Why Invest in an Investment Manager?

Why Invest in an Investment Manager?

(Bloomberg Opinion) -- As Europe’s fund management companies polish their PowerPoint slides before they update the markets about their third-quarter performance, their shareholders should ask themselves this question: Why invest in an investment firm?

The list of challenges the industry faces is daunting. The flood of money into low-cost exchange-traded funds continues unabated, putting downward pressure on the fees investors will tolerate for actively managed funds. The burdens of regulation are growing ever heavier: improved data-privacy standards; cybersecurity; and the push to make the industry, rather than its customers, foot the bill for market research have all pushed costs up.

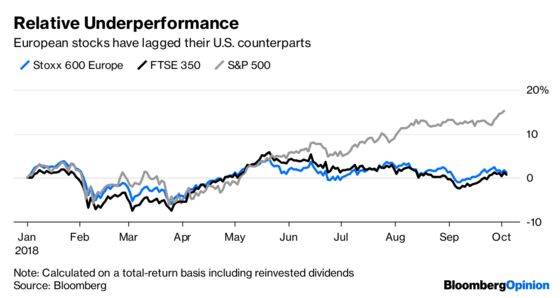

Markets aren’t helping. Returns from European equity markets have trailed those of their U.S. counterparts. The Stoxx 600 Europe index is roughly unchanged for the year, while the S&P 500 index is up 15 percent, with dividends reinvested.

European investors scanning this year’s returns from their portfolios are unlikely to rush to put more money to work. Analysts at UBS Group AG estimate that Amundi SA, Europe’s biggest fund manager, grew its 1.3 trillion euros ($1.5 trillion) of assets under management by just 0.7 percent in the third quarter from the second; they predict the same growth at DWS AG, but see Jupiter Fund Management Plc’s assets shrinking by 0.5 percent in the past three months.

In the febrile market for passive products, index trackers in Europe are replicating the success that the market has enjoyed in the U.S. in recent years. The cash allocated to ETFs in Europe is poised to top $800 billion for the first time, with the market doubling in the past five years.

But building an ETF business is far from a guaranteed route to riches amid a race to the bottom in what to charge investors for the products. DWS, for example, trimmed the fees on several of its Xtrackers ETFs, with the charges on one product that tracks the MSCI Europe index more than halving to 0.12 percent.

DWS said it was passing on the benefits of economies of scale as its ETF business grows; but the bottom line is that competition will only intensify and fee income from ETFs will diminish.

And while no one in Europe has yet followed Fidelity Investments’ move to open funds that charge zero fees to investors, it can only be a matter of time. “Cheap is great, but free is irresistible,” as my Bloomberg Opinion colleague Nir Kaissar wrote when the move was announced in August. And as billionaire hedge-fund manager Cliff Asness said in a profile published by Bloomberg Markets this week, “The trend in passive index fund fees is inexorably toward zero.”

So what will remedy the fund management industry’s ailments? The most oft-touted antidote, industry consolidation driving mid-sized fund managers to the M&A altar, hasn’t materialized — with a handful of notable exceptions, including the mergers that created Standard Life Aberdeen Plc and Janus Henderson Group Plc.

“Thank goodness we’re ahead of the curve,” SLA’s co-Chief Executive Officer Martin Gilbert said in August. It was a tacit acknowledgement that the then 25 percent drop in his share price since the merger was announced in August 2017 — a decline which has since accelerated to more than 30 percent — could have been much worse if he hadn’t done the defensive deal.

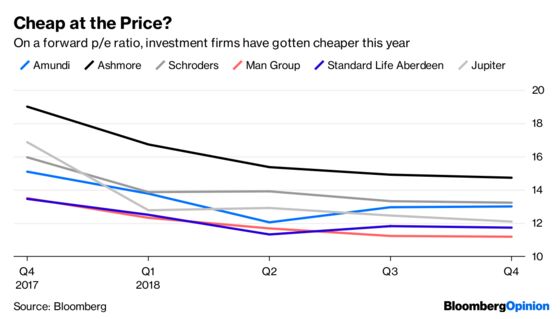

As the chart above suggests, investment firms look cheap at their current valuations. With the pressures that have driven down their share prices unlikely to abate any time soon, it’s possible the urge to merge will finally consume investment firms. But in the absence of that, there’s little incentive for investors to hang around for an increasingly bumpy ride.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.