Weakest Junk Companies Struggle to Sell Debt, Fueling Defaults

Weakest Junk Companies Struggle to Sell Debt, Fueling Defaults

(Bloomberg) -- Junk-rated companies are selling bonds at a feverish pace. But the weakest corporations are notably absent from the party, and their struggles to borrow mean that this year’s wave of bankruptcies may intensify.

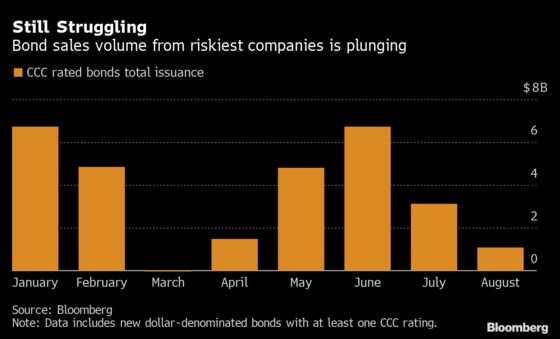

Sales of junk bonds from companies in the CCC tier, typically the lowest credit ratings seen in the high-yield market, amounted to just $1.1 billion this month through Friday, according to data compiled by Bloomberg. That’s less than any month since March, and around 2% of high-yield issuance for August, despite accounting for about 12% of the overall junk bonds outstanding.

Money managers are shying away from many of the bonds because they fear the companies’ revenues are getting clobbered by the pandemic, especially in businesses like cruise lines and oil drillers. Buying some of the riskiest notes at the beginning of a potentially long economic slowdown can amount to courting trouble, said Gary Russell, head of high-yield credit for DWS North America.

“People are a little bit reluctant to go out and take risks in those companies, because we still have some risks on the macro side given what’s going on with Covid-19,” said Russell, whose firm globally oversees $880 billion.

When CCC companies can’t borrow, they often end up filing for bankruptcy as debt comes due. This year has already seen a glut of corporate failures: there were 177 U.S. bankruptcy filings year-to-date by companies with over $50 million in liabilities, according to data compiled by Bloomberg through Aug. 21. That’s the most for any comparable period since 2009, when there were 271 in the full year, the data show. The American Bankruptcy Institute forecasts that bankruptcy filings will reach a record this year.

Economic slowdown can be particularly hard on companies rated CCC. For example, Fitch Ratings cut U.S. Steel Corp.’s senior unsecured debt grade to CCC in May, citing in part its expectation that demand for steel from carmakers would decline. A representative for the company declined to comment.

‘No Choice’

There is still hope for CCC companies. With the Federal Reserve having cut interest rates close to zero, investors are struggling to earn decent returns, and demand for CCC bonds could start to edge higher, said Oleg Melentyev, head of U.S. high-yield strategy at Bank of America Corp.

“Investors have no choice. They’re going to have to go there,” he said.

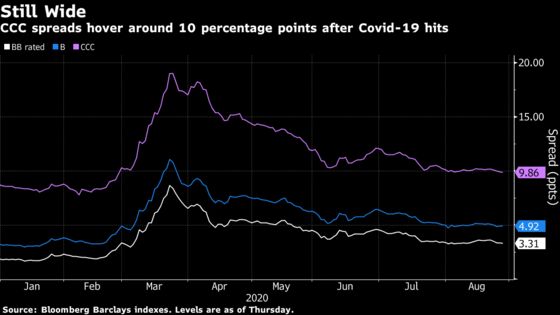

Some already are going there. From June through August, every CCC corporate bond deal that was sold has risen in price, with just one exception, and the average gain is around 5 cents on the dollar, said Melentyev. This month, the lowest-rated junk bonds have been some of the best performers, with CCCs having gained 1.6% through Thursday, single Bs 0.84% and BBs, 0.5%, according to Bloomberg Barclays index data. Average risk premiums on the securities fell below 10 percentage points, a level commonly associated with distress, on Aug. 26.

“The market is saying that it’s time for lending deeper into the credit spectrum,” said John McAuley, head of North American leveraged finance at Citigroup Inc. in an interview. “You will see more CCCs get more access to the market and you will see more stressed credits get access over the coming months.”

Pike Corp., a company that constructs and repairs electric utility lines, sold $500 million of eight-year notes with at least one CCC tier rating earlier this month that yielded just 5.5%. It originally sold at 100 cents on the dollar, and on Friday traded around 100.5 cents.

“That’s a very low yield by historical standards for CCC credit and the deal has traded very well,” said Kevin Bakker, co-head of high yield at Aegon Asset Management. “It’s a signal that for the right company people dont have a problem buying CCCs necessarily.”

Any pickup in issuance of CCC bonds is likely going to be selective, depending on both the borrower and the outlook for its industry amid the pandemic, according to Adi Habbu, senior distressed debt trading desk analyst at Barclays. For one thing, many struggling companies have already borrowed against most of their assets, which may make additional issuances now more difficult, he added.

“Given the current uncertainty, lenders in this space will still focus on whether the particular industry is on a path to recovery and whether there are assets to secure any new debt,” said Habbu.

©2020 Bloomberg L.P.