Yen Swaptions Signal 2016 Redux as Bets for BOJ Rate Cut Climb

Yen Swaptions Signal 2016 Redux as Bets for BOJ Rate Cut Climb

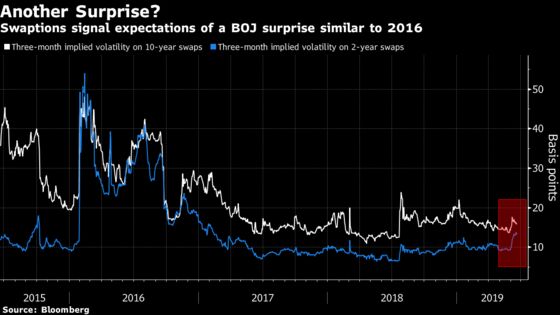

(Bloomberg) -- An esoteric metric in the rates markets is indicating that the Bank of Japan may pull off a policy surprise, just as it did three years ago.

Three-month implied volatility on two-year yen interest-rate swaps has touched its highest since February 2017, with the advance outpacing a rise in volatility on 10-year swaps, according to data compiled by Bloomberg. The so-called two-year swaptions climbed above the longer tenor in 2016, when the BOJ surprised markets with the introduction of its negative interest-rate policy.

JPMorgan Chase & Co. predicts that the central bank will lower its short-term interest rate to -0.3% from -0.1% in September to head off risks from an expected easing by the Federal Reserve. The BOJ will conclude a two-day policy meeting on Thursday.

“The move is probably driven by bets of a drop in rates in case the BOJ cuts its short-term borrowing costs,” said Shuichi Ohsaki, chief rates strategist at Bank of America Merrill Lynch in Tokyo. “Given that the BOJ looks to be avoiding a flatter yield curve, market participants see a greater likelihood of a cut to short-term rates” than a change in the 10-year bond yield target, he said.

While all 50 economists polled by Bloomberg News expect no policy change this week, 62% of them think that the BOJ will ramp up easing measures as its next step. That’s up from 48% in April, the survey shows.

BofAML’s expects the BOJ to remain on hold even if the Fed lowers rates, Ohsaki said.

--With assistance from Stephen Spratt.

To contact the reporter on this story: Masaki Kondo in Tokyo at mkondo3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Shikhar Balwani, Brett Miller

©2019 Bloomberg L.P.