Wave of Expiring Treasury Options Adds Risk to Jackson Hole

Wave of Expiring Treasury Options Adds Risk to Jackson Hole

(Bloomberg) -- A flood of