Yield Curve Drama No Reason to Lose Your Mind, Stock Pickers Say

The basis for their gripe is the world’s sudden obsession with the relative altitude of interest rates.

(Bloomberg) -- An inverted yield curve may be a recession portent and evidence of generalized market chaos, but it’s no reason to cut and run in equities, was the near-unanimous view of professional equity managers.

While someone was obviously hitting sell Wednesday, sending the Dow Jones Industrial Average to its worst day of the year, it wasn’t these investors, who while trying to insulate their portfolios said they weren’t bailing. For the most part, fear of missing out continues to overpower fear of getting decimated.

“People believe that is going to cause a recession, that it’s only a matter of time. And in fact, what we find is that it takes quite a long time,” said Mariann Montagne, a fund manager at Gradient Investments, which oversees $2.3 billion. “We have a lot of money to make between now and then.”

The basis for their gripe is the world’s sudden obsession with the relative altitude of interest rates. Yield curve inversion, while an ominous sign, didn’t exactly sneak up on anyone, they note, while concerns about slowing growth, the Federal Reserve and trade with China began buffeting markets months ago. It was back then, not now, that Lamar Villere, a portfolio manager at Villere & Co., was raising cash and adding low-volatility stocks.

“We’re not bailing, and we’re not expecting all of a sudden something magic to happen,” Villere, who helps manage around $2 billion, said in an interview at Bloomberg’s headquarters in New York. “I don’t think anything fundamentally has changed for us based on the yield inversion.”

Cliched as it may be, managers with a longer-term horizon said the plunge, if anything, creates an opportunity to buy stocks. Jason Browne, president of Alexis Investment Partners, did just that in the past several days, using money he raised in July when markets were at an all-time high.

“It doesn’t mean I don’t own things like gold or more defensive positions that I can get more aggressive with,” Browne said by phone from Bethlehem, Pennsylvania. “But I’ve redeployed that cash because I feel what I was looking for in terms of a little pullback has happened. I’m more of a buyer within the context that when I look across the positions I own, they’re all things that I feel like I can trade around.”

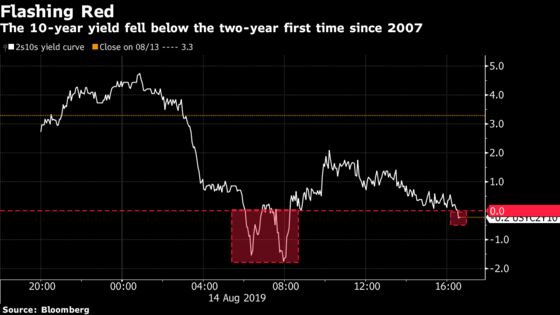

When the spread between two- and 10-year Treasury yields flipped 10 times since 1956, it preceded recessions. But never right away. The S&P 500 topped out anywhere from two months to two years later, data compiled by Bank of America strategists show. Gary Bradshaw, a portfolio manager at Hodges Capital Management in Texas, is also a buyer.

“Just because the 10 year is less than 2 year, it doesn’t preclude me from adding to the Microsofts, Visas and Paypals of the world,” Bradshaw, who helps oversee $1.5 billion at Hodges Capital Management, said by phone. “I’ve been sitting here buying attractive stocks that are beaten up, and I will continue to do that.”

It’s not like risk is new to the world. For months, trade tensions have been souring and signs that global growth is slowing have been cropping up. Angst was sparked anew on Wednesday after data showed Germany’s economy shrank in the second quarter and Chinese retail and industrial numbers came in below expectations.

To Ed Keon, a managing director and portfolio manager at QMA in New Jersey, that’s a signal stock prices can go lower. He’s been cautious for a while and kept a neutral to slight underweight stock position. Now he’s waiting for a further drop to add to his portfolio.

“Prices aren’t to the point yet where they are just compelling, but the data today with the industrial data coming out of about Germany’s economy and Chinese industrial numbers wasn’t all that great,” Keon said by phone. “We aren’t planning on making major portfolio changes until the prices are compelling.”

Timing the stock market decline following a yield curve inversion is a task for the brave of heart. Six of the last 10 times the yield curve flipped, the S&P 500 rolled over within three months. In the other four, the gauge didn’t top out until at least 11 months later, Bank of America data show.

Marshall Front, the chief investment officer at Front Barnett Associates in Chicago, is taking no chances timing the market decline. He reduced his stock position by about 2 percentage points 1.5 months ago, but not out of growth concern but because one of his positions started looking less attractive.

“Having a substantial equity exposure is still warranted, even though we have clouds that have built on the horizon,” Front said by phone. “Our investment policy and results are not going to depend upon whether we make a correct market timing decision. It’s about the item selection and about whether they fare the storms that definitely will be coming well.”

--With assistance from Olivia Rinaldi.

To contact the reporters on this story: Elena Popina in New York at epopina@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net;Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.