Ulta Beauty Is Looking Blemish-Free

Ulta Beauty Is Looking Blemish-Free

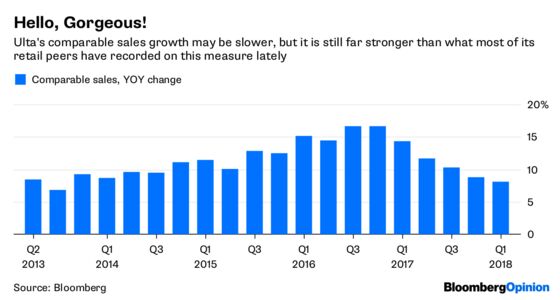

(Bloomberg Opinion) -- Ulta Beauty Inc. has slowed down a little. But don't get the wrong idea: The cosmetics chain is still a front-runner in retailer.

Ulta reported late Thursday that its comparable sales rose 8.1 percent in the first quarter from a year earlier. The increase was driven by all the right things: A booming 48 percent increase in digital sales, as well as 5.1 percent growth in transactions and a 3 percent increase in average ticket.

Investors puzzlingly sent shares down after the report, even though the results beat estimates by almost every measure, and the company raised its full-year earnings guidance. The truth is, Ulta's beauty is way more than skin-deep, and I see no reason that won't continue to be the case for the foreseeable future.

The chain has been adding stores at a breakneck pace, with its fleet now roughly double what it was five years ago. That might sound short-sighted as more spending migrates online, but Ulta has proven the expansion is perfectly justified. Michael Goldsmith, an analyst with UBS, estimates that Ulta's in-store sales per store have grown steadily even as it has added hundreds of locations. In other words, it apparently isn’t cannibalizing its sales; rather, it’s taking market share in a hot category. And he expects this pattern to keep up for the next several years:

Meanwhile, the ranks of Ulta's loyalty program grew to 27.8 million members at the end of last year, an impressive 19 percent increase over the previous year. This program should allow Ulta to wring more visits and dollars out of customers who already dabble at the chain. And the loyalty program is a powerful platform for dispensing targeted, personalized offers – surely a more sustainable business model than relying heavily on storewide discounts and promotions.

You may be tempted to think that Amazon.com poses a serious threat to Ulta. After all, once you like a certain kind of shampoo, why not just order it via Subscribe & Save?

But that misunderstands who Ulta's most important customer is. CEO Mary Dillon likes to say her company is chasing after the "beauty enthusiast," meaning someone who likes to keep up with skincare and makeup trends, someone who shops for these products for the fun and the sport of it. That experiential, sensory shopping experience just isn’t what Amazon does best.

Plus, even if a beauty enthusiast does go digital, Ulta offers a distinctive e-commerce assortment. Goldsmith, the UBS analyst, found that many of Ulta's top-selling online products aren’t available at rival retailers. For example, Amazon and Walmart.com did not directly sell any of Ulta's 25 best-selling makeup items. They did have many of the products for sale via third-party sellers, but he found that make-up prices from such sellers tend to be higher on those sites for this product category.

To be clear, Ulta cannot let itself be lulled into thinking it will simply skate to strong results for the next several years. As Seema Shah, a consumer analyst with Bloomberg Intelligence, points out, lots of retailers are fighting harder to get a piece of the beauty business right now, including J.C. Penney Co. with its Sephora shop-in-shops and Macy’s Inc. with its Bluemercury chain.

But Ulta is well-positioned to keep on taking market share.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

©2018 Bloomberg L.P.