What Market Strategists Are Watching for From the Fed’s Decision

The Federal Reserve’s decision on Wednesday is one of the last big events in one of the most turbulent years for markets.

(Bloomberg) -- The Federal Reserve’s decision on Wednesday is one of the last big events in one of the most turbulent years for markets.

Strategists are waiting to see if the central bank links the future of asset purchases to measures of employment and inflation, or even takes action to alter the pace or composition of bond buying, for instance by tilting debt purchases to longer maturities to support the economy.

The meeting comes as Covid-19 vaccines are rolled out for the first time, bolstering optimism that the pandemic will ease in coming months. Congressional leaders also appear to be getting closer to agreeing on a fiscal relief package. But if those talks continue to drag on, the pressure on the Fed and Chairman Jerome Powell for economic support may increase.

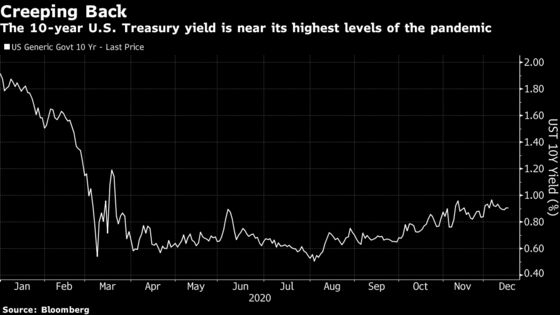

Among the predictions are a flatter yield curve, dollar weakness and a rally in stocks if the Fed delivers a dovish surprise. Looking further out, some strategists still expect the benchmark 10-year Treasury yield to top 1% next year.

Click here for Bloomberg Intelligence’s Fed meeting preview

Here are some views on how markets might react to Fed moves:

Dovish Surprise

There is the possibility that “the Fed manages to surprise dovishly,” said Goldman Sachs Group Inc. strategists led by Kamakshya Trivedi, and that “could unlock a new bout of dollar weakness in fairly short order, and some catch-up in rate-sensitive areas, including tech stocks.”

Bond-Buying Twist

An extension in the bond-buying program, which would be somewhat similar to Operation Twist in September 2011, could “lean toward the lower band of the 2011 move, or about 15 basis points lower in longer-end Treasury yields” given current global central bank accommodation, said Leslie Falconio, senior fixed income strategist at UBS Global Wealth Management. “However, we expect this move to be short-lived, and it does not alter our outlook of a steeper yield curve or higher interest rates (1.25% in the 10-year yield)” in the second half of 2021.

Longer-Term Guidance

“The FOMC could give some longer-term guidance on what would eventually lead to a slowing or ending of asset purchases,” said Steven Englander, global head of G-10 FX research at Standard Chartered Bank. “These steps may be enough to limit the backing up of bond yields on a fiscal deal in Congress and encourage yields lower, faster, absent a deal. Paradoxically, there may be more need for increased asset purchases in the event of a deal, because of the need to demonstrate a soft commitment to capping bond yields.”

Nuanced Needs

“In early 2020, it was obvious when the economy and markets were in distress and required Balance Sheet Galactica,” said Jim Vogel of FHN Financial. “Upcoming needs are likely to be more nuanced, demanding more refined Fed guidance -- which will take time for markets to grasp. Investors have not yet integrated the new inflation policy approach at all.”

Yield Curve

“A WAM extension would bull flatten the curve as the market is only about 25% priced for this dovish outcome. Stopping short of a WAM extension would bear steepen the curve,” said TD Securities strategists including Jim O’Sullivan and Priya Misra, referring to weighted average maturity. In FX, “our base case sees further downside risks for USD, but its downtrend is now increasingly mature. Stretched positioning and valuation considerations may ultimately be a limiting factor on a dovish outcome.”

Dovish Hold

“Our best guess is that the overall tone will be one of hope, but inundated with caution,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. “All said, expect the FOMC to be a dovish hold; with the devil in the details and USD on the back foot.”

©2020 Bloomberg L.P.