Rewriting the Rules of M&A

Rewriting the Rules of M&A

(Bloomberg Opinion) -- The CEO of Europe's biggest insurer is up for a big deal. He just doesn't want Allianz SE to pay for it. Oliver Baete is going to find it hard to have his cake and eat it.

Three years into the job, and things are going well for him: Allianz reckons it has surplus capital and the shares have outperformed their peers despite a recent wobble. But Europe's insurance market is only growing slowly, and the group is keen to boost its general insurance business, which is less capital intensive than life and savings. A deal would put some of Allianz's surplus cash to work, generate savings and re-shape the group.

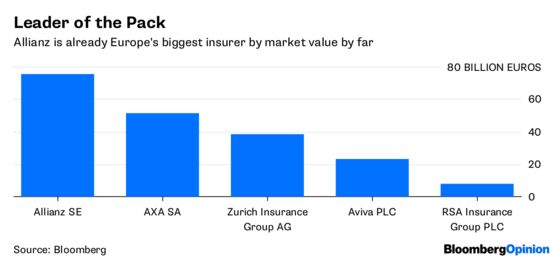

Baete has long-list of potential targets, including Zurich Insurance Group AG, Aviva Plc and RSA Insurance Group Plc, Bloomberg News reported last week.

A small deal wouldn't make much difference to Allianz, which has a market value of 76 billion euros ($87 billion). But big deals mean large premiums. The standard top-up of 30 percent on a 5 billion-euro takeover would cost 1.5 billion euros. For a company the size of, say, Zurich, the equivalent would be 13 billion euros. Axa SA agreed to pay a 57 percent premium for XL Group Ltd. in March — and its shareholders are livid.

Faced with this dilemma, Baete recently floated the idea of a merger of equals in an interview with the Financial Times. But this would need a target willing to play the junior partner and agree to a combination at prevailing market values with no premium.

There would be synergies for sure — cost savings from slashing duplicate functions plus a capital benefit from diversification. Scale is also advantageous at a time when the industry is spending on technology like car sensors and apps that cut out brokers. Better, so the argument goes, for two firms to share the burden of investment than replicate it on identical projects.

Set against this is the higher than average disruption in financial services deals. Trustbusters could force disposals, shrinking the deal and its benefits. Arguing for a "European champion" to see off the Chinese bogeyman isn't going to cut it, not yet at least. Axa and Allianz aren't facing the same competitive pressures as, say, Alstom SA and Siemens AG.

For these reasons, targets will want a decent premium and buyers like Allianz will be wary of paying it. Zurich's management has argued that the digitization of insurance means absolute size is no longer a benefit, although scale helps locally. A deal would dilute its very Swiss identity, making it a tough sell politically.

Aviva's 20 billion-pound ($27 billion) market value means a takeover premium would be affordable. What's more, the company is cheap, trading at only nine times next year's estimated earnings. But its business mix wouldn't do much to tilt Allianz away from life and pensions — unless Allianz could find a specialist life company willing to take that part off its hands.

RSA, worth 6.8 billion pounds, has no life business but its shares are already baking in a takeover premium. Allianz would still have to pay something more on top.

Baete can't rewrite the rules of M&A. If he wants a deal and the target doesn't, he's going to have dangle a proper takeover premium. That applies to transactions big and small. Otherwise he could do worse than grow Allianz by improving its valuation, and letting shareholders find a use for his surplus capital.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.