`Unprecedented' Reliance on Housing Fuels Canada Recession Call

`Unprecedented' Reliance on Housing Fuels Canada Recession Call

(Bloomberg) -- This recession call is coming from inside the house.

The Bank of Canada has highlighted elevated household debt and imbalances within the nation’s real estate market as the two chief vulnerabilities to the financial system in the event of a recession.

But what could trigger such a downturn? Macquarie Capital Markets offers one simple answer: the housing market itself -- highlighting that the share of employment tied to construction as well as finance, insurance and real estate is nearly two standard deviations above its long-term average.

Tighter mortgage rules and higher interest rates have weighed on activity in formerly high-flying Canadian housing markets, with home sales in Toronto having their worst start to the year since 2009.

“For downside risks to be realized, however, any potential housing-related weakness must spill over into the labor market,” analyst David Doyle wrote in a note to clients Thursday. “While rising rates put pressure on consumer finances, job losses trigger defaults and a tightening in credit conditions that can lead to more severe economic outcomes.”

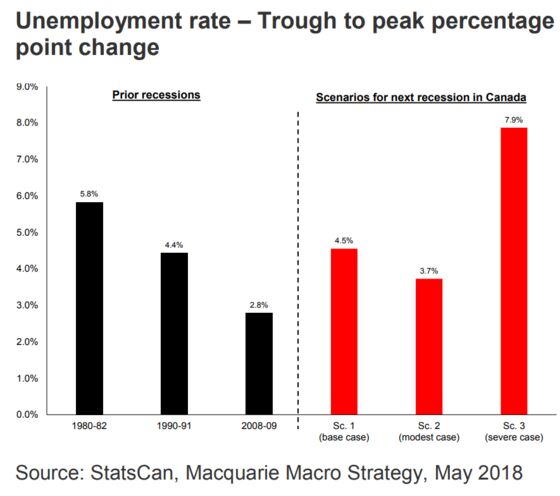

Roughly half of all economic weakness during recessions since World War II is tied to fluctuations in residential investment, he calculates, and the extent to which Canadian output and employment are currently reliant on this is “unprecedented.”

Macquaire’s best-case scenario is that the fallout, starting in 2020, will be as bad for Canada as the 2008-09 financial crisis. Worst case: The unemployment rate will spike by more than any recession since the Great Depression.

In terms of employment concentration in housing-linked industries, this dependency is particularly pronounced in Ontario and British Columbia but still prevalent across the rest of the country. Job growth in these sectors has come amid shrinking payrolls in other cyclical areas like manufacturing, making “housing an all the more important driver of the Canadian business cycle,” Doyle said.

The strength in housing starts and consumer spending, however, suggest only a “modest” risk of a housing-led recession in the nearer-term, according to the analyst.

Macquarie sees the U.S. dollar rising to C$1.36 relative to its Canadian counterpart by the end of 2019. Housing-related risks inform the bank’s stance to overweight outward-facing segments of the S&P/TSX Composite (like energy, technology and industrials) while underweighting areas with immense domestic ties (banks, consumer and telecom).

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Andrew Dunn, Brendan Walsh

©2018 Bloomberg L.P.