‘Japanification Effect’ Means Treasuries Should Be This Sleepy

‘Japanification Effect’ Means Treasuries Should Be This Sleepy

(Bloomberg) -- Concern is swelling on Wall Street that sleepy markets are setting a trap for investors betting on continued tranquility.

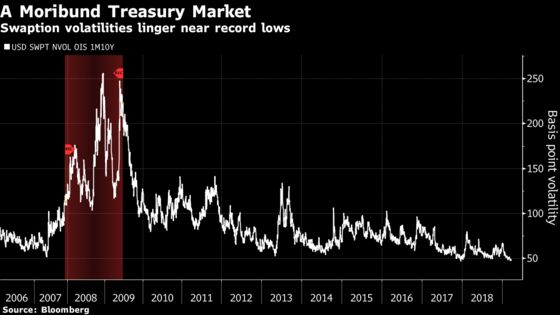

But in the bond market -– the most soporific of them all -– it’s perfectly appropriate for volatility to be plumbing record lows, according to TD Securities, based on how little yields have been swinging.

“Current implied vols are not significantly stretched, suggesting that swaption volatiles may indeed stay low for some time,’’ writes U.S. rates strategist Wen Lu, highlighting the drop in one-month, 10-year swaptions, or options giving the buyer the right to enter into an interest-rate swap agreement.

TD is staying neutral on realized volatility in U.S. Treasuries, citing the “Japanification effect’’ created by the Federal Reserve’s dovish pivot, a nod to the Bank of Japan’s yield curve control strategy which crushed longer-dated swaption volatility in the JGB market. Relative lack of appetite from buyers and sellers alike in that part of the surface is also contributing to a low level of implied fluctuations, he added.

“We find it unattractive to be outright short but also difficult to be outright long, especially when macro and programmatic participants are willing to sell vol on any spikes,’’ concludes Lu.

To contact the reporter on this story: Luke Kawa in New York at lkawa@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Dave Liedtka, Rita Nazareth

©2019 Bloomberg L.P.