Well, That Was Fast. So Are the Bulls Back in Charge, Now?

It’s the correction, corrected.

(Bloomberg) -- It’s the correction, corrected. The unshakable bull. Or the little sell-off that couldn’t.

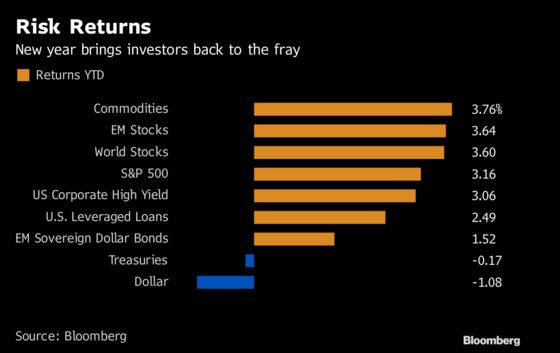

The S&P 500 Index just posted a third consecutive week of gains -- the longest streak since August and the best performance since early 2016. And the resurgent equity gauge isn’t alone: Less than 10 days into the new trading year, a slew of major assets have combined to stage a comeback worthy of a Hollywood blockbuster.

Pick your reason. The U.S.-China trade talks were “serious” and “in-depth.” Jerome Powell checked his stock portfolio. The sun was shining. To a host of investors it probably matters little. The key is that reports of the death of the bull market were, at the very least, premature.

Vaguely upbeat macro news and perceptions of a dovish tilt by the Fed are certainly a large part of this revival. Another has been the dramatic re-pricing of assets during the course of the sell-off, which helped lure investors back to securities that not long ago looked overvalued.

Bank of America Merrill Lynch’s Bull & Bear Indicator fell to an “extreme bear” level on Jan. 3, triggering a buy signal, according to the firm. The gauge has since turned, and strategists led by Michael Hartnett note that the last time it flashed a brief buy signal global equities went on to gain 9 percent in three months. The speed of this reversal is a product of the economic landscape, they reckon.

“Moves are extreme because ‘windows of risk opportunity’ become less in late-cycle,” Hartnett and his team wrote on Thursday.

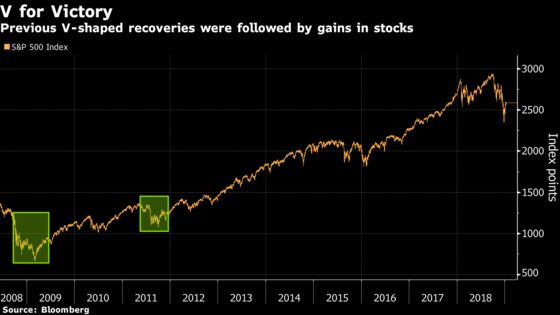

That the velocity of the S&P 500’s reversal is rare can’t be doubted. In the wake of any three-month period in the past decade during which stocks fell 15 percent or more, they only posted a rally of similar magnitude in 10 days or less on three occasions. On two of them, the gauge didn’t revisit its low for at least a year.

That pace raises questions about the sustainability of the move. Jeffrey D. Saut, the chief investment strategist at Raymond James, notes that by one measure the S&P 500 has gone from an extremely oversold condition to an extremely overbought condition in one of the fastest moves on record.

“When this has occurred before there has tended to be a short-term ‘give back,’” Saut wrote in a note on Thursday. “But over the next year returns were substantial.”

U.S. stocks ended Friday little changed, capping a weekly advance of 2.5 percent. The stage looks set for the rally to continue, at least in the near-term. American economic data remains solid, the latest being a not-too-hot, not-too-cold inflation reading on Friday. Downward revisions to forecasts mean companies need to do less to impress during the impending earnings season.

Another factor in the calendar. Investors tend to be cash-rich in January, having reduced risk in their portfolios at the end of the year -- positioning changes that are likely to have been all the more pronounced given the brutal fourth quarter. For all the talk of easing trade fears or a dovish Fed, incremental increases in allocation are one technical reason for the breadth and speed of the rally.

