Goldilocks of the Bond Market Loses the Sweet Spot

Goldilocks of the Bond Market Loses the Sweet Spot

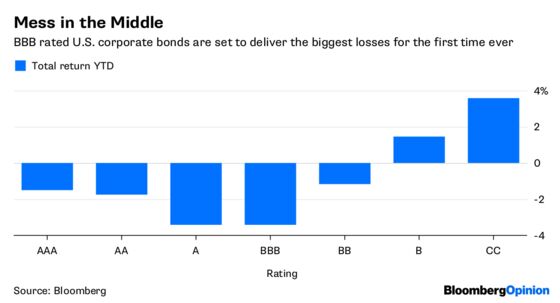

(Bloomberg Opinion) -- For the first time in at least the past quarter-century, bonds with the lowest investment grades have delivered the biggest losses in the U.S. corporate debt market.

Intuitively, this shouldn’t make sense to bond traders. Fixed-income returns hinge primarily on interest-rate risk and default risk. When the economy is on the mend or the Federal Reserve is raising rates (2017, 2016, 2009 and 2004, for instance), top-ranked debt underperforms. When the economy is in a downturn or cracks emerge in key industries (like 2015, 2008, 2007 and 2000), defaults spike and junk-rated companies deliver large losses.

Corporate bonds rated in the BBB tier by S&P Global Ratings and Fitch Ratings, or the Baa range by Moody’s Investors Service, by contrast, have traditionally been a Goldilocks of sorts. They’ve delivered an annualized return of 5.9 percent over the past 20 years, better than the 4.4 percent earned on AAA debt and the 5.7 percent gain on CCC securities, Bloomberg Barclays data show.

So for those who haven’t been paying attention, it may be surprising that the same debt that for decades has been “just right” for investors is suddenly all wrong. What’s more, it’s unlikely to get better anytime soon.

The amount of BBB debt outstanding has ballooned to $3.3 trillion as years of rock-bottom interest rates encouraged companies to take on leverage, whether to finance an acquisition or simply buy back their stock. And these highly indebted companies are largely household names: Just today, you may very well drive a Ford Motor Co. car past a CVS Health Corp. store, a McDonald’s Corp. restaurant or a Starbucks Corp. coffee shop. Perhaps your mobile phone carrier is AT&T Inc. or Verizon Communications Inc. Maybe your kitchen is stocked with products from Kraft Heinz Foods Co. purchased at Kroger Co.

Being rated BBB, of course, isn’t by definition bad. After all, it’s still an investment grade. And debt-financed acquisitions or share buybacks may very well have represented prudent corporate governance at the time.

But the growing fear among investors is that the bond market is fast approaching a tipping point. The 3.4 percent loss this year for BBB debt, the worst since 2008, reflects that angst. And it points to a worst-case scenario: that some of these companies, as big and broad as they may be, might falter under the weight of their debt burdens when the next recession rolls around. Because they’ve pushed themselves all the way to the brink of investment grade, how they handle hard times could prove to be a make-or-break moment.

Strategists at Citigroup Inc. (which, incidentally, is also rated in the BBB tier) published a report Tuesday that recommends “how to position for a correction” in the lowest investment-grade debt. They suggest a trade that involves buying protection on the 10 companies that the market is already punishing the most severely and the 10 that have been the most resilient. That will pay off if losses intensify.

“The widest names will provide immediate protection as the market begins to sell off, while the tightest names will underperform if the sell-off reaches significant ‘systemic’ proportions,’’ Anindya Basu and Calvin Vinitwatanakhun wrote.

It would be one thing if Citigroup were alone in warning of big losses. But earlier this month, KKR & Co.’s Jamie Weinstein, global co-head of special situation investing, also predicted that the “big explosion” of BBB corporate debt market might be sowing the seeds of the next crisis.

So far, investors aren’t rushing for the exits. The much-ballyhooed jumbo bond sale from Bayer AG, which my colleague Marcus Ashworth chronicled, not only came and went without much market disruption, but the spread on its longest dollar-denominated maturities narrowed from initial price talk. S&P cut Bayer two notches to BBB because of raised leverage to complete the $63 billion acquisition of Monsanto Co. Moody's lowered its grade one notch to Baa1.

AT&T is next in line: It will most likely need to return to the bond market to help finance its purchase of Time Warner Inc. The acquisition was delayed, triggering a clause from when it sold $22.5 billion of bonds almost a year ago that mandated a debt buyback. But, as Bloomberg News’s Molly Smith reported last week, it may not have to come with a blockbuster deal all at once.

That may make the bonds easier to take down, but it doesn’t address the overarching issue that there’s simply too much BBB debt out there. If it’s not interest-rate risk or default risk that’s battering the securities’ performance this year, then maybe it’s downgrade risk.

If even a fraction of the BBB debt drops below investment grade, with the company becoming a “fallen angel,” can high-yield investors handle it? The Bloomberg Barclays U.S. Corporate High-Yield Index is $1.28 trillion in size, sure, but that overstates things. The two largest exchange-traded funds for the asset class (tickers HYG and JNK) oversee $25 billion combined. That’s less than what’s owed individually by several of those aforementioned household names.

Now, it’s almost inconceivable that such a wide swath of industry leaders would falter, even in a weaker economy. And certainly, some companies rated BB could turn into “rising stars” with an upgrade or two as the expansion continues. But as investors were reminded just this week when General Electric was dropped from the Dow Jones Industrial Average, prospects can dim for even the biggest companies. As my colleague Brooke Sutherland wrote, earnings disappointments and poor capital-allocation decisions put the conglomerate in jeopardy.

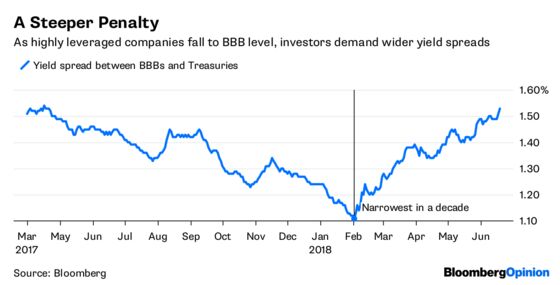

With so many questions, there are few reasons to expect BBB debt performance to get any better. It’s not that investors are shunning risk altogether, because U.S. corporate bonds rated several steps below investment grade have delivered some of the best returns across global debt markets. No, this is specifically a rejection of the leveraged behemoths that for years have received a free pass to borrow. The BBB index yields 1.53 percentage point more than benchmark Treasuries, the highest in 14 months. Just in February, it touched a decade low of 1.11 percentage points.

It’s ugly right now for BBB corporate bonds. But if the bond markets work like they’re supposed to, the penalties now may prevent even steeper losses in the future.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.