Fed Preps Second $75 Billion Blast With Repo Market Still On Edge

It had been more than a decade since Federal Reserve traders jumped into U.S. money markets to inject cash.

(Bloomberg) -- It had been more than a decade since Federal Reserve traders jumped into U.S. money markets to inject cash. And they seemed to get the reaction they wanted Tuesday morning, instantaneously driving down key short-term rates that had spiked to as high as 10% and threatened to muck up everything from Treasury bond trading to lending to companies and consumers.

But the move didn’t last long.

By the end of the trading session, rates were grinding back up, prompting Fed officials to fire off a second missive late in the day: They would be back Wednesday morning to offer another $75 billion of cash to the market. Overnight repurchase rates were being quoted at around 4% for Wednesday morning, according to Jefferies.

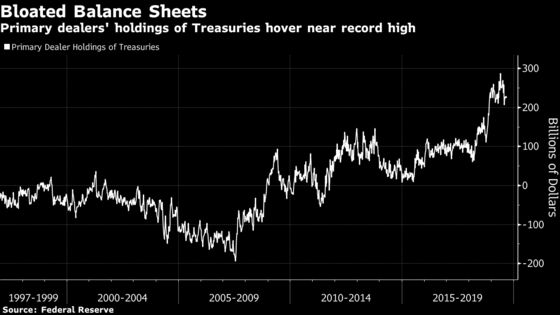

The moves underscored just how deep the structural problems in U.S. money markets have become. Namely, there is often not enough cash on hand at major Wall Street firms to meet the funding demands of a market trying to absorb record Treasury bond sales needed to cover U.S. budget deficits. The solution, according to longtime observers, would be for the Fed to continue to inject cash on a regular basis.

“The underlying problem is that there isn’t enough liquidity in the system to satisfy the demand and the job of the central bank is to provide such liquidity,” said Roberto Perli, a former Fed economist and partner at Cornerstone Macro in Washington. “What the Fed did was just a patch.”

A couple of catalysts caused the squeeze in repo liquidity. There was a big swath of new Treasury debt that settled into the marketplace -- adding to dealer balance sheet holdings -- just as cash was sucked out by quarterly tax payments companies needed to send to the government. If left unchecked, the escalation in rates could do damage to the broader economy by hiking borrowing costs for companies and consumers.

The timing couldn’t have been worse, with Fed leaders and many key New York Fed staffers gathered in Washington for a two-day policy meeting that will end Wednesday. Fed officials are widely expected to cut their target rate by a quarter-point. But the money-market problem threatens to overshadow that, as Wall Street is ready to find out what, if anything, the Fed might do to fix the situation for good.

“The increase in repo and other short-term rates is indicative of the reduced amount of balance sheet that financial intermediaries -- particularly primary dealers -- are either willing or able to provide those in search of short-term financing,” said Tony Crescenzi, market strategist at Pacific Investment Management Co. and author of a 2007 edition of “Stigum’s Money Market,” a widely read textbook first published in 1978. “It serves as a reminder of the challenges that investors could face in other ways if and when they seek to transfer risk -- sell their risk assets -- during a risk-off mode.”

This is far from the first bout of volatility in the over $2 trillion repo market, but eye-catching moves tend to happen only at quarter- or year-end when liquidity sometimes dries up -- not in the middle of the month, as it is now. Even setting aside this week’s huge spike, turmoil has been more pronounced following the 2008 crisis because reforms designed to safeguard the financial system have driven some banks out of this market. Fewer traders can lead to rapid swings by creating imbalances between supply and demand.

Fed interventions in the repo market, like the one deployed Tuesday and planned for Wednesday, were commonplace for decades before the crisis. Then they stopped when the central bank changed how it enacted policy by expanding its balance sheet and using a target rate band.

The tumult seen Monday and Tuesday doesn’t mean another global funding crisis, even though trouble getting funds through repo a decade ago doomed Lehman Brothers and almost snuffed out the global financial system.

But, many experts say, these wild few days show that there’s not enough reserves -- or excess money that banks park at the Fed -- in the banking system. That means traders are this week having to pay up to get these funds, even as bank reserves total more than $1 trillion. And it suggests the Fed may again have to grow its $3.8 trillion balance sheet through quantitative easing, or debt purchases that create fresh reserves.

There are other remedies. The Fed has considered introducing a new tool, an overnight repo facility, that could be used to reduce pressure in money markets. And some strategists predict it may make another technical tweak to something called the interest rate on excess reserves on Wednesday, an attempt bring markets back in line.

“There were a confluence of factors that triggered the issues this week,” said Darrell Duffie, a Stanford University finance professor who’s co-authored research on repos with Fed staffers. “But the fact that it’s happening means something at the Fed should be done. For the Fed to be really confident in ending the issues, they will have to grow the balance sheet.”

The U.S. government has made matters worse over the past year by adding a record amount of new debt, and that will likely only increase as the deficit swells past $1 trillion. That has buoyed the amount of debt that dealers have on their balance sheets, and the repo market is one way they finance those positions. That said, their Treasury holdings are down from a peak in May, so that’s not necessarily behind this week’s big moves.

“Supply is a backdrop contributor to the issues, as there is just that much more collateral that needs to be financed,” said Seth Carpenter, a former adviser to the Fed Board of Governors who is now chief U.S. economist at UBS Securities LLC. “The market is still trying to deal with tight balance sheets from dealers. Overall this is all part the market shifting through time to a new set of realities.”

To contact the reporter on this story: Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Nick Baker, Kara Wetzel

©2019 Bloomberg L.P.