Rising Rates See Traders Mull Trigger Point for Stock Upset

Trigger Point Looms for Rising Yields to Upset Risk Asset Run

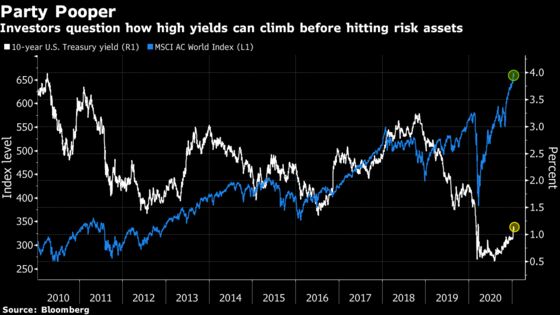

(Bloomberg) -- As benchmark Treasury yields rise amid expectations for stronger growth, the key question on investor minds is how high can they climb before spoiling the global risk-asset rally.

Some such as JPMorgan Asset Management worry about the pace of the ascent, while others are focusing on breaches of levels from 1.3% to 1.6%, areas last seen in early 2020. The 10-year yield traded just above 1.1% Friday after details of President-elect Joe Biden’s Covid-19 relief package of $1.9 trillion were released.

“If we look at historical volatility in the 10-year yield, as well as borrowing the example of 2013 taper tantrum, I think a 30-50 basis point rise in yields over two to three weeks could potentially add to market pressure,” said Tai Hui, JPMorgan Asset’s chief Asia market strategist. “Government bond yields rising too fast can be problematic for financial markets.”

The global bond benchmark touched 1.19% this week, its highest since the pandemic-induced market rout in March, as traders bet the rollout of vaccines and Democratic control of the U.S. government boosted the odds of further stimulus and higher inflation. That caused ripples in a number of markets, with bonds selling off, the under-pressure dollar rebounding and its emerging-market counterparts pulling back from recent highs.

The moves brought back memories of 2013’s so-called taper tantrum, when yields surged on the disclosure the Federal Reserve was considering dialing back asset purchases, leading a jump in volatility in financial markets.

| Related stories |

|---|

Treasury 10-Year Yields Can Reach 2% This Year, Citigroup Says What’s Next for Markets After 10-Year Yields Climb Back to 1% Fed Officials See Strong U.S. Rebound, Fanning Talk of Taper Treasury Yields Look Ominous for Emerging-Market Stock Rally Higher Yields to Have Minor Impact on Risk Assets: Wellington |

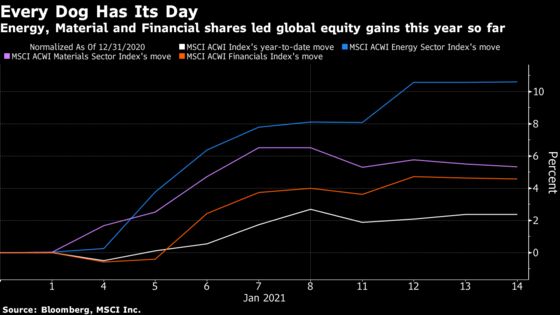

So far, global stocks have taken the rise in yields in stride with the MSCI AC World Index remaining close to its all-time high reached this month. But underneath the surface, investors have been rotating into energy, financials and cyclical stocks, seen as more exposed to an economic recovery, and are less enthusiastic about once market-leading technology shares.

Kieran Calder, head of Asia equity research at Union Bancaire Privee Ubp SA, said 10-year Treasury yields moving to the 1.2% to 1.3% levels would still be supportive of equities in general, though it may prompt investors to “gradually re-introduce” longer-dated bonds to cushion risk-asset exposure.

“Assuming inflation stabilizes near 2%, then 1.2% to 1.3% would leave inflation adjusted yields still below the pre-pandemic range consistent with the Fed’s desire to retain an accommodative stance,” he said.

Real Deal

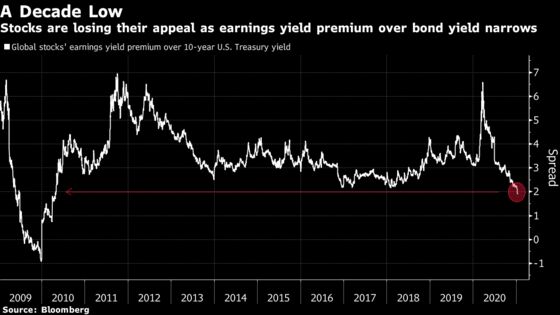

For many market participants, inflation is the key factor and that means watching real yields, not just nominal ones.

“The most common incoming client query I continue to receive is at what point will equities no longer be able to handle higher real rates,” Charlie McElligott, a Nomura Holdings Inc. strategist, wrote in a note this week.

Though higher real rates at this juncture are not an issue for stocks, the likes of a big upside surprise on inflation could trigger an “unruly” rates selloff or gap higher in yields, that may require further intervention from the Fed to calm financial stress, he said.

Strategists at Citigroup Inc. including Amir Amin say holding onto risk assets until the four-week change in real yields reached 40 basis points is a “reasonable” approach.

The so-called breakeven rate on 10-year Treasuries -- a gauge of expected inflation -- climbed above 2% this month to the highest in more than two years. The “real yield” -- that on 10-year inflation-protected Treasuries -- was at minus 1% Friday, up from a low of minus 1.12% at the beginning of January.

Emerging Scare

Emerging-market investors are watching yields particularly closely given the sensitivity of that asset class to Treasuries.

Mizuho Bank Ltd. strategist Vishnu Varathan sees benchmark yields in the 1.6% to 1.8% range -- higher than pre-pandemic levels -- as enough to cause a “proper scare” for investors in developing nations.

“The steeper yield curve and higher nominal Treasury yields will victimize emerging markets with high inflation -- as the loss of real yield differential advantage will be felt,” he said.

| Related stories |

|---|

TD, Morgan Stanley Add Short Rupiah Trades on Rising U.S. Yields Quants Ditch Treasuries Amid Battle Over How High Yields Can Go Treasury Yield Spike Risks Sparking Domino Effect in Markets |

Some in the currency market are not waiting for yields to move much higher before acting. Last week’s 20 basis points jump in Treasury yields, the most since June, has spurred firms including TD Securities and Morgan Stanley to recommend emerging-market trades such as shorting the Indonesian rupiah to clients.

Status Quo

Still, many investors remain positioned for moderate levels of inflation that would allow the Fed to keep rates low, despite chatter about tapering. The central bank signaled last month interest rates would stay near zero at least through 2023.

The current market environment -- an improving growth outlook, stable inflation and supportive global policy -- is unlikely to lead to a sharp spike in yields that could suffocate risk assets, said Ricky Chau, a portfolio manager at Franklin Templeton Investment Solutions. The asset manager still favors risky assets and has a one-year target of 1.3% on 10-year Treasury yields.

Reasons Matter

For Thomas Poullaouec, T. Rowe Price’s head of multi-asset solutions, the driver of rising bond yields matters more than levels.

“If yields increase because of a reflationary environment, this should not pose a problem for risky asset investors,” said Poullaouec. “If the yield increase is due to a change in monetary policy, this would be more negative for risk assets.”

©2021 Bloomberg L.P.