Wild Week Puts Wall Street on Notice: The Rout Isn’t Going Away

Stocks pinballed from surge to slump as investor fears over the coronavirus battled hopes over the policy response.

(Bloomberg) -- All week long, stocks pinballed from surge to slump as investor fears over the coronavirus battled hopes over the policy response. Fear gained the upper hand Friday.

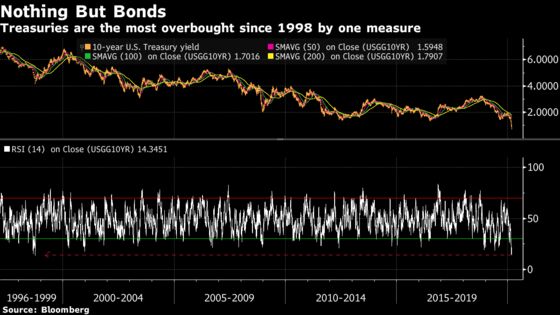

It was a day when the 10-year U.S. Treasury yield, already at unprecedented lows, at one point dropped more than 25 basis points to below 0.7%. The S&P 500 plunged as much as 4% before a closing rally cut that by half. Credit markets buckled after data showed cash fleeing corporate bond funds at the fastest ever pace.

This kind of drama, these types of falling dominoes across multiple asset classes, speaks to a market starting to act as if a recession might be in the offing.

“This is Minsky at work,” said James Athey, a money manager at Aberdeen Standard Investments in London, referring to the twentieth century economist Hyman Minsky, who described the process of an asset-price collapse. “It’s difficult to not sound too cataclysmic at this juncture.”

Crucially in this sell-off, the pessimism is infecting levels of the market beyond the main benchmarks.

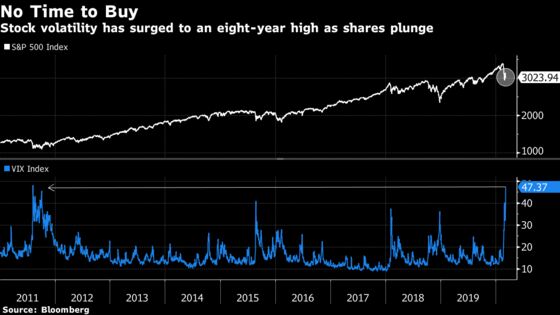

From America to Europe, inflation expectations have plunged to the lowest this century. The options market shows bets for stock volatility still rising even after they hit the highest since the 2011 euro debt crisis. Cracks are appearing in both credit and the interbank lending markets.

Against that backdrop, all talk from investors an analysts of V- or even U-shaped recovery is fading fast.

The Federal Reserve’s emergency interest rate cut on Tuesday, coming after the best day for U.S. stocks in more than a year, only sowed more seeds of doubt. That turned into fear toward the end of the week amid relentless virus headlines: The number of global cases surpassed 100,000 on Friday.

Minsky warned in his work that losses are in fact exacerbated by deceptively dull periods, and those who wish to see a pattern like that can find it in this year’s moves.

Even as China took extreme action to lock down tens of millions to control the virus in January, and the world began to fret over the spreading disease, U.S. stock volatility remained low, the S&P 500 rose to all-time highs and credit spreads were narrowing.

“The size of the volatility outbreak is directly a function of the complacency, mispricing and madness which had preceded it,” reckons Athey.

Following the Fed’s failed bazooka, and with little room for more easing at many of the world’s central banks, some argue markets are desperate for measures like fiscal stimulus or more drastic, coordinated efforts to contain the disease.

The bond market “forced the Fed already into an emergency cut,” said Dirk Thiels, the Brussels-based head of investment management at KBC Asset Management NV. “They’re probably trying to force governments into spending more money in the economy.”

The trouble is, governments rarely work like central banks. They can be conflicted by politics or constricted by fiscal limits. Their responsibility is not only economic health but also the literal health of the nation, meaning their priority is likely dealing with the virus itself and its human cost.

Although for some, that may also deliver the cure for the market’s ills.

“The antidote to this crisis, in my opinion as a citizen not as an expert, is to deal with the spread of the virus itself, not money printing or interest-rate cuts,” said Stephen Jen, chief executive officer at Eurizon SLJ. “With the passing of each day, the virus is spreading exponentially and the policy makers all have this blank stare.”

The trouble for markets is an analyst sitting in an investment bank -- or holed up in a home office -- can’t predict the impact on earnings or growth because they can’t model the rate of infections, and that makes the coronavirus a different kind of economic shock. Add in long-standing worries about the potency of monetary policy and investors are struggling to find a bull case for riskier assets.

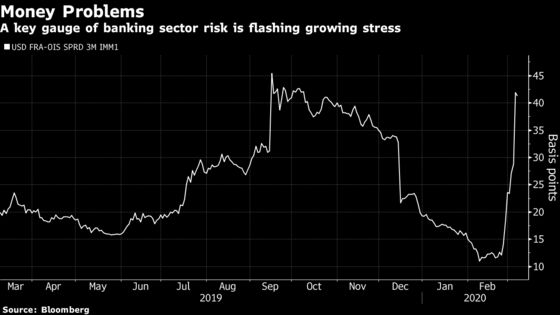

In the interbank lending market -- a crucial part of the global financial plumbing -- the spread between Libor and the Fed funds effective rate has spiked to the widest since the repo upheaval in September, a telltale sign risks may be building. The so-called TED spread, which is a measure of financial stress that compares funding costs for banks and the government, has also reached a 1 1/2-year high.

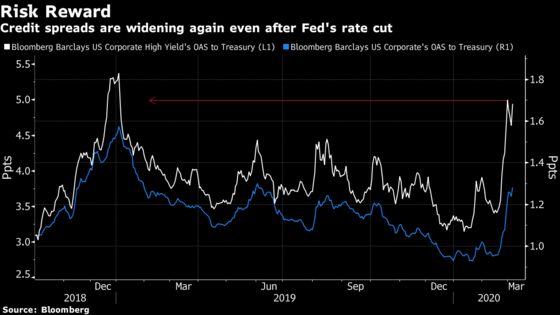

Meanwhile in corporate debt, spreads on the riskiest credit are widening to near a one-year high again. The premium on the highest-rated bonds has reached the highest since mid-2019.

All this pessimism across assets means investors are ditching stocks even as falling bond yields make equities more attractive. The S&P 500’s dividend yield is now the highest versus 10-year Treasury yield on record.

Thiels at KBC hopes the market is now pricing in a worst-case scenario, and that even when earnings and economic data drop, they will have a low bar to clear.

“We’re not far away from people expecting another financial crisis,” he said. “In a three-, four-, five-year horizon, it’s ridiculous to keep money in cash or to invest in bonds. There is really no alternative but equities, but you need some reassurance that the world economy is not falling off a cliff.”

--With assistance from Cecile Gutscher.

To contact the reporters on this story: Justina Lee in London at jlee1489@bloomberg.net;Anchalee Worrachate in London at aworrachate@bloomberg.net;John Ainger in Brussels at jainger@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Jeremy Herron

©2020 Bloomberg L.P.