Why It’s So Hard to Overthrow the Mighty U.S. Dollar

The U.S. dollar is on one side of almost 90% of foreign-exchange transactions and accounts for two-thirds of international debt.

(Bloomberg) -- As the coronavirus outbreak reached pandemic status, people began panic buying staples: rice, pasta, noodles — and the U.S. dollar. The demand was so intense that the U.S. Federal Reserve stepped in to help foreign central banks and others get their hands on the greenback in March. It was a similar situation as during the 2008-2009 financial crisis, when calls grew louder for an end to the global dominance of a single currency. Yet, just over a decade on, the dollar still reigns supreme.

1. Why are some people fed up with the dollar?

Because of its sheer prevalence. The U.S. currency is on one side of almost 90% of foreign-exchange transactions and accounts for two-thirds of international debt. Virtually all international trades in oil are priced in dollars. Jean-Claude Juncker, the former president of the European Commission, said it was “absurd” that 80% of Europe’s energy imports are priced in dollars. The greenback’s ubiquity makes nations beholden to fluctuations in its value, ties their economies to decisions made in Washington and serves to amplify dangerous shocks to the financial system, like the one triggered by the pandemic.

2. How does that happen?

When the financial world is teetering, investors view the U.S. currency as the safest haven, even more so than gold, the yen or the Swiss franc. As the grim economic implications of the virus outbreak strained markets in March, demand for the dollar soared, pushing other currencies lower. Countries with significant debt denominated in dollars suddenly faced higher repayments just as they were confronted with looming recession. Banks — wary of lending to other banks during the eye of a financial storm — started hoarding the greenback, pushing gauges of funding stress to their highest levels in more than a decade. It was the Fed’s actions that prevented dollar shortfalls turning into currency crises.

3. Are there other drawbacks for some countries?

Ask Iran and Russia. The central role that U.S. banks and the dollar play in the global economy means that American politicians can exert leverage by imposing sanctions on countries, people or companies. Violators might see their American-based assets blocked or lose the ability to move money to or through accounts held in the U.S. A spate of such penalties pushed Russia to target faster “de-dollarization.” As President Vladimir Putin put it: “We aren’t ditching the dollar, the dollar is ditching us.”

4. Is dollar concern a new thing?

The U.S. currency has dominated since the end of World War II, when world leaders met at Bretton Woods, New Hampshire, to establish a system to manage foreign exchange and linked their currencies to the dollar. The push to dial back the greenback has its origins partly in the 1998 currency crisis, when Asian nations got caught borrowing too many dollars and were plunged into recession. Fast forward a decade, and Asia’s amassing of dollars to build currency reserves helped fuel a U.S. credit binge that triggered the sub-prime mortgage crisis.

5. Is the dollar’s influence shrinking?

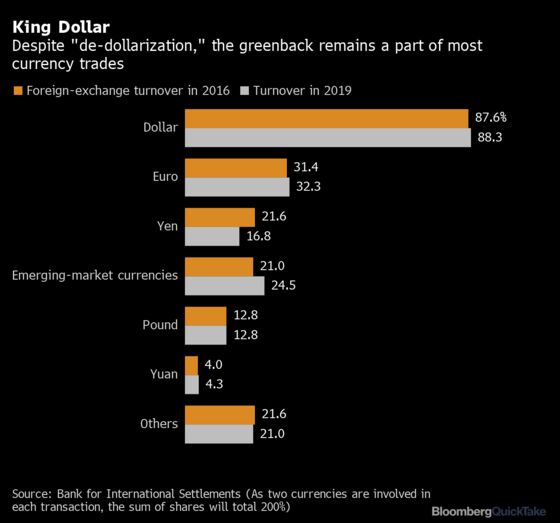

Hardly. The share of currency trades in dollars increased to 88.3% in 2019 from 87.6% in 2016, according to the Bank for International Settlements. The proportion of foreign reserves held in dollars has remained steady around 60% over the past decade. The currency’s usage in global payments tracked by financial institutions has risen since 2010. And credit extended to non-banks in dollars more than doubled over a decade to a record $12.1 trillion by September 2019.

6. Why is it hard to compete with the dollar?

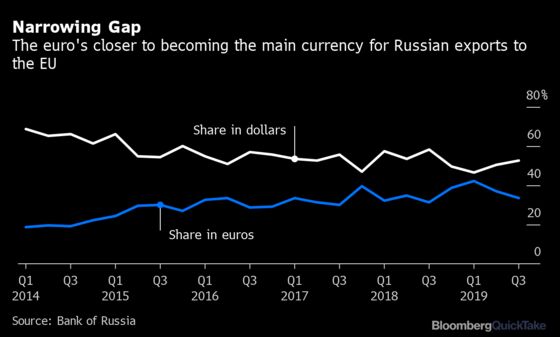

Any move away from the greenback involves bother and expense. Shifting to the euro, yuan or ruble means higher costs and difficulty finding banks to handle business. Faced with U.S. sanctions, Russia has succeeded in loosening the dollar’s grip. The country now has a higher share of reserves in euros (30%) than in dollars (23%). The euro has also overtaken the dollar as Russia’s main currency in trade with China and is close to doing the same in trade with the European Union. But diversification comes with perils attached: When the dollar rallied in March, the value of Russia’s international reserves plunged by 5% in a week.

7. Can any currency take on the dollar?

There’s certainly a will. Putin said using the dollar as an instrument of pressure was “undermining its role as a global reserve currency.” Chinese President Xi Jinping more obliquely described “hegemonism” as a global challenge. Still, the yuan accounted for just 4% of currency trades in 2019 after China shifted its focus from turning it into a freely convertible currency without government restrictions to promoting it as a reserve currency and stable asset in times of stress. The euro, which was involved in 32% of foreign-exchange transactions in 2019, is the only currency that comes anywhere close to the dollar, but its allure was undermined by the region’s 2010 sovereign debt crisis and the European Central Bank’s use of negative interest rates. Former Bank of England Governor Mark Carney says it would be a mistake to switch one dominant currency for another; he advocates a global digital currency to supersede the dollar.

The Reference Shelf

- Click here for QuickTakes on the coronavirus outbreak.

- Swap lines: How the Fed eased pressure for dollars.

- How the dollar’s dominance amplifies crises.

- How Russia got punished for diversifying.

- Emerging-market central banks see reserves dwindle.

- A BIS survey underlines the dollar’s ubiquity. A BIS analysis of dollar hoarding.

- A Functions for the Markets article on yuan bonds’ appeal in the coronavirus crisis.

©2020 Bloomberg L.P.