These Shiny Economic Numbers May Be a Mirage

These Shiny Economic Numbers May Be a Mirage

(Bloomberg Opinion) -- Friday was another strong day for U.S. economic data, with the unemployment rate falling to a new generational low. But hidden in another dataset from Friday, the widely followed Institute for Supply Management manufacturing report, is some evidence that economic bottlenecks may be producing quirks in the data, which will result in sunny reports in the second quarter but some unwelcome effects a couple months later as those bottlenecks clear. We may realize in retrospect that what looked like strong productivity growth in the second quarter actually was an early indication of inflation.

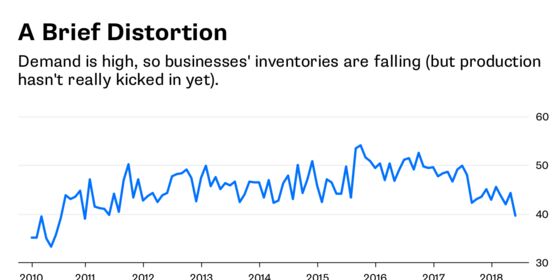

That manufacturing report indicated customer inventories were at 39.6, well below a reading of 50 that indicates a balanced reading. That was the lowest level for the indicator since December 2010. At the same time, readings for new orders and prices paid were both very high, indicating strong demand and high costs for materials that go into the production of manufactured goods.

The ISM noted in its summary of the report that inventory reductions were “likely caused by supplier performance issues" and "lead-time extensions, steel and aluminum disruptions, supplier labor issues, and transportation difficulties continue."

Strong reports on the employment front, construction spending, and the aforementioned ISM report led the Atlanta Fed to revise up its "nowcast" for second-quarter real gross domestic product growth to 4.8 percent, which would represent the fastest pace of growth since the third quarter of 2014. While there are limitations with any growth forecast and there's still plenty of economic data to come in the quarter, this would seem to imply a rapid pickup in productivity growth in the second quarter as well.

But there are reasons to doubt this implication. Look back at that customer inventories line item in the ISM report. As the great recession was ending in 2009, productivity growth was extremely high, peaking at a whopping 8 percent in the second quarter of 2009. As recessions end, there's a glut of inventory, and until companies sell it off, they choose not to pay to restock their companies. For a brief period the economy is selling more than it's producing as it works down inventories, which is great for corporate profits and revenues, but doesn't lead to much hiring demand or inflationary pressures. Mechanically, this shows up in the data as strong productivity growth, but it's not sustainable. Eventually, production and sales come back in balance as businesses restock.

For very different reasons there's a similar inventory dynamic going on today. For ingrained psychological reasons, it's still very difficult for companies to get consumers to pay higher prices for things, as consumer goods companies can attest. At the same time, it's getting more expensive for companies to produce things, because of labor shortages, higher energy prices, tariff fears and freight shortages. Even for those willing to pay, suppliers are struggling to keep up. The result is that companies are selling down the inventories they have in stock, many of which they might have bought at cheaper prices over the past few years, while delaying purchases of higher-cost products they may be unable or unwilling to buy, and deferring the pricing conversation with customers.

But this isn't sustainable. For a few months it may look like a utopian economic environment, with consumer inflation still not yet a concern, high profits as companies sell down their inventories without paying to stock up and a mirage of faster productivity growth.

However, before long, those inventories are going to need to be rebuilt. And from everything we're seeing in the economy, it's going to take much higher prices to do that production. This is likely to be the moment of truth for corporate America: Will they finally be able to pass those higher prices on in a meaningful way to consumers, providing an inflationary jolt to the economy? If not, profits and overall economic growth will suffer when this bottleneck ends.

To contact the editor responsible for this story: Philip Gray at philipgray@bloomberg.net

©2018 Bloomberg L.P.