‘Play-the-Pause’ Trading Strategies Gain Traction on Wall Street

`Play-the-Pause' Trading Strategies Gain Traction on Wall Street

(Bloomberg) -- The Federal Reserve’s dovish monetary-policy pivot is fueling the rise of a new wave of trading strategies designed to capitalize on a pause in the central bank’s tightening cycle.

Vanguard Group Inc.’s Gemma Wright-Casparius says she expects to play both sides of the range-bound Treasury yield curve, while Morgan Stanley Investment Management’s Michael Kushma is looking to build extra carry into the firm’s global bond portfolios. HSBC Holdings Plc’s Max Kettner says it’s time for fund managers to be positioned neutral versus their benchmarks, while preparing to aggressively adjust at a moment’s notice.

Even as volatility crumbles across stocks, bonds and currencies, investors see plenty of opportunities. Market veterans are anticipating large swings in sentiment amid one of the most uncertain interest-rate outlooks in recent decades, as well as ongoing trade and geopolitical tension. With the Fed’s shift causing popular trends to stall, many see new ways to make money for those willing to change tack.

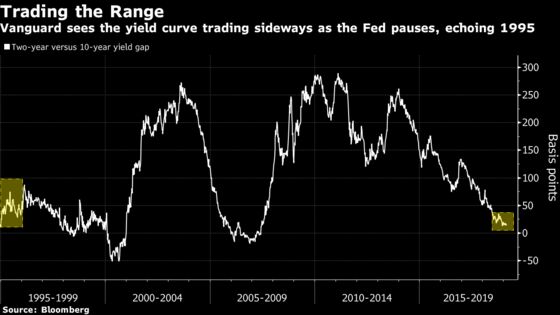

Playing Both Sides

Wright-Casparius, a senior money manager at Vanguard, still remembers trading swings in the gap between 2- and 10-year Treasury yields when the Fed held rates steady for extended periods in 1995 and 1996. The curve plied a narrow range at the time, and she expects spreads to react similarly now as they did back then.

“During the last protracted pause period for the Fed, everything went sideways,” Wright-Casparius said. “It didn’t mean we didn’t trade both ends of that range. And in this pause, you will get volatility from time to time because of the uncertainty about the path of the economy and the Fed policy.”

The 2-year 10-year spread is currently about 15 basis points, after dwindling to just 9 basis points in December, the least since 2007.

Going Tactical

The present environment is ripe for hard turns in investor sentiment, and traders are likely to see markets sway from pricing in “Goldilocks scenarios” to renewed fears of a recession, according to Kettner, a multi asset strategist at HSBC.

“We’ll probably have the market keep questioning where we really are,” Kettner said. “The real way for investment managers to make money is sort of being quite neutral to their benchmark and then flipping in-and-out pretty aggressively.”

U.S. stocks have rebounded from their worst December since the Great Depression, triggered in part by concerns over a slowdown in earnings. The S&P 500 Index has surged about 19 percent from its low on Dec. 26. Still a debate on the trajectory of corporate profits in raging.

Carry On

Capturing returns by parking cash in assets denominated in high-yielding currencies while funding the trade in a low-rate currency is becoming increasingly attractive, according to Chris Turner, head of foreign-exchange at ING Groep NV’s London branch. He doesn’t expect further Fed tightening until the third quarter, and recommends being long carry through the Turkish lira or Mexican peso, where one-year rates are at about 17 percent and 8 percent, respectively.

“It’s too early to expect super perfect conditions for a carry trade,” Turner said. But investors “are going to be looking for dips in those high yielders to get back on, unless some clearly big negatives emerge.”

Low volatility is a boon for carry, as it reduces the chance that changes in currency values will erode gains made on interest-rate differentials. A JPMorgan Chase & Co. gauge of global currencies swings has fallen to 7.5 percent, from 9.4 percent in January.

Kushma, chief investment officer for global fixed income at Morgan Stanley Investment Management, is focused on conservatively boosting carry in the firm’s debt funds. That’s because key 2018 headwinds for riskier assets, including further Fed tightening, a strong dollar and rising Treasury yields, have now dissipated.

“We are trying to build in extra carry into our portfolios in a safe way,” said Kushma, who said he favors buying emerging-market debt from countries such as Brazil, Poland and Hungary, as well as securitized assets linked to the U.S. residential and commercial property. “But we can’t afford to see weaker and weaker data, even as the Fed is in a more neutral stance.”

The Doomed Dollar

A lack of any imminent Fed tightening could spell bad news for the dollar, according to Greg Gibbs, founder of Amplifying Global FX Capital, especially if global confidence improves.

“A pause in U.S. rates could help support a broad-based recovery in other currencies, strong global equities and weakness in the dollar,” Gibbs said.

The greenback has more than held its own in recent weeks as global growth headwinds prompt central banks around the world to tilt dovish. But if key concerns over global trade, Chinese stimulus, euro-zone growth and Brexit are resolved, global confidence would improve and weaken the dollar, Gibbs said.

Looking Past the Pause

Some, like Jeffrey Snider, global head of research at Alhambra Investments, says now is the time to wager on what happens after the pause, given that the business cycle is already long in the tooth and the strong track record of money-market traders in predicting Fed policy. Overnight index swaps have priced out any chance of a rate increase in 2019, and are pricing in a full 25 basis point cut over the next two years.

“One way to trade this is be long any kind of bond,” Snider said. “There is already a high probably in the futures market for a rate cut.”

To contact the reporters on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net;Misyrlena Egkolfopoulou in New York at megkolfopoul@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.