Rush Into Hot CLO Market Leaves Latecomers Fighting for Scraps

Rush Into Hot CLO Market Leaves Latecomers Fighting for Scraps

(Bloomberg) -- The feeding frenzy sparked by the need for protection against rising interest rates is forcing a flood of firms in the U.S. market for bundled corporate loans to fight over scraps.

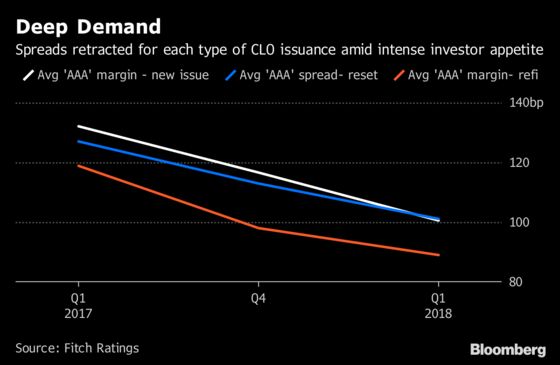

Demand is so strong in Wall Street’s hottest debt market that the number of managers doing business there jumped by about 20 percent last year and continues to increase. And while the market itself may be on pace for record sales this year, the throng clamoring for collateralized loan obligations is rising faster, enticing issuers to weaken terms to an extent that some say doesn’t compensate investors enough for the risk. But so far, there’s plenty of takers.

“One of the risks is market exuberance with everyone chasing the same collateral,” said Peter Sallerson, a senior director at Moody’s Analytics Inc. “Credit terms are getting weaker than some think they should be.”

With underwriting standards eroding amid the brisk demand, managers have been forced to reach for smaller and less liquid loans to get higher spreads, according to Maggie Wang, head of U.S. CLO research at Citigroup Inc.

“Everyone wants to get the best loans, and there’s only so much of them,” Wang said.

One example is the changing loan covenants, which are agreements between the issuers and borrowers that permit or restrict certain activities. This risk can get passed on to investors.

“In a nut shell, deals are coming with lower coupons and less structural and document protections than we would like to see,” said Gretchen Lam, a portfolio manager at Octagon Credit Investors LLC. “That is something we continue to be challenged with as a buy-side community.”

New CLO deals may be on pace to reach an all-time high of $150 billion this year, according to Wells Fargo & Co. New issuance increased 65 percent in 2017 from a year earlier, while refinancings and resets, which renew the coupon and the terms on an issue, reached $166 billion last year, data compiled by Bloomberg show.

A recent rule change has boosted supply. An appeals court ruled in February that firms no longer need to keep a percentage of the securities they sell, setting free a wave of assets into the market. As a result, more managers entered the market because the end of risk retention made it cheaper and easier to put together CLOs.

While the volume of deals has increased, so has the number of managers. Sixteen firms, 12 of whom are new, entered the sector, raising the total to 99 at the end of last year, Wells Fargo said. Four have made debuts so far this year: CarVal Investors, Kayne Anderson Capital Advisors, Partners Group and Post Advisory Group.

But calling these CLO managers “new” might be a stretch. Some of the firms have deep roots in the credit market and others have poached industry veterans to lead new departments. The market is also seeing former players reemerge. For instance, PPM America came back to the market on Friday for the first time since 2007.

“Toward the later innings of a cycle, this is not surprising that you see this given the supply and demand dynamics,” Chris Mawn, head of CarVal’s corporate loan business who was hired last year from CLO firm Highland Capital, said in reference to the looser underwriting standards. “You just have to be all the more diligent in picking your spots and where you want to take risk.”

But few in the market are panicking. Many managers have baked in more protections in CLOs than during the financial crisis, when they performed well. The credit quality of issuers whose loans are in CLOs remained relatively stable during the first quarter, though defaults increased, according to S&P Global Ratings. The default rate for junk-rated corporate debt rose to 3.3 percent in March from 3.1 percent at the end of last year, the firm said in a note.

Even still, the economy and credit market will shift at some point -- a majority of analysts polled by Bloomberg see a slowdown over the next two years -- and CLO investors may now be more exposed than in the past.

“This is a natural progression through a credit cycle where spreads are so tight and so focused on floating rate assets,” Berkin Kologlu, a portfolio manager at Angel Oak Capital Advisors, said. “There’s not a whole lot you can do in fixed income.”

--With assistance from Adam Tempkin.

To contact the reporter on this story: Shelly Hagan in New York at shagan9@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Randall Jensen, Dave Liedtka

©2018 Bloomberg L.P.