Winners Taking Everything in Relentless Five-Week Nasdaq Surge

Russell 2000 lags Nasdaq 100 by 7 percentage points in 2 weeks.

(Bloomberg) -- For a clear lens into how investors see the Covid crisis reordering the economy, consider how they are dividing the stock market’s bounty during what is fast becoming the rally’s most powerful stretch.

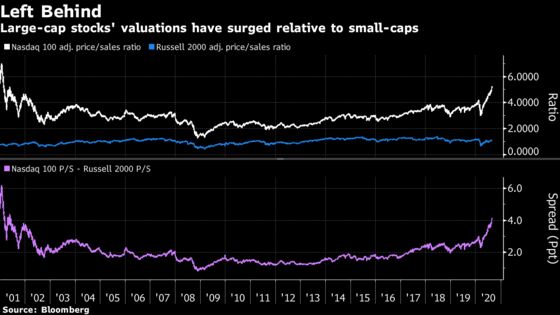

A five-month surge in the Nasdaq 100 just pushed one valuation measure -- the index’s price relative to the combined sales of its companies -- above 5 times, a level comparable to the dot-com bubble. On the other end of the luck spectrum are small caps, where pessimism about a broad-based economic rebound has held the ratio to 1/5th that, one of the widest gaps ever.

The rally’s been called a lot of things. Euphoria bred by stimulus, day-trader sentiment overtaking sense, falling discount rates boosting the net present value of future earnings. But its distinguishing feature has been constant: investors upping bets that the economy’s rewards will fall decisively on giant automation-enabled companies with fewer workers and hoards of cash -- while their smaller brethren fade.

“Winners continue to win,” said Lauren Goodwin, economist and multi-asset portfolio strategist at New York Life Investments. “That will continue to be the case as long as the virus is the dominant economic story.”

The Nadaq 100 climbed almost 4% in the five days ended Aug. 28, rising for a fifth week, the longest streak since January. The Russell 2000 added 1.7%, and has lagged the tech-heavy index by almost eight percentage points over the last two weeks.

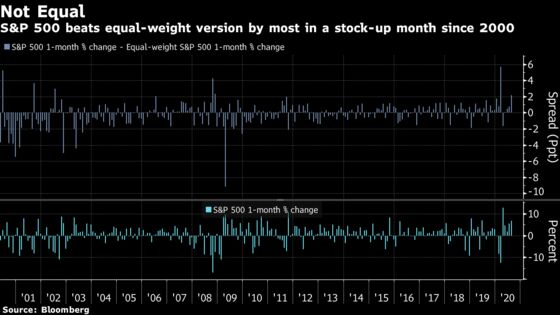

In another demonstration of megacap dominance, a version of the S&P 500 Index that strips out market-cap biases has gained 5.1% in August with one trading day left. The cap-weighted index is up 7.2%. According to Bloomberg columnist Cameron Crise, the gap is the widest for an up month in two decades.

Down 5.4% this year, the Russell 2000 trades at 1.1 times its companies’ sales over the last year, cheaper than what it fetched prior to the Covid-19 crash. Meanwhile, at 5.2 times sales, the Nasdaq 100 trades at the most expensive levels since the dot-com days. The ratio has risen from 3.8 at the start of the year. The widening gap is shorthand for the economic divide Covid has created.

In the three months ended in June -- a period in which the U.S. economy suffered its worst downturn in at least eight decades during strict virus lockdowns -- small companies saw their profits cut in half from the quarter prior, according to data from Jefferies LLC. The hit to S&P 500 company earnings was 20 percentage points less.

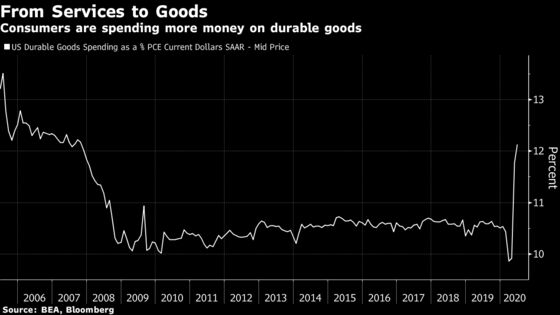

In the same period, sales for small-cap companies fell 17%, almost double the decline experienced by large-cap stocks. To Srinivas Thiruvadanthai, research director at the Jerome Levy Forecasting Center, the divide can be attributed to the nature of Covid-19 and the economy it’s created -- one driven by goods consumption with people cutting back on dining out and travel. The share of consumer spending focused on durable goods reached 12% in the second quarter, the highest in over a decade.

“That’s the scale of shift toward goods, and that tends to be all very large companies -- manufacturers of goods or sellers of goods, whether it is Amazon or Walmart or Home Depot or Lowe’s, and also the manufacturers of those goods,” Thiruvadanthai said in an interview on Bloomberg Television. “That’s the main thing here.”

Amazon.com Inc. is up 84% this year. Home improvement stores Lowe’s Cos. and Home Depot Inc. have both gained more than 30%, and shares of Walmart Inc. have risen 18%.

For a back-of-the-envelope view on what the widening valuation gap might be saying about the fate of large and small companies, consider what it would take to get the Nasdaq price-sales multiple back to normal.

Index members sport a combined market value of $13.4 trillion, roughly 5 times their annual sales. To squeeze the multiple back to historical normalcy -- say, 2.3 times sales -- their revenue would have to double to roughly $6 trillion a year. That’s a $3 trillion revenue grab that equates to half the domestic product of small business in America, at least according to the most recent SBA data, which dates back six years.

Pacific Life Fund Advisors, which has been under-weight small-cap stocks through the Covid crisis, is considering adding exposure, though. Max Gokhman, the firm’s head of asset allocation, points to metrics that are improving: Expected earnings growth for smaller companies is rebounding quicker than forecasts for large-cap profits, and measures of debt loads are lightening up.

“There are a few fundamental reasons for why, but one of the simplest macro reasons to tilt out of the year-to-date winners into the year-to-date losers is because if the market continues rallying past all-time highs, then small-caps and value will have to start catching up,” Gokhman said. “Conversely, if the market finally hits a wall and reverses, the styles that have not had the biggest gains are likely to also fall relatively less. That’s the kind of asymmetry we’re always looking for.”

For the year, returns in the Nasdaq and Russell 2000 are separated by more than 42 percentage points, a chasm in fortunes that will be all but impossible to ford in 2020.

©2020 Bloomberg L.P.