Distressed Argentina Oil Firm Leads Emerging-Market Bonds

YPF Is a Rare Bright Spot for Argentine Debt After 2021 Default

(Bloomberg) -- Only 14 months ago Argentina’s YPF SA was a nightmare for investors caught out by a $6 billion distressed debt restructuring. Now, in a swift turnaround, the 100-year-old state-run oil company is producing the best fixed-income returns in all of emerging markets.

YPF has rewarded steely creditors with returns topping 20% this year on some of its notes. It emerged from the pandemic with a strong cash position after bondholders agreed to push back $630 million in debt payments, helping fund long-term investments in Vaca Muerta, the vast Patagonian shale patch. Repeated promises by executives to reverse a long decline in oil production have finally started to come true.

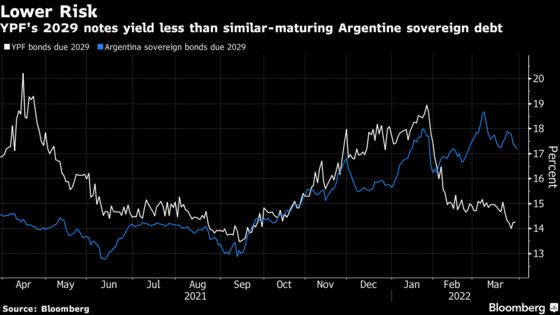

The operational turnaround since Fitch Ratings and S&P Global Ratings declared YPF in default in February 2021 has brought yields on the company’s debt below Argentine government bonds, a phenomenon almost unheard in any country given that sovereign debt is usually considered the least risky. Even architects of the comeback plan can’t quite believe how well it’s going, especially as higher fuel prices amid the global oil rally help to shore up the company’s books even further.

“Things evolved in a much better way than we anticipated,” Chief Financial Officer Alejandro Lew said in an interview. “If we’d continued to decline and hadn’t put forward a significant capex plan, the situation would’ve become completely unsustainable.”

After hitting lows of about 51 cents on the dollar in the months after the restructuring, YPF’s $750 million of bonds maturing in 2029 now trade at almost 72 cents. A 23% return this year beats all other notes from sovereign and corporate issuers in emerging markets, according to a Bloomberg index, which shows an average loss of 9.8%. In fact, YPF bonds occupy five of the top six slots in 2022.

Lew, a former fixed-income syndicate trader at JPMorgan Chase & Co. in New York, is now overseeing hikes to YPF’s domestic fuel prices that are spurring another boost in capital expenditures, driving what would be the company’s biggest annual jump in oil and gas production in a quarter of a century.

That rosy picture contrasts with a gloomier situation for creditors in Argentina more broadly, with the International Monetary Fund already warning of risks to a brand-new repayment program. That has put yields on YPF’s quasi-sovereign debt in the strange position of trading inside the sovereign.

Investors are assigning less risk to YPF because of last year’s restructuring and the receipt of a $300 million loan from the Andean Development Corporation, or CAF, in January. Plans for interest rates to step up on several of the company’s securities are also bolstering prices, according to Paula La Greca, a corporate credit analyst at TPCG Valores in Buenos Aires.

Read More: Argentina’s Energy Bonds Seen Top 2022 Bet

Siby Thomas, a portfolio manager at T. Rowe Price in Baltimore, said YPF’s healthy cash position has given him confidence in the company despite concerns about other corporate issuers in Argentina.

YPF had $1.1 billion in cash and equivalents at the end of 2021, according to its last earnings presentation. The company has $700 million in debt maturities this year, with about $400 million stemming from international bonds that it will mostly pay with the CAF loan.

“We’re fairly bearish on Argentina corporates, but in the short term we’re comfortable with YPF,” Thomas said.

Argentina Risk

The biggest risk for YPF is that it operates in Argentina, meaning it could be whipsawed by frequent changes to the country’s economic policies, including currency controls, and inflation running at more than 50% a year.

Under current foreign-exchange regulations, YPF should be able to access dollars for all its debt payments through 2024, Lew said.

Another question mark for investors is government oversight that limits how much YPF is allowed to increase diesel and gasoline prices. That means the company only fully benefits from the global commodities rally on the almost 20% of its revenue that comes from exports and products sold locally that aren’t regulated.

“YPF’s crude and fuel pricing policies will likely result in its cash flow lagging global oil peers,” Bloomberg Intelligence analysts Fernando Valle and Brett Gibbs wrote in a note.

ESG Plans

If the numbers don’t add up, YPF says it won’t hesitate to rein in drilling investments in Vaca Muerta to ease stress on its finances.

YPF is also in early-stage plans to swap some of its overseas notes for a sustainability-linked bond to meet rising demand for securities based on environmental, social and governance, or ESG, goals, Lew said.

Even as the world strives to accelerate the energy transition to cleaner fuel and move away from fossil fuels, Lew believes the window is still wide open for YPF and other Argentine drillers to grow shale production.

“You have a trade-off around the world between climate change and energy poverty,” Lew said. “I think the market went too far ahead on the E and forgot about the S in ESG. We still need to supply cheap energy to billions of people. The S requires investments in oil and gas to remain pretty high.”

©2022 Bloomberg L.P.