Why Traders Are Taking a No-Deal Brexit Threat In Their Stride

Why Traders Are Taking a No-Deal Brexit Threat In Their Stride

(Bloomberg) -- With just three weeks to go, Britain is hurtling toward a no-deal Brexit and yet markets are decidedly sanguine on the looming economic shock.

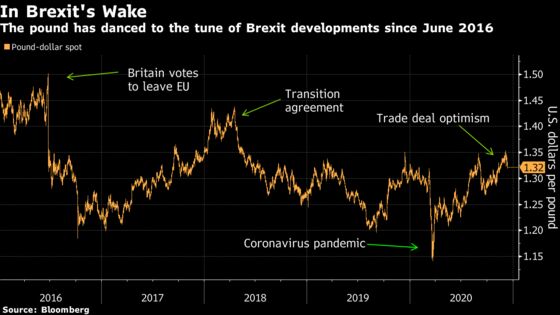

It’s a scenario that few imagined a year ago. Helped by dollar weakness, the pound isn’t far from the highest in two years and the FTSE 250 Index is down just 3% this week. The spread between French and Irish debt, a gauge of Brexit anxiety, is the narrowest since September.

At first blush, the relative resilience of U.K. markets is remarkable. Businesses and political leaders are warning of chaos -- from food shortages to days-long border lines -- if the country is forced to rely on World Trade Organization rules. Yet, plenty of investors are looking past the potential upheaval to supply chains and economic demand.

“We will move on from Brexit soon,” said Mark Nash, head of fixed income alternatives at Jupiter Asset Management. “When the market is already priced for a bare-bones deal, then there’s not much further to go.”

As anyone following Brexit negotiations knows only too well, nothing is certain. It’s unclear if Prime Minister Boris Johnson’s warnings to the public to prepare for no-deal are tough talk or the real deal. There’s still time for a trade settlement of sorts -- or officials could agree on a “friendly no-deal” that puts some contingency measures in place and keep talks going.

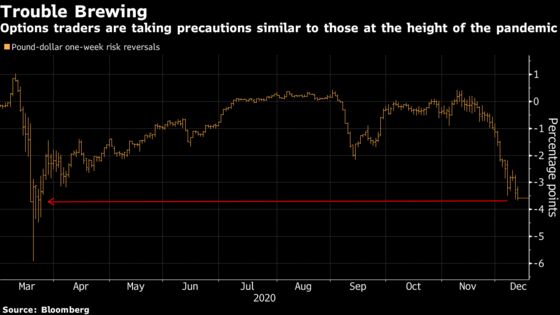

Yet the clock is ticking. No wonder there are flashes of fear in some market corners. Gilt yields tumbled this week as investors sought safer assets and the relative cost of hedging a weaker pound is at its highest since March.

Few are predicting the market collapse that would have once seemed possible. Here are some theories on why U.K. markets are holding up:

No-Deal Damage Already Baked In

One of the biggest reasons why investors say U.K. markets can largely absorb a no-deal Brexit without falling precipitously is that they’re already so cheap.

Equity valuations are at 30-year lows relative to the rest of the world on an analysis from Morgan Stanley that combines metrics include price-to-earning and price-to-book ratios.

The pound, the most Brexit-sensitive asset, is already some 4% undervalued against the euro this year, according to a measure of its purchasing power parity, with only the Japanese yen and the U.S. further down on the list of G-10 peers.

Economy in a Slow Burn

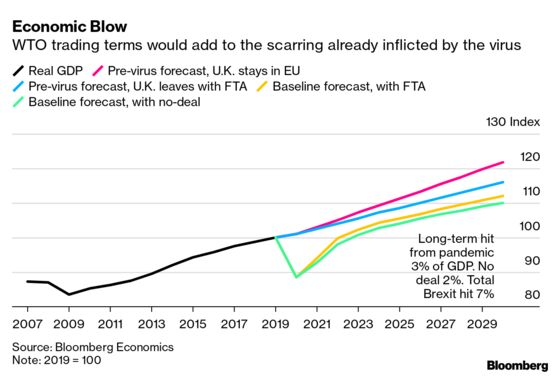

Of course, the no-deal fallout could feel less dramatic coming after a historic pandemic crunched the economy by the most in three centuries.

