‘A Lot of Very Young People’ Are Going to Buy the Dip in Stocks

‘A Lot of Very Young People’ Are Going to Buy the Dip in Stocks

(Bloomberg) -- Someday, the post-pandemic equities rally is going to end. When it does it will take a lot of newly christened stock bulls with it.

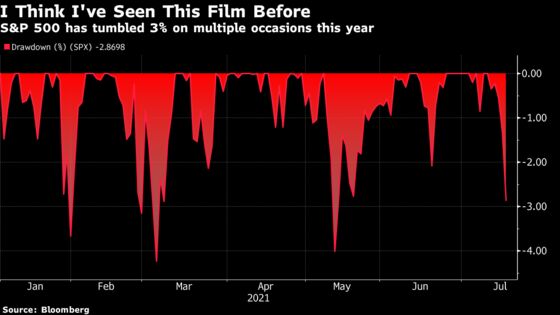

Their refusal to bend has been the signature fact of the stock market for at least 12 months, putting a floor under four other selloffs in 2021 alone that look just like the one that has sheared almost 3% off the S&P 500 Index since Thursday. Whether the devotion of retail investors is enough to turn the tide again is the biggest question in markets right now.

“There’s a lot of very young people in the accumulation phase,” said Dan Egan, managing director of behavioral finance and investing for robo-adviser Betterment, who added that younger investors in particular have used selloffs as buying opportunities. “If they have any excess cash sitting around, they’re going to use it to buy in.”

Four other times this year, the S&P 500 Index has closed 3% below a historic high, and each time it rebounded to a record, according to data compiled by Bloomberg. That shows how difficult it’s been to dislodge the retail traders who have fueled the rally -- as well as the conditioning at work in markets that will inevitably be their comeuppance.

“The dip buyers have stepped in very quickly and bought very quickly and that’s one of the reasons we haven’t had a full 10% correction -- and frankly I don’t think we’ll have one this time either for that reason,” said Randy Frederick, managing director of trading and derivatives for Charles Schwab Corp. “Every dip has been bought and immediately paid off within a week or two of not just where it started but above.”

Will this be the selloff that sticks? Some say yes. Gina Martin Adams, Bloomberg’s stock strategist, says big drops in small companies and transportation firms bode particularly badly. “Leading indicators imply a breakdown in stock prices remains most likely in the interim,” she wrote in a note.

Still, it’s been a long time since anything could shake the nerves of the retail cadres who have fueled the post-pandemic rally. Predicting they will stop plowing money into the market has been a losing bet to date.

Exchange-traded funds are about to lure more money in seven months than in any calendar year on record -- with $486 billion added so far in 2021, the inflow will soon surpass last year’s $497 billion full-year record. In July alone, equity ETFs have taken in more than $15 billion.

Other signs portend good news for the bulls. A measure of implied volatility in VIX options known as the Cboe VVIX Index is trading above 140, the level it’s been at three other times since October and which became an ultimate buying opportunity. When the so-called volatility of volatility measure peaked at 152 in late October, that marked the lowest point of the S&P 500, which proceeded to embark on a rally. When it rose to 158 on Jan. 27, the equity gauge found its trough two days later. When the same happened in mid-May, the S&P 500 rose more than 1% in each of the next two days.

As the market’s run higher, options trading has also picked up again, with strategists from Goldman Sachs Group Inc. saying last week the month-to-date average daily notional amount traded has risen to a record. Roughly $534 billion of options have changed hands on average each day this month, with more than half of that happening in call options. That’s above last year’s average of around $367 billion.

For many strategists, the current retreat is a blip before the reflation trade reasserts itself once again. That would imply stocks sensitive to the economic reopening will stage a comeback, with cyclical and value-oriented sectors of the market standing to benefit the most.

UBS Global Wealth Management Chief Investment Officer Mark Haefele in his monthly letter to clients last week wrote that fears over premature Federal Reserve tightening or the spread of the delta variant derailing the recovery are “overdone.” Consumers have strong balance sheets, he said, and the need for businesses to rebuild inventory and capex could sustain economic momentum and corporate earnings.

Marko Kolanovic, JPMorgan Chase & Co.’s chief global markets strategist, is also among those calling for such a bounce, arguing that it could happen once delta variant fears subside and inflation surprises persist.

And Michael Purves, founder and CEO at Tallbacken, on Monday raised his year-end target for the S&P 500 to 4,800 from 4,250, implying a roughly 13% gain from current levels.

“We think the combination of low, and stable, interest rates with a strong earnings growth trajectory will support the equity risk premium at healthy levels at 4,800 at year end,” he wrote in a note. “While we are past peak earnings growth, the earnings growth story into and through 2022 will continue to be robust. Further, we find little evidence that a rollover in peak earnings growth is a reason to sell the market.”

©2021 Bloomberg L.P.