When Good Trade Talk News Eclipses Bad Macro Data: Taking Stock

When Good Trade Talk News Eclipses Bad Macro Data: Taking Stock

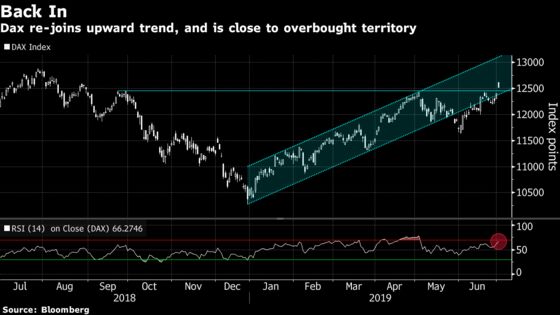

(Bloomberg) -- The restart of U.S.-China trade talks has sent Germany’s DAX back into a bull market, completely eclipsing yesterday’s poor manufacturing data. But a number of strategists question whether the revived rally will stretch beyond the short term, as economic growth stutters and the U.S. is already back on the trade war front, this time with potential tariffs on EU goods.

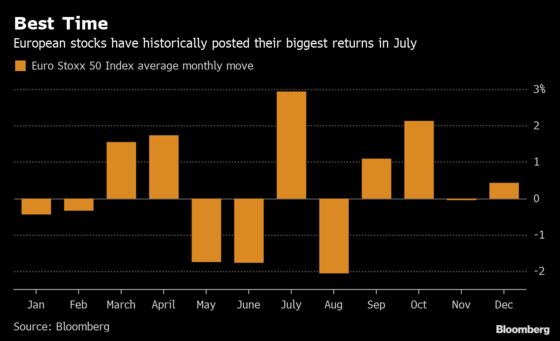

We are entering what is traditionally the best month for the Euro Stoxx 50. The gauge has climbed 2.9% on average in July over the past decade, rising in all but two of those years. One notable difference though: June was unusually good this year, and European stocks just posted their best half-year since 1998.

The export-heavy German DAX has returned to its upward trajectory, spurred by trade optimism after the G-20 summit. There is no reason to be short on the German index, says Andy Dodd, a technical analyst at Louis Capital Markets.

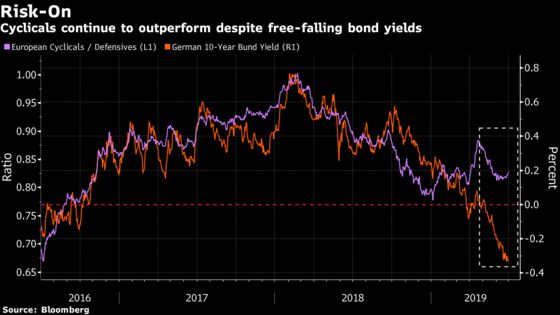

Before the tariff truce, the change of tone from central banks had already boosted stocks. Looking at the chart below, cyclicals’ relative performance to defensives has mostly ignored plummeting bund yields, opening a significant gap. Yesterday’s jump in basic resources, technology and oil stocks, while utilities, food and telecoms shares lagged, could enhance that trend.

Still, the G-20 announcements were taken with a pinch of salt by a number of strategists who only see a short-term relief rally. And then there is the latest PMIs. China’s manufacturing gauge hasn’t picked up, while Europe’s was mostly gloomy.

The question remains: for how long can stocks shrug off the poor macro data? JPMorgan strategists say the activity indicators are near lows right now, and are likely to look better in the second half of the year. This, combined with easing central banks and a weaker dollar, is enough to stay bullish on equities, they say.

Unsurprisingly, 75% of investors say the U.S.-China trade situation is the key driver of equity prices over the next three months, according to a Citi poll. Which means as long as the trade newsflow is on the positive side, other factors could be eclipsed.

In the meantime, Euro Stoxx 50 futures are trading up 0.2% ahead of the open.

- Watch Airbus and its suppliers on Tuesday after the U.S. proposed a series of further tariffs in a long-running subsidy dispute involving the plane maker and its U.S. rival Boeing. Watch engineers like Rolls-Royce Holdings, GKN-owner Melrose Industries, Safran and MTU Aero Engines; also Jenoptik and IT systems maker Sopra Steria.

- Watch oil stocks after crude prices pulled back from the five-week highs it hit on Monday, despite a nine-month extension to output cuts, as the fundamental drivers for higher prices clashed with weakening economic sentiment.