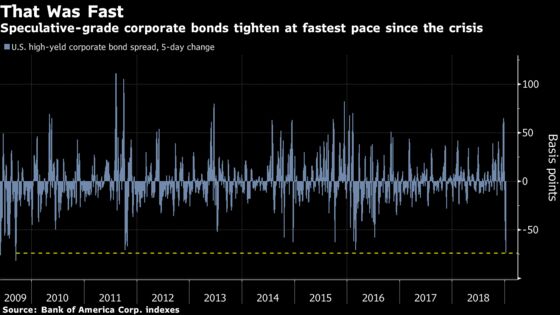

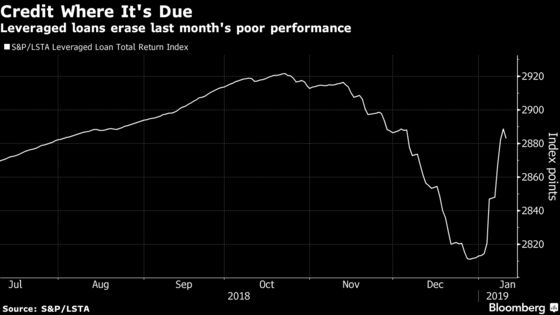

Nowhere has the rebound been more dramatic than the American credit market. At the tail end of 2018, the likes of Leon Black at Apollo Global Management and Scott Minerd at Guggenheim were among big names using words such as “collapse” and “bubble” as they fretted over corporate leverage. As gauges of credit plunged in December, that kind of talk seemed prescient.

Yet the U.S. high-yield spread has tightened at the fastest pace since 2009. Leveraged loans clawed back the losses from all of December in just six sessions.

“There were elements of policy mistake and fears of slowing growth behind recent the moves,” TD Securities strategists including Richard Kelly and Priya Misra wrote this week. “We see no signs that credit availability has tightened sharply in the U.S. In fact, we can see similar episodes through the Eurozone financial crisis of 2010-2012 or the oil shock in 2015-16 when market tightness did not materialize into significant or protracted credit tightness for borrowers.”

This comeback for risk assets, coming so late in this bull market, is the stuff of dreams for many investors. Yet few will easily forget the drama that made it possible. To get up from the canvas you have to first be knocked down, and the final, brutal weeks of 2018 put traders on notice: No one wins forever.

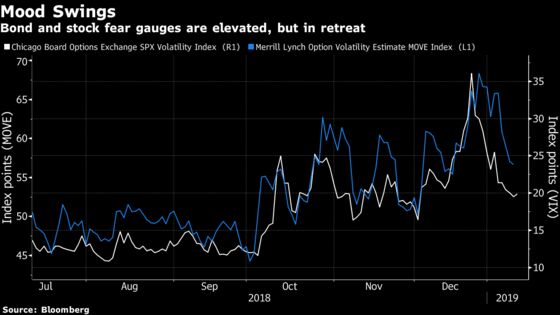

This week the Cboe Volatility Index, a gauge of expected price swings for the S&P 500 known as the VIX, sank back below 20 after peaking above 35 just before Christmas Day. Bank of America Corp.’s MOVE Index, the equivalent gauge for volatility in U.S. Treasuries, is also in retreat as the rush for safer assets ebbs.

But investors are under no illusion that the zen-like calm of 2017 is about to return. The VIX remains at elevated levels, according to Morgan Stanley strategists including Hans Redeker, and is “a warning signal” to investors. Tightening liquidity conditions as well as stubbornly high single-stock volatility are to blame, they wrote in a note.

The latest rout was a vital lesson for a generation on Wall Street that has until now barely known a down year, at least in terms of equities; a dress rehearsal for a volatility regime more in line with historic norms.

“In a post-QE and forward-guidance world and with the Fed funds rate at neutral, we expect levels of volatility to be episodically higher,” wrote Kelly and Misra at TD Securities. “The party’s over, but even factoring in the significant market volatility we saw over the last month, it doesn’t yet point to an immediate collapse in growth.”

--With assistance from Sid Verma, Lisa Lee, Eddie van der Walt and Dani Burger.

To contact the reporter on this story: Samuel Potter in London at spotter33@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Chris Nagi

©2019 Bloomberg L.P.