Wild Year in China Markets Ends With Record Defaults and Dull Yuan

Wild Year in China Markets Ends With Record Defaults and Dull Yuan

(Bloomberg) -- It was a bumpy year for China’s markets, considering all the turbulence in relations with the U.S. Still, the final results really aren’t bad.

The Shanghai Composite Index closed off its best year since 2014, boosted by a huge rally in the first few months, when the country’s major equity benchmarks entered a bull market. While the yuan was whipsawed at times by every twist and turn in the trade dispute, it’s only weakened about 1.3% the past 12 months. Sovereign bonds rose, but lagged bigger gains in government-bond markets elsewhere.

Economic worries in China took their biggest toll on corporate debt, with mainland firms setting a new high for bond defaults, exceeding 2018’s record tally.

Still, with the economy ending last year somewhat brighter, market watchers have some reasons for better days ahead. Here’s a look at what they went through over the past 12 months.

Solid Stocks

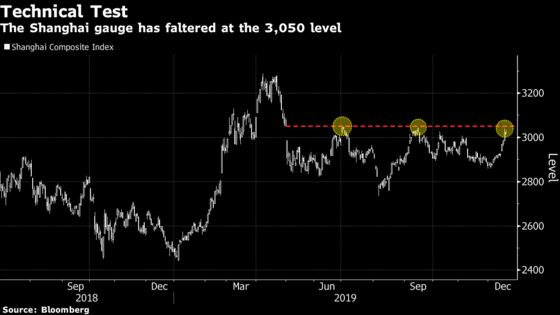

Despite the trade war, the Shanghai Composite Index rose 22% for its best performance in five years. Some of the excitement early in 2019 could be attributed to new chief securities regulator charming investors with his talk of reverence for the market. The launch of the new Star board in Shanghai was meant to be another highlight of the year, but investors quickly lost interest in that venue.

The party stopped in April, when policy makers signaled large-scale stimulus wasn’t in the works. It later suffered another blow with a pair of tweets from U.S. President Donald Trump, who threatened to boost tariffs on Chinese goods. Since then, the Shanghai Composite has struggled to climb over a technical level at 3,050 points several times. It closed Tuesday right at that mark.

Still, there’s a ray of hope for China stocks, at least if a survey of analysts and fund managers is to believed. Equities could climb in the first quarter of 2020, they said, citing optimism over the economy and easing trade tensions.

Yo-Yo Yuan

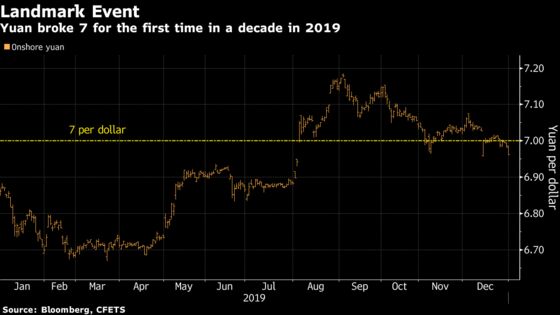

The yuan’s wild year ended almost right where it began. The currency’s drop in 2019 would be its smallest annual move in seven years.

The yuan has indeed had its share of drama. In August, the currency weakened past the key level of 7 per dollar for the first time since the financial crisis on concern the dispute between the world’s two largest economies would escalate. Then over the final quarter it gained about 2.6% as tensions eased amid an initial trade agreement.

Analysts predict the yuan will end 2020 at 7.1, according to the median forecast in a Bloomberg survey. That implies a drop of about 2% from the current level.

Boring Bonds

It wasn’t a good year for government bonds, even though 2019 marked the first inclusion of sovereign and policy bank debt into global indexes. The 10-year sovereign yield was stuck in its narrowest range since 2012, missing out on a global rally that took the world’s stockpile of negative-yielding bonds to $17 trillion. While central bank has tweaked multiple policies to support the country’s economy, it continues to signal that it will refrain from large-scale easing.

Elevated inflation and an incoming supply surge in 2020 are likely to keep weighing on the bond market. It may see some relief in the first quarter, when the central bank is expected to ease monetary policy to address a “liquidity hole.”

Defaults Rise

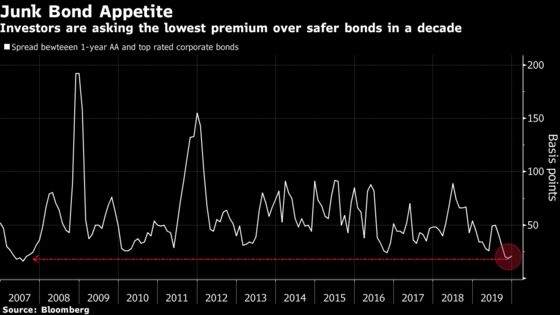

Hit by the economic slowdown, Chinese companies defaulted on 132.1 billion yuan ($19 billion) of domestic bonds last year, topping the prior record of 122 billion yuan in 2018. While China’s private companies made up a bigger proportion of China’s defaulters, state firms weren’t spared. Tewoo Group Co. recently became biggest dollar bond defaulter among China’s state-owned companies in two decades.

The record run of defaults has counter-intuitively proven to be a boon for the development of the nation’s junk bond market as investors engage in greater credit differentiation. That’s helped spark a rally for lower-rated debt.

--With assistance from Molly Dai, Livia Yap, Tian Chen and Tongjian Dong.

To contact Bloomberg News staff for this story: April Ma in Beijing at ama112@bloomberg.net

To contact the editors responsible for this story: Sofia Horta e Costa at shortaecosta@bloomberg.net, Kevin Kingsbury, Philip Glamann

©2020 Bloomberg L.P.

With assistance from Bloomberg