Goldman Says Riskiest Junk Bonds Are Most `Mispriced' Since 2007

Goldman Says Riskiest Junk Bonds Are Most `Mispriced' Since 2007

(Bloomberg) -- The C-C-Craze for some of the riskiest corporate credits has gone too far, according to Goldman Sachs Group Inc.

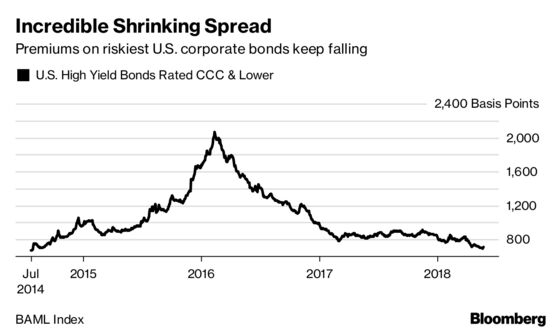

While U.S. investment-grade bonds that are most sensitive to moves in borrowing costs have been hit hard this year, investors continue to pile into debt sold by some of the weakest junk-rated companies. Bonds in the CCC category -- just two notches above default -- have returned a whopping 330 basis points in total this year, according to Bloomberg index data.

That outperformance has helped push spreads on the Bank of America Merrill Lynch gauge of CCC rated debt to below 700 basis points earlier this week -- the smallest premium since July 2014.

Meanwhile, Goldman’s preferred valuation measure of corporate credit, which subtracts their projected expected-loss rates from current spreads, shows U.S. high-yield obligations are now mispriced for even the most benign scenarios.

"In a nutshell, the CRP is the expected excess return on a buy-and-hold strategy of diversified credit portfolios over a five-year period," write Goldman analysts led by Chief Credit Strategist Lotif Karoui in a note. "Put differently, the CRP is the extra premium earned by investors as compensation for future default losses."

Goldman estimates the credit-risk premium for CCC obligations has sunk to a negative 53 basis points, "even under a fairly optimistic assumption of no recession for the next five years."

That’s the lowest level since before the financial crisis, when the CRP touched negative 420 basis points in June 2007, at the height of the froth in the global debt market. It suggests investors are likely accepting credit risk without adequate compensation.

"The key takeaway: the premium currently embedded in high-yield spreads is mispriced even if default losses do not ratchet up to recession-like levels," the analysts conclude "Aside from energy, we continue to see little value in CCC-rated bonds at current levels."

To contact the reporters on this story: Tracy Alloway in Abu Dhabi at talloway@bloomberg.net;Cecile Gutscher in London at cgutscher@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma

©2018 Bloomberg L.P.