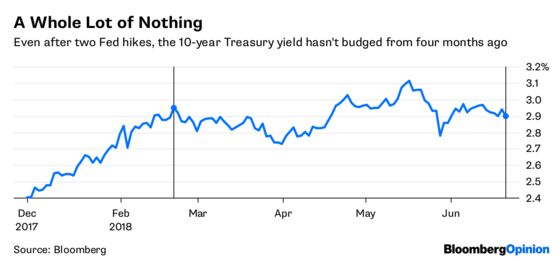

(Bloomberg Opinion) -- Four months ago today, the benchmark 10-year Treasury yield rose to 2.95 percent, the highest level since January 2014. Markets rebounded from that pesky spike in volatility in early February and were looking forward to stronger economic growth, a pickup in inflation and more Federal Reserve rate increases.

U.S. yields, by all indications, were only headed higher. My Bloomberg News colleagues and I rushed to publish a guide overnight for when the 10-year rate reached 3 percent. Traders gobbled it up.

Now here we are, two Fed rate hikes later, with inflation at the highest in 15 months and the labor market as strong as ever — and the 10-year yield is below 2.9 percent.

Sure, you can come up with any number of reasons that make sense out of this. German 10-year yields have been cut in half over the period, to 0.35 percent from 0.7 percent (to the detriment of Bill Gross). In geopolitics, the prospect of a U.S. trade war with China is heating up and euroskeptics are gaining ground in Italy. And as I argued recently, corporate pensions are exerting an invisible force on longer-term yields, keeping them subdued since the end of 2017.

But no matter how you spin it, it’s a victory for bond bulls like Colin Robertson at Northern Trust Asset Management, who told me in an interview this week he’s growing more convinced that 10-year yields have peaked for 2018. And it’s a clear setback for those like JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon and Franklin Templeton’s Michael Hasenstab, who rushed to say the benchmark was headed to 4 percent just weeks after it breached 3 percent.

Calling the top of the yield range, of course, is a tough business. Strategists at BMO Capital Markets said in mid-March that they were “increasingly comfortable with the notion that the 2018 peak of 10- and 30-year yields might have already been established,” referring to the highs of Feb. 21, four months ago. That didn’t happen.

But at that point, global synchronized growth was still the base-case scenario for many investors. The months since then have spurred more calls for divergence, and questions about whether the Fed can really tighten policy alone.

Robertson says there’s a good chance economic growth will be weaker a year from now. That might mean the Fed will have to pause its rate hikes, no matter what the “dot plot” suggests. He acknowledges that his view is contrary to market expectations. And in December, he predicted only one 2018 increase by the central bank. But misjudging the central bank’s path comes with the territory of being bullish on Treasuries when the Fed is tightening at its most aggressive pace in more than a decade.

Still, those bullish instincts have merit. After all, if you bought long bonds four months ago and rode it out, you’d have a tidy profit. The ICE Bank of America 30-year Treasury index has returned 4.2 percent over that span, compared with 1 percent for both the broad Treasury market and U.S. high-yield bonds. Corporate debt has lost 0.6 percent. The S&P 500 Index is up 2.5 percent.

Again, it’s easy for anyone to see peaks in hindsight and difficult to call them in the moment. But maybe it’s a bit clearer now, with the Fed firmly in the middle of its tightening cycle and the European Central Bank spelling out its plans for the next year. And even during a trade spat, China isn’t doing anything rash with its Treasury holdings in an attempt to spike U.S. borrowing costs.

Whether the buying opportunity for 10-year Treasuries is at 3 percent, 3.12 percent or 3.25 percent is up for debate. But one thing bond traders can largely agree on, based on the past few months: A move to 4 percent is going to require a Herculean effort.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.