Yield Hunters Lured by Junk Bonds Even as Defaults Pick Up

Yield Hunters Lured by Junk Bonds Even as Defaults Pick Up

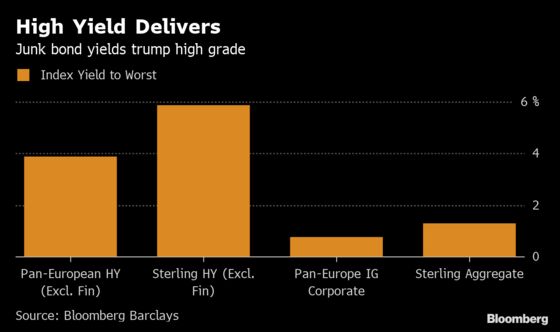

(Bloomberg) -- Investors are rushing to buy high-yield bonds in Europe at a time when the number of issuers defaulting has reached the highest level since 2010.

The 12-month notional-weighted default rate could rise to 2% by year-end compared with 0.6% a year ago, according to analysts at JPMorgan Chase & Co. Meanwhile high-yield funds with a European focus have attracted inflows for five consecutive weeks totaling 2.7 billion euros ($3.0 billion), the analysts said citing the bank’s own data.

“The search for yield will continue with high-yield being a renewed hunting ground for investment grade buyers,” said Andrew Wilmont, a senior investment manager at Pictet Asset Management SA in Geneva, which manages 165 billion euros of assets. “They’re on the lookout for better returns amid a growing negative yielding market.”

But the current rally across fixed income markets, fueled by speculation that the European Central Bank is preparing another round of monetary stimulus, may be masking a key risk in the high-yield market: the fragility of corporate balance sheets.

Blow-Ups

Amid the hunt for yield some portfolio managers are avoiding the riskiest categories of high-yield bonds however, given concerns about idiosyncratic risks, valuations and liquidity.

“Investors have to keep owning the right names and with default rates rising it’s a case of trying to avoid the blow ups,” said Azhar Hussain, head of leveraged finance at Royal London Asset Management, who manages 4.7 billion pounds of assets.

Spread dispersion in Markit’s iTraxx Crossover index is at an all-time record, indicating the current diversity of risks in high-yield names and how selection is critical for portfolio performance, Bloomberg Intelligence strategist Mahesh Bhimalingam wrote in a research note Tuesday.

There’s “a huge bifurcation in the market right now” with investors buying BB-rated and good quality B-rated names and “not daring to touch weaker B-rated and triple-C deals with a barge pole,” Royal London’s Hussain said.

Yield Grab

A decade of easy monetary policy has pushed bond investors into riskier assets that yield enough to match their liabilities. And with hints of more monetary stimulus to come, investors predict it’s only a matter of time before people turn their attention to what is yielding more.

“Value is being squeezed thanks to the inflows from investment-grade accounts and we now expect investors to begin reaching down the quality curve for yield,” said Mark Benbow, a fund manager at Kames Capital Plc. “People thought we were at the end of the cycle but Draghi is giving us a few more hours on the dance floor.”

The Edinburgh-based fund manager said he has started buying CCC-rated credits -- which are seven levels below investment grade -- after de-risking earlier this year in a bid to boost his returns, but added that the key is to stay credit selective.

“The next bet will be on CCC credit, it will be a case of ‘that looks reasonable.’ Normally we know it’s the final hour when CCCs let rip,” he said.

To contact the reporter on this story: Laura Benitez in London at lbenitez1@bloomberg.net

To contact the editors responsible for this story: Vivianne Rodrigues at vrodrigues3@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.