Junk Bond Market Signals WeWork to Look Elsewhere for New Cash

WeWork Bonds Drop by Most on Record as Company Delays IPO

(Bloomberg) -- WeWork has an ambition to copy Netflix in one regard: sell junk bonds -- lots of them -- to fund its expansive growth plans.

Netflix Inc., and a small group of other unprofitable companies such as Uber Technologies Inc., have managed to become darlings of the high-yield market even though they’re burning through cash.

But for now, bond investors are signaling to WeWork that coming back to the high-yield credit market would be costly. And that could present a major challenge to the office-sharing company’s expansion hopes now that its initial public offering is on hold until at least October.

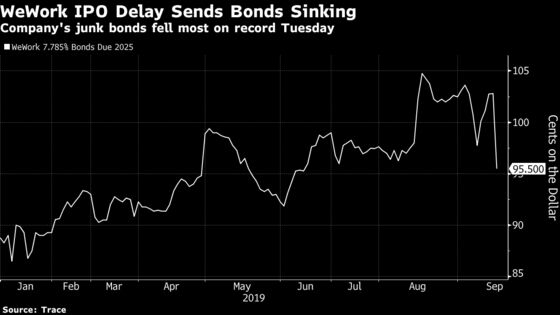

The market’s verdict was delivered Tuesday morning when WeWork’s bonds sunk the most on record. Yields shot up to 8.5%. That’s around a percentage point more than a comparable offering from even lower-rated Tesla Inc.

The IPO delay has left investors guessing where WeWork might turn for much-needed cash, short of another injection from backer Softbank Group Corp. WeWork was seeking to raise more than $3 billion in the IPO, and has another $6 billion in credit financing lined up if the offering was successful.

But in the face of widespread concern over its financial model, the company’s valuation has plummeted, to $15 billion or less. That will make any new debt taken on by WeWork all that more riskier, said Arnold Kakuda, a senior credit analyst at Bloomberg Intelligence.

“If they continue to grow, they’re going to need more and more financing,” Kakuda said. “There’s risk if this market capitalization is so low and yet they have so much debt.”

WeWork’s $669 million of junk-rated bonds due in 2025 dropped as much as 7.3 cents on the dollar to 95.5 cents Tuesday in New York, according to the Trace bond-price reporting system. They’ve since pared back some of those losses to trade around 97 cents on the dollar.

Riskier Credit

At current levels, the market prices WeWork’s debt between the B and CCC ratings tiers. Both Fitch Ratings and S&P Global Ratings give the debt B range grades. Compared to Netflix, which is rated a tier higher, with the third-highest junk grade from ratings companies, it’s a riskier credit.

The potential problem for WeWork is that companies with riskier credit ratings -- or those that trade in line with them -- can have trouble maintaining regular access to the credit markets. In times of turbulence, investors typically cut those companies off first. Less than 10% of new junk bonds this year have been sold by CCC rated companies. (Uber has found success selling bonds that carry a CCC+ grade from S&P.)

Read more from Bloomberg Intelligence: WeWork: Potential Early Redemption For Bonds

Vicki Bryan, chief executive officer of Bond Angle, a high-yield credit research company, said in a report Tuesday that she could still see WeWork issuing more junk bonds, given how hungry investors are for yield in a world with $13.8 trillion of debt with negative interest rates. But she’s skeptical that the debt would be a good buy.

“Just because the company needs fresh cash, pronto, doesn’t mean it’s a good idea for investors to oblige,” Bryan wrote. “Upside potential is limited at best versus downside risk.”

She recommended selling the bonds at their Monday level of about 102.8 cents on the dollar, saying the bonds could plunge 10 to 15 cents if the company falters further.

If the IPO fails, WeWork’s best back-up plan to keep growing might be more cash from Softbank Group, Kakuda said. The Japanese telecom giant made its last investment in WeWork, renamed We Co., at a valuation of $47 billion and the company and its affiliates hold about 29% of WeWork stock.

WeWork has said it could become profitable faster if it slows its expansion plans. But it’s clear the company badly needs cash. S&P Global Ratings has estimated that the company will add 725,000 new desks next year at a cost of about $4.5 billion -- and will likely need to raise cash to fund its 2020 goals.

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Larry Reibstein, Dan Wilchins

©2019 Bloomberg L.P.