Turkey's Island of Market Calm Is a Mirage

Turkey's Island of Market Calm Is a Mirage

(Bloomberg Opinion) -- It's hard to see anything positive behind the plunge in the Turkish lira. But there is one glimmer of light in the banking sector – the foreign loan market is still functional.

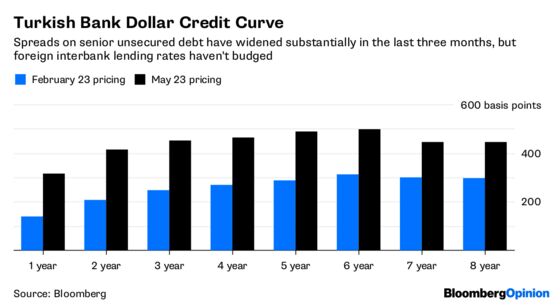

Earlier this week the major Turkish banks rolled over one-year dollar loan funding from foreign banks at a spread of around 130 basis points over Libor. This premium is unchanged from a week, a month, a year ago.

Though the country is mired in a currency crisis and political turmoil, the banking system appears stable.

These interbank lending rates represent a subsidy by foreign institutions in exchange for access to domestic Turkish business. This practice has been around for a while, and that it’s persisting through the current market gyrations suggests lenders are betting that this crisis will pass. Underlying this stance is the idea that President Recep Tayyip Erdogan’s tactics haven’t done any real damage to the economy, and there’s a prospect for relative stability to resume after his (all but certain) reelection on June 24.

It’s a substantial subsidy. The spread between banks’ primary and secondary market rates is at least 200 basis points.

The cost of this goodwill has never been higher, because this appearance of banking stability is tenuous.

The lira’s 23 percent drop against the dollar in the past two months to a record low has real consequences. The rout will lift import prices, and drive the inflation rate higher – and it’s already in the double digits. Higher crude prices will only worsen the situation. S&P Global Ratings and Fitch Ratings have warned the decline could lead to a credit downgrade.

It gets worse. Erdogan’s fiscal plans will only worsen the current account deficit, already one of the worst in emerging markets. This shortfall drives the currency’s sensitivity to dollar strength, and there’s no sign of it abating given Turkey’s substantial reliance on overseas funding.

Turkey’s central bank could ride to the rescue – but it probably won’t. Policy makers meet on June 7 (if they can last that long), and a substantial interest-rate increase could break the death spiral between rising inflation and an ever-weakening currency. But given that the President, rather fantastically, believes higher rates lead to higher inflation, this is extremely unlikely. His views are crippling Turkey.

Even if Erdogan were to allow a tiny move, that wouldn’t be enough. The central bank raised rates by 75 basis points at its last meeting, on April 25. Unfortunately the lira's recovery was fleeting. Having let this spiral perpetuate, a rate hike of several hundred basis points from the current 13.5 percent would be the minimum needed to regain control of prices. But there’s more at stake now than inflation. Officials have to ensure basic financial stability, and prevent an economic crash.

The commercial banks are floating on an apparent island of calm. But as these real problems hit home, foreign lenders’ willingness to offer subsidies to their Turkish counterparts could evaporate. The more immediate problem may be their willingness to refinance any foreign currency loans extended in better times to Turkish companies. Any reluctance here, or a serious change in borrowing charges, raises the risks of funding strains and potentially defaults that could severely test domestic banks.

Unless the central bank asserts its independence and raises rates aggressively, the rest of the economy will drag the banks down anyway.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

©2018 Bloomberg L.P.