- Watch Italian banks and sectors sensitive to moves in the country’s government bonds after the government lowered its 2019 budget deficit in a bid to avoid EU sanctions for failing to rein in its debt. Watch UniCredit, Intesa Sanpaolo, Banco BPM among others.

- Watch Hong Kong-exposed stocks as pro-democracy protests ramped up on Monday. Watch luxury-goods merchants and Asia-exposed banks like HSBC and Standard Chartered, both of which underperformed on Monday.

COMMENT:

- “European equity compares favourably to the Japan of today: the cash yield is c.100bp higher in Europe, the demographics are slightly less negative, and sales growth and ROE are higher,” Goldman Sachs strategists write in a note. “But Japan is restructuring and Europe’s economy remains stymied by a lack of policy flexibility.”

COMPANY NEWS AND M&A:

- U.S. Proposes More Tariffs on EU Goods in Airbus-Boeing Spat (2)

- AB InBev Asia Unit Sets Terms for $9.8 Billion Hong Kong IPO

- Deutsche Bank Discusses Lowering Its Capital Buffer (Correct)

- WPP Confirms Exclusive Talks With Bain for Stake in Kantar

- Telecom Italia Set to Tap EUR 2.5B Loan for Vodafone Deal: Rtrs

- Key Swedbank Shareholder Confident Board Can Rebuild Confidence

- Credit Suisse International Wealth CEO Exits; Wehle Promoted

- Publicis Says Epsilon Acquisition Positive for Shareholders

- Elior Completes Sale of Areas to PAI Partners for EU1.4B Net

- PostNL-Sandd Merger Gets No Approval From ACM: Telegraaf

- Stadler Rail Wins EU600m German Deal, Objection Period Expired

- Intelsat C-Band Plan Gets Counter Proposal From Charter, Groups

- Grenke First Half Leasing New Business CM2 EU233 Mln

- Covivio Buys 32% Stake in Portfolio of Accor Hotels for EU176M

- Cembra Money Bank Places 1.2m Shares at CHF94 Apiece

NOTES FROM THE SELL SIDE:

- Auto Trader has continued to be resilient in challenging times for the car market, with innovation and new products supporting revenue growth, but the stock looks fully valued, Peel Hunt says in note as it cuts to hold from add.

- Intertek EPS estimates are boosted 3%-6% by Jefferies on reduced concern over trade wars and more confidence in Ebita boost driven by Alchemy, putting the broker 1% ahead of consensus for FY19 and 4% ahead in FY20. PT lift to 5,900p.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 392.7 (July 2018 high); 397.9 (May 2018 high)

- Support at 381 (50-DMA); 374.5 (61.8% Fibo)

- RSI: 64.3

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,514 (May high); 3,596 (May 2018 high)

- Support at 3,410 (50-DMA); 3,403 (61.8% Fibo)

- RSI: 67.2

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Anima upgraded to outperform at Mediobanca SpA; PT 4.50 Euros

DOWNGRADES:

- Adidas downgraded to hold at HSBC; PT 300 Euros

- Auto Trader downgraded to hold at Peel Hunt

INITIATIONS:

- None reported.

MARKETS:

- MSCI Asia Pacific up 0.9%, Nikkei 225 up 0.1%

- S&P 500 up 0.8%, Dow up 0.4%, Nasdaq up 1.1%

- Euro up 0.02% at $1.1288

- Dollar Index down 0.05% at 96.79

- Yen up 0.07% at 108.37

- Brent up 0.3% at $65.2/bbl, WTI up 0.1% to $59.1/bbl

- LME 3m Copper down 0.1% at $5947/MT

- Gold spot up 0.5% at $1391.2/oz

- US 10Yr yield down 1bps at 2.02%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) May Budget Balance YTD, prior -67.2b

- 9am: (SP) June Unemployment Change, est. -90,000, prior -84,075

- 10:30am: (UK) June Markit/CIPS UK Construction PMI, est. 49.2, prior 48.6

- 11am: (EC) May PPI MoM, est. 0.1%, prior -0.3%

- 11am: (EC) May PPI YoY, est. 1.7%, prior 2.6%

* For a daily wrap on developments in European equity capital markets, click here

--With assistance from Jan-Patrick Barnert and Namitha Jagadeesh.

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Jon Menon

©2019 Bloomberg L.P.