Why Investors Will Still Flock to Negative-Yield Japan Bonds

Why Investors Will Still Flock to Japan's Negative-Yield Bonds

(Bloomberg) -- The return of dovish central banks is putting Japan’s negative-yielding government bonds back on the investment menu for global funds.

Overseas investors bought 638.3 billion yen ($5.8 billion) of Japanese bonds in five days through Feb. 1, the most in three weeks, Ministry of Finance data showed Thursday. In more evidence of buoyant appetite, an auction of 10-year JGBs Tuesday drew the strongest demand in 13 years, followed by an upbeat 30-year sale two days later.

The dovish pivot from other major central banks has lessened concerns about a widening yield gap between Japan and its developed peers, with risks to global growth further supporting a bond rally. While JGBs have negative or close to zero yields, investors are still able to make juicy returns by swapping foreign currencies into yen and then investing the proceeds into the debt.

“Foreign demand will remain robust this year, especially for futures and shorter maturities, thanks to basis swaps,” said Naoya Oshikubo, a senior economist at Sumitomo Mitsui Trust Asset Management Co. in Tokyo.

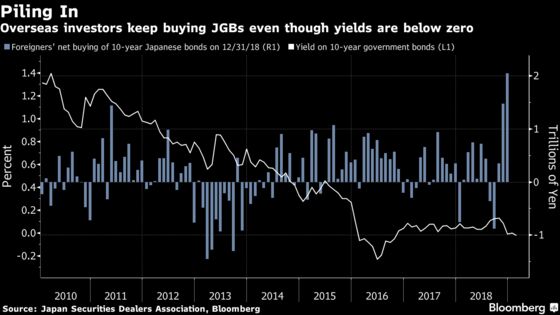

Global funds purchased a net 2.04 trillion yen of long-term JGBs in December, a record in data from the Japan Securities Dealers Association going back to 2004. The use of swap transactions that lock in exchange rates enables them to earn more from Japan’s bonds -- which offer the lowest yields globally after Switzerland -- than they do from Treasuries.

For example, the effective yield on five-year JGBs, at 2.95 percent, offers 50 basis points of incremental carry above nominal similar-maturity U.S. Treasuries.

Friday’s Rally

Japan bonds rallied with their Asian peers on Friday as Australia’s central bank cut its growth and inflation forecasts, following a move Thursday by the European Commission to slash its expansion estimates for all the euro region’s major economies.

New Zealand’s 10-year bond yield slipped to a record low, while Australia’s benchmark declined by as much as 8 basis points. The 10-year JGB yield touched a five-week low of minus 0.035 percent.

It will be “quite challenging” for Japan’s 10-year yield to rise above 0.1 percent, said Akio Kato, general manager of trading at Mitsubishi UFJ Kokusai Asset Management Co. in Tokyo. He sees a level of minus 0.05 percent as a floor.

‘Safest Trade’

Rising global growth concerns will support demand for Japanese bond futures, Oshikubo said. “There will continue to be foreign appetite for JGB futures as an arbitrage for shorting stock futures in a move similar to the one seen late last year,” he said.

Basis swaps have also helped turn Japanese bills -- which are trading at even deeper negative rates -- into a lucrative proposition for dollar lenders, prompting them to pile into the securities.

“Short-dated JGBs are extremely attractive for foreigners,” said Shinji Kunibe, head of fixed income at Daiwa SB Investments Ltd. in Tokyo. “It’s the safest trade if there aren’t constraints on their balance sheets.”

Such overseas demand may prove crucial in helping maintain a balance in Japan’s money flow this year given odds that negative yields at home and the yen’s strength could prompt local investors such as life insurers to chase returns beyond the nation’s shores.

With U.S. yields clearly peaking and the European Central Bank unlikely to raise rates this year, overseas demand will be key to determining how low Japanese yields drop, Kunibe said.

The Bank of Japan’s policy of pinning 10-year rates near zero means foreign demand for JGBs will strengthen, particularly as the Federal Reserve and the ECB are turning dovish, according to Nomura Securities Co.

“While the U.S. curve is flattening rapidly, the BOJ’s yield-curve control ensures a spread between the policy rate and the 10-year yield,” said Takenobu Nakashima, senior rates strategist at Nomura in Tokyo. “As long as there is a relative curve steepness, JGBs hold priority and their appeal for foreigners remains intact.”

To contact the reporters on this story: Chikako Mogi in Tokyo at cmogi@bloomberg.net;Kazumi Miura in Tokyo at kmiura1@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Shikhar Balwani

©2019 Bloomberg L.P.