A $431 Billion Fund Says Time to Take Profit on Italy Shorts

A $431 Billion Fund Says Time to Take Profits on Italian Shorts

(Bloomberg) -- The Italian market selloff has been quick, brutal -- and now likely gone too far.

That’s the view of Californian bond giant Western Asset Management Co., which has begun taking profits in short positions in Italian debt, forecasting yields to stabilize once the political turmoil roiling Europe’s fourth-biggest economy subsides.

“Ultimately we think Italy stays in the club, yields will settle down at a more reasonable level, but one that reflects ongoing political risk premium,” said Gordon Brown, London-based co-head of global portfolios at the firm which manages $431 billion in assets. “This is a very dysfunctional market, with terrible liquidity and one that is reacting to a perceived systemic shock which we ultimately don’t think will materialize.”

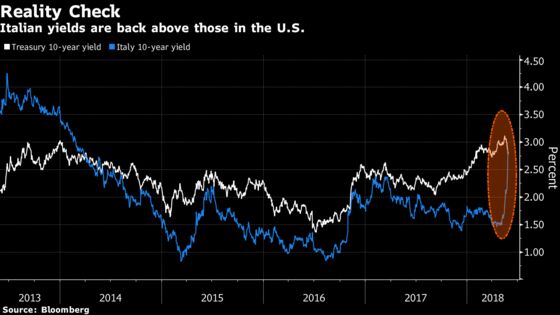

Yields on Italy’s 10-year bond fell 14 basis points to 3 percent on Wednesday. They had skyrocketed about 70 basis points in the first two days of the week as political parties failed to form a government and a fresh election looms. The rout has sparked comparisons to the 2012 debt crisis when Greece teetered on the brink of bankruptcy and the European Central Bank said it would do anything it takes to support the currency union.

Western Asset started taking overweight positions in Italian debt in 2012 after ECB President Mario Draghi declared his commitment to prop up the common currency, said Brown, who helps oversee $23 billion in assets.

However, the firm started shorting Italian bonds last week and has “benefited from the carnage.” While Western Asset remains underweight the nation’s securities, it started trimming some of its positions on Tuesday, Brown said.

Investors have been dumping Italian debt over concerns of anti-EU, nationalist parties in the Southern European country turning a repeat election into a de-facto referendum on membership of the euro.

Euro Positions

“It’s one of the sharpest sell-offs I’ve ever seen,” said Brown, in a briefing in Sydney.

As a result of the turmoil, Western have also closed their long positions on the euro, “tempering” their previous “enthusiasm” for the common currency, Brown said.

In times of stress in peripheral Europe, investors take money out of euro assets and tend to hedge their exit, putting downward pressure on the currency, he added.

Below are excerpts on some of Brown’s other views:

Front-end of Treasuries:

- Sees U.S. economic growth tracking between 2 percent and 2.5 percent

- Doesn’t believe inflation pressures are going to pick up that sharply, therefore doesn’t think the Federal Reserve needs to be very aggressive in normalizing policy

- Western Asset is overweight Treasuries, and has been shifting exposure from longer-dated maturities toward the five-year part of the curve

- 10-year Treasury yields should trend sideways for rest of 2018

Euro View:

- Been very constructive on the euro for the past year or so, recognizing that European growth is picking up and that ECB policy normalization is on the near-term horizon

- Longer term believes the euro will appreciate against the dollar, potentially it could get back above $1.20

Picks in EM:

- Favors currencies of Russia, Indonesia, India, South Africa, and Mexico; thinks longer term they are undervalued

- Likes EM fundamentals, though there are some “challenged stories,” such as Turkey and Argentina. EM weakness has been driven by much stronger U.S. growth, higher Treasury yields, a stronger dollar

- Says Indonesian real rates are quite attractive

--With assistance from Garfield Reynolds.

To contact the reporters on this story: Ruth Carson in Sydney at rliew6@bloomberg.net;Andreea Papuc in Sydney at apapuc1@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2018 Bloomberg L.P.