Quant Minefield Clears as Correlations Plunge From 20-Year High

Quant Minefield Clears as Correlations Plunge From 20-Year High

(Bloomberg) -- It will take a lot more than a mini-skid in the great stock rally of 2021 to hurt a popular breed of Wall Street quant that finally has a shot at redemption this year.

The $2 trillion universe of rules-based funds that dissect equities by their factors, like how fast prices have risen or how cheap companies look, is on the rise as healthy market patterns reminiscent of the pre-virus world return.

Long-only systematic funds are beating benchmarks by 1.4% so far in 2021 to outrun fundamental peers, according to a Friday note from Sanford C. Bernstein. Just last January, strategists there warned of a “quant apocalypse,” in part thanks to the multi-year rally in Big Tech that caused diversified investors to underperform. The pandemic mayhem only added insult to injury.

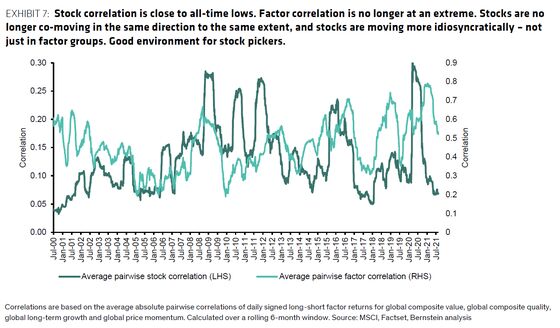

Now, with fewer sharp rallies and reversals spurred by news on lockdowns and vaccines, stocks with high dividend yields, for example, are moving independently from those with big profit margins. Factor correlations have plunged to pre-pandemic levels, after surging to the highest in at least two decades at the start of 2021, Bernstein data show.

AQR Capital Management’s market-neutral strategy is set for its best year since 2015 thanks to a bumper first quarter, while its long-short equity portfolio is poised for a record in its eight-year history.

“This set-up for low correlations, it’s been a good three or four years since we’ve seen it,” said Josh Russell, a New York-based systematic portfolio manager at Carson Wealth. “This is what you wait for.”

Like practically everyone else, multi-factor quants shot the lights out in the historic first quarter as risk-on strategies skyrocketed. The shift now is more fundamental -- stock groupings are dancing to their own beat, bolstering confidence in the fundamental rules discovered by academics decades ago.

Momentum, quality and low volatility have all made money this quarter, Dow Jones market neutral indexes show. Value has stabilized after sliding in June.

The prospect of renewed market stress hasn’t gone away. As U.S. stocks gyrated this week thanks to the spreading delta variant and the Federal Reserve’s plan to taper stimulus, tech mega-caps outperformed. It’s a small reminder of the kind of concentrated market moves seen in recent years -- and turbocharged in 2020 -- that have hurt factor quants with diversified books.

Yet through a medium-term lens, there’s been a sea change in trading conditions for active managers. With bond yields rising with inflation expectations over the past year, investors are no longer all crowding into Big Tech, allowing a broader range of shares to rise.

“The level of correlation among factors has now reverted back to normalized levels,” the Bernstein team led by Sarah McCarthy wrote in a note. “This indicates stocks are moving more idiosyncratically -- not just moving about in factor groups -- an easier environment to pick winners and losers.”

Factor styles come in all shapes and sizes. The risk-on camp includes value, which likes cheap and often more cyclical stocks, and size, a tilt toward small caps. In the risk-off camp are companies seen offering low volatility or reliable profits, dubbed quality. The quant mantra has it that these investing strategies may not pay off day-in and day-out, but put them together and diversification will work over the long haul.

The problem in pandemic markets was that factors were in thrall to macro-driven swings. From the depths of the Covid-induced recession to the vaccine-sparked bull run, the risk-on and risk-off factors mostly canceled each other out -- meaning quants made no money or even posted losses.

Now market swings are proving more stable. The 90-day volatility of the momentum investing style has also dropped to the lowest since 2019, a sign stock leadership is not flip-flopping violently. The 40-day correlation between value and momentum is now just 0.3, after the two factors mirrored each other almost perfectly from late 2019 through April 2021.

No surprise then that after two dismal years, Vanguard Group’s Market Neutral Fund hasn’t lost money for six straight weeks for its best run since 2017.

“When the sentiment -- whether it’s risk on or risk off -- gets extreme, that’s when it’s difficult for factors to perform the way you’d expect,” said Sumali Sanyal, a Durham, North Carolina-based senior portfolio manager at investment firm Xponance. “You don’t have those extreme spikes, and you’ll see multi-factor models being able to perform better.”

©2021 Bloomberg L.P.