“It’s a bit more of a slow-burning economic impact,” said Simon Harvey, a foreign-exchange analyst at Monex Europe. “The pandemic obviously is a very large contracted economic shock to the point that it almost dwarfs somewhat the shock that Brexit will have.”

Trading on WTO terms could lead to an 8.1% reduction in gross domestic product over a decade, according to research group U.K. in a Changing Europe. Harvey expects a 6% to 8% fall in the pound to around $1.23 if there’s no trade deal. Prior to the pandemic, the currency forecast was below $1.20 in that scenario.

BOE Action

Investors can also count on the Bank of England for fresh help. It has already cut interest rates to 0.1% and relied on asset purchases to keep borrowing costs low. Policy makers could go further: BOE Governor Andrew Bailey said that the central bank has a lot of tools in its armory and officials are doing extensive work on the impact of negative rates.

Earlier this month, two other policy makers on the rate-setting committee indicated they were open to using negative rates in the future. And this week, money markets have moved forward bets for a cut in the BOE’s benchmark rate to zero.

Foreign Money Has Already Left

Another theory is that foreign traders have largely exited the U.K., leaving domestic investors that are more likely to sit on their holdings. According to Bank of America Corp.’s latest fund manager survey, the U.K. is the world’s biggest underweight.

Brexit Fatigue Is Real

Elsa Lignos, global head of foreign-exchange strategy at RBC Europe Ltd., sums up a sentiment held among many of her currency-watching peers:

“The pound is notable overnight for not being the worst performer,” she said.

“How to explain this? 1. Brexit fatigue surely plays a role (we may have lost half our readers just by kicking this note off with Brexit). 2. Also high is an expectation that this is all part of the set-up for a ‘Christmas miracle’, both in markets and the media. 3. And in some quarters, there is a feeling WTO-only, aka the euphemistic ‘Australian solution’ is no big deal.”

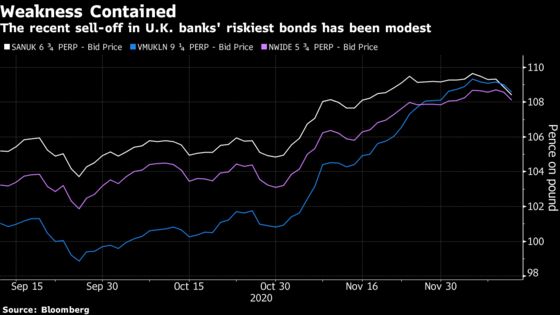

Bank Resilience

The capital strength of U.K. lenders may help curb a selloff in their bonds, since it puts them in a better position to weather the economic pain.

That’s reflected in the BOE’s decision to ease a ban on dividends since lenders are “resilient to a wide range of economic outcomes,” it said. The sector’s average Common Equity Tier 1 capital ratio -- a key measure of strength -- is 15.7%, according to central bank data, higher than the 14.9% European average.

But Markets Are Still in Danger

Yet for all that, a no-deal scenario would still inflict cross-asset damage, spurring many to hedge in the derivatives market.

Morgan Stanley strategists led by Graham Secker spelled out the risks in a Friday note:

“We believe that there has been a healthy consensus that a no-deal Brexit would be avoided. In fact, the idea of such an outcome has been absent in almost all of our investor conversations this year. Although there may still be grounds for a last-minute compromise, investors now need to consider the prospect of a genuine and negative (in market terms) ‘surprise.’ We suspect investors and markets more generally are relatively unprepared for such an eventuality, not least because the longer-term ramifications are unclear and complex.”

©2020 Bloomberg L.P.