Who's Really Getting Paid in the Oil Sector

Who's Really Getting Paid in the Oil Sector

(Bloomberg Opinion) -- Owning oil and gas stocks has been an exercise in masochism for the past few years:

Running an oil and gas company can’t have been the best time either. But the pay helped — a point that hasn’t been lost on investors.

Short-term incentives — typically cash bonuses — are particularly in focus, said Chris Crawford, president of compensation consultant Longnecker & Associates. (Long-term incentives often come in the form of restricted stock or something similar, which generally align more closely with shareholders’ experience.)

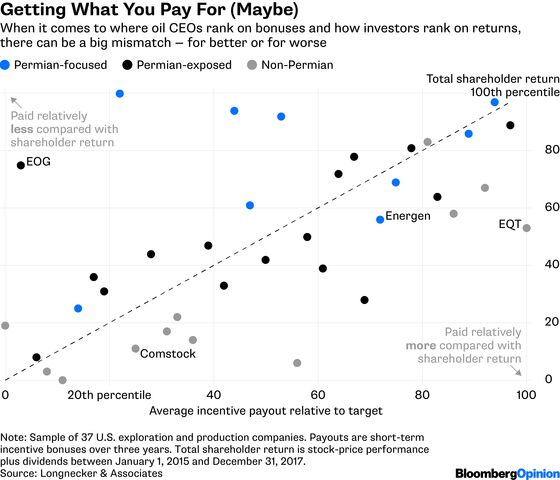

Longnecker surveyed 37 exploration and production companies for the three years ended December 2017. With market caps ranging from a hundred million dollars or so to tens of billions, comparing absolute CEO pay doesn’t work. Instead, Longnecker looked at the average percentage of the target bonus that was paid to each company’s CEO over the period. Typically, a target bonus is set and the actual one paid is higher or lower depending on whether various objectives were met, exceeded or missed. The companies were then ranked by how generous they were compared with where they ranked on total shareholder return:

Toward the top left is shareholder paradise, with relatively high returns but relatively modest bonus payouts; the opposite corner is less desirable. About a third of the companies hug that diagonal line pretty closely, meaning returns and bonus levels are more aligned, in relative terms. Companies like EOG Resources Inc. look extremely attractive while the likes of EQT Corp. — which was targeted by activists and whose CEO resigned in March — less so.

One point that jumps out is that companies focused on the Permian basin generally screen much better, especially compared with those with no exposure.

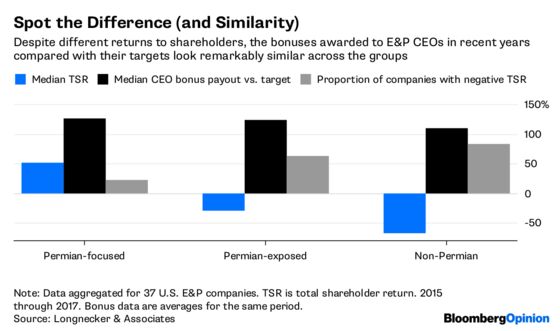

While it’s too simplistic to praise or condemn each company based on this snapshot, the vast differences in relative returns compared with the striking similarity in bonus payouts across the subgroups is exhibit A for why short-term incentives are receiving attention.

As a whole, only 15 of these 37 companies generated a positive shareholder return during the period. On a relative basis, only 17 beat the SPDR S&P Oil & Gas Exploration and Production ETF, and just six beat the SPDR S&P 500 ETF Trust. Yet 30 of them paid their CEOs at least 100 percent of their target bonus on average during the period.

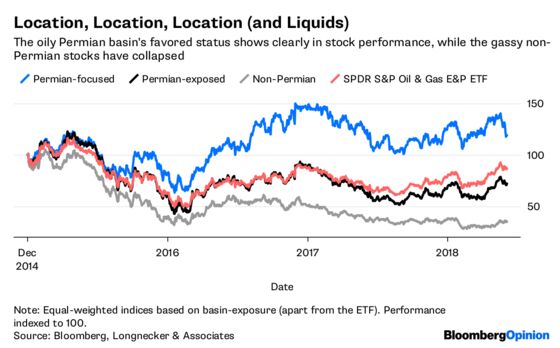

The primary culprit is a historical focus on growth over returns. This features prominently, for example, in the bonus criteria of Comstock Resources Inc., which I profiled here the other day and, you’ll notice, sits in that less desirable half of the graphic above. Last year, fully 60 percent of Comstock’s CEO bonus was tied to growing reserves and production, chiefly of natural gas — not a market exactly crying out for more supply. It is notable that for the benighted non-Permian group, 70 percent of its production last year was lower-value natural gas, according to figures compiled by Bloomberg.

That has worked differently for the Permian-focused companies because, even if they incentivize growth, it has been into a recovering oil market (only 25 percent of their output is natural gas, on average), often twinned with falling costs. Using Longnecker’s survey group, these indices constructed on the Bloomberg Terminal illustrate the stark differences in how the three groups have performed over the past few years:

One thing worth noting is that sharp recent dip in the Permian-focused stocks. Investors are fretting about the discounts being taken on barrels there as surging production runs into logistical bottlenecks.

The point is that focusing on growth can come back to bite anyone in this most capricious of markets. All E&P companies — gassy or Permian-based, or whatever — can benefit from a greater focus on value rather than volume (notably, this is the case with EOG.) Because if virtually every CEO is getting paid while a minority of companies are generating positive returns, those wordy explanations in the proxy of how bonuses are set start to read more like “LOL! Who cares?”

-- Elaine He assisted with graphics

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

©2018 Bloomberg L.P.