Woodford’s Woes Hurt Active Managers Fending Off Passive Funds

Woodford’s Woes Hurt Active Managers Fending Off Passive Funds

(Bloomberg) -- Neil Woodford’s troubles gives advocates of passive investing another reason to slam actively managed funds.

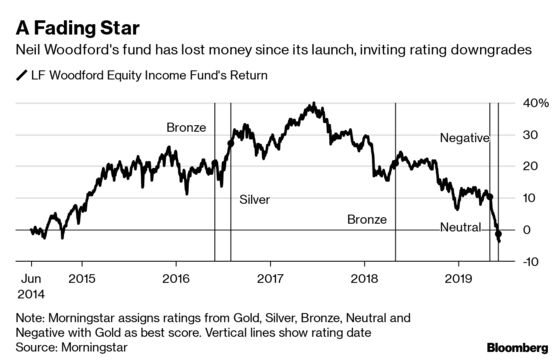

Once one of the U.K.’s most famous stock pickers, who made a name for himself over the past three decades, Woodford cracked under redemption pressure last week and locked investors out of his main fund following months of poor returns. Since then, Woodford’s loyal backers have bailed on him and he has come under fire from politicians, regulators and investors.

The real damage could reverberate across the U.K.’s 8 trillion-euro ($10 trillion) asset management industry. Active managers, which are facing scrutiny for charging high fees and failing consistently to beat their benchmarks, are already ceding ground to index and quantitative funds. Woodford’s move may further undermine investor faith in active management.

“The redemptions freeze by Neil Woodford’s fund could further damage the reputation of active management, serving as another catalyst for the move toward passive investing,” Bloomberg Intelligence analysts Athanasios Psarofagis and Eric Balchunas wrote on Tuesday.

In the U.S., where the move towards passive management is already threatening fund managers who earn a living by picking individual stocks and bonds, roughly four in every 10 dollars are invested in pools mimicking an index, according to the Investment Company Institute. In the U.K. almost 75% of assets are still actively managed but that’s down from 83% a decade ago, data from The Investment Association show.

Woodford, who charges 65,000 pounds ($83,000) a day to manage the now frozen LF Woodford Equity Income Fund, or about 65 basis points of its assets, according to Bloomberg calculations. That could be enough of a reason for investors in U.K. investments to shift their focus. Some European exchange-traded funds that offer similar exposure for less than 40 basis points have outperformed the Woodford fund since July 2017, according to Bloomberg Intelligence.

When Woodford allows investors to take their money out, Psarofagis and Balchunas say they expect the capital to be redeployed into cheaper index tracker funds rather than given to other managers.

Under Pressure

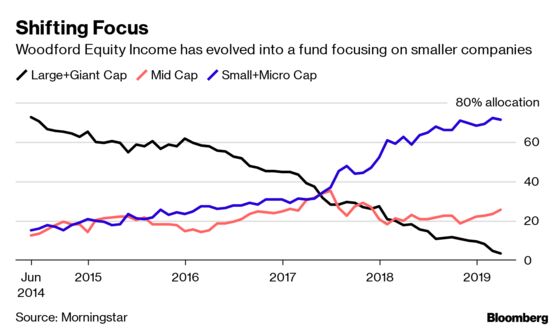

Woodford’s woes appear to be self inflicted. By changing his strategy to relatively less liquid securities he sowed the seeds of his current troubles years ago.

Investors were attracted by Woodford’s 26 years of stock picking success at Invesco Perpetual and allocated billions of pounds to his new firm in 2014. St James’s Place took 3.7 billion pounds of its clients’ assets out of Invesco and parked it in Woodford’s new funds.

Woodford’s new firm started by picking large liquid stocks but kept moving towards smaller companies, with an emphasis on domestic and early-stage companies. The moves dramatically altered the profile of his fund.

They raised the risk profile of Woodford’s funds and largely remained unnoticed. That contrasts starkly with the approach taken by index funds, which are easy to predict because they are based on additions and exclusions of companies in the benchmarks they track.

“If active managers want to keep their market share vis a vis passive investing, the Woodford debacle can be a good case study of what to avoid,” said Nicolas Roth, head of alternative assets at Geneva-based Reyl & Cie.

To contact the reporter on this story: Nishant Kumar in London at nkumar173@bloomberg.net

To contact the editors responsible for this story: Shelley Robinson at ssmith118@bloomberg.net, Sree Vidya Bhaktavatsalam

©2019 Bloomberg L.P.