Goldman Says Yuan Will Hit 7 as China Avoids Heavy Meddling

The yuan has come under intense pressure to fall as China became embroiled in a trade war with the U.S.

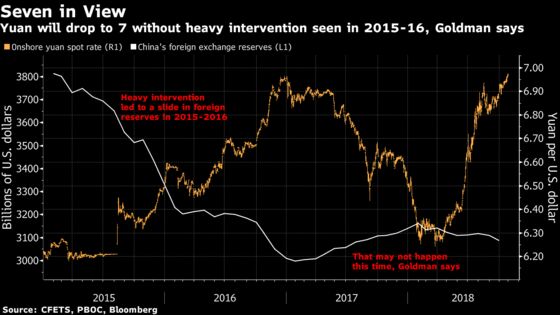

(Bloomberg) -- China’s policy makers will likely allow the yuan to hit the key level of 7 per dollar within the next six months without conducting heavy intervention, according to Goldman Sachs Group Inc.

While the authorities may guide sentiment by issuing stronger fixings, they won’t likely sell the dollar heavily to defend the currency as they did in the aftermath of a shock devaluation three years ago, according to MK Tang, a senior China economist at Goldman in Hong Kong. That is because the conditions for the yuan to hit 7 are "more mature" than in the past as capital outflows remain contained, he added.

"We see good economic reasons arguing for a weaker yuan, especially in the coming months," Tang said. "It’s only a matter of time for the yuan to hit 7."

The yuan has come under intense pressure to fall as China became embroiled in a trade war with the U.S. and loosened its monetary policy to bolster a slowing economy. The currency touched its weakest level in more than a decade this week, spurring debate on when and whether it could slide to 7 for the first time since the global financial crisis.

Another reason policy makers are likely to be averse to outright intervention is the yuan is more liberalized than in the past, Tang said, and such tools will only be used moderately in the future. Chinese officials have been working to make the yuan more market-driven as they seek to attract more foreign investors onshore and promote the currency’s global use.

How far the yuan can slide may depend on how much weakness the PBOC is willing to tolerate. In early 2017 when the currency was close to the current level, the authorities engineered a cash squeeze in the offshore market to punish bears. The latest sign of officials’ uneasiness came on Wednesday, when Hong Kong’s government said the Chinese central bank will issue bills in the city for the first time ever -- a move that would drain liquidity and support the yuan.

Read more: China Says More Aid Coming as Downdraft From Trade War Rises

Signs of rising fund outflows are emerging as official data suggest that Chinese investors’ demand for foreign-exchange surged the most in nearly two years in September. Still, the level is only a fraction of the capital flight seen after the 2015 yuan devaluation. The government has had capital controls in place since then -- limiting banks’ cross-border transfers and making it less convenient for households in China to buy the dollar -- to stem fund exodus.

"It’s possible that outflows will pick up from September as the yuan continues to weaken," Tang said, adding he sees the yuan weakening to 7.1 in the next six months. "I expect policy makers to use capital controls more proactively to manage outflows pressures."

The onshore yuan climbed for the first time in four sessions, rising 0.38 percent to 6.9473 per dollar as of 5:24 p.m. Thursday in Shanghai. That move came after the People’s Bank of China set its daily reference rate at a stronger-than-expected level. The offshore rate gained 0.38 percent.

Here are some other points Tang made:

- Trading could become "sticky" around 7, with the yuan moving stronger and weaker than that level several times amid moderate PBOC management of the currency

- Policy makers may manage sentiment by using the counter-cyclical factor in the fixing, which would help investors to get used to the idea of the yuan at 7 per greenback

- An offshore funding squeeze is possible, but it depends on whether herd behavior is seen in the offshore market

- Capital outflows won’t become as serious as in 2015-16

To contact the reporter on this story: Tian Chen in Hong Kong at tchen259@bloomberg.net

To contact the editors responsible for this story: Richard Frost at rfrost4@bloomberg.net, Philip Glamann, David Watkins

©2018 Bloomberg L.P.