With Rate Hold a Given, Twist Aim in Focus for Indian Bonds

The RBI has so far bought Rs 40,000 crore of long-term bonds, while selling 282.8 billion rupees of short-tenor debt.

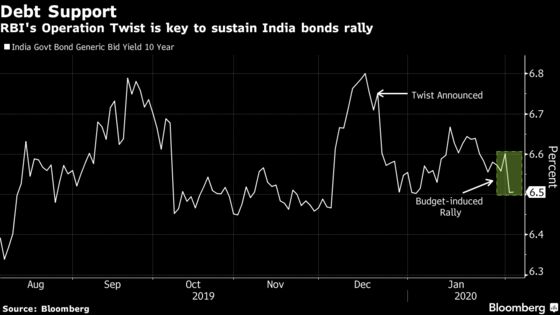

(Bloomberg) -- Holding on to recent gains in Indian sovereign bonds depends on whether the central bank will extend its open-market debt purchases, traders say.

With status quo on interest rates factored in at this week’s monetary policy meeting, they will be closely following Governor Shaktikanta Das’s press conference Thursday for cues on how long the Federal Reserve-style Operation Twist will be used to soak up supply in another year of record borrowings.

“Communication on the objective of Operation Twist will play a key role in making or breaking bonds,” said Arvind Chari, head of fixed income and alternatives at Quantum Advisors in Mumbai. Clarity on whether the twist is meant to “manage the yield curve” will help the market gauge the extent of the tool’s use, he said.

Ten-year bond yields have slid 24 basis points since the first announcement of Operation Twist on Dec. 19, with the gains accelerating after the government’s 7.8 trillion rupees ($109 billion) borrowing plan unveiled at the Feb. 1 budget met expectations. The rally may fade if there’s reluctance to extend the debt-support measure, Chari said.

The yield rose one basis point to 6.51% at 10:05 a.m. in Mumbai on Wednesday.

The RBI resorted to Twist as economic growth failed to recover even after five rate cuts last year and term spreads -- the gap between 10- and 2-year bond yields -- widened to a nine-year high in December. On its part, the central bank said the measure was guided by “liquidity and market conditions.”

Relief Rally

The RBI has so far bought 400 billion rupees ($5.6 billion) of long-term bonds, while selling 282.8 billion rupees of short-tenor debt.

Some participants say the authority may intervene less frequently in future as the budget provided relief to a market that has struggled in recent months.

“The need for operation twist is less, given that the market has stabilized and rallied,” said Naveen Singh, head of fixed-income trading at ICICI Securities Primary Dealership in Mumbai. The policy decision Thursday will be neutral for the bond market, he said.

The RBI “cannot turn dovish due to inflation and deficit worries, and it can’t take a hawkish turn owing to growth worries,” Singh said.

To contact the reporter on this story: Kartik Goyal in Mumbai at kgoyal@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Ravil Shirodkar, Karthikeyan Sundaram

©2020 Bloomberg L.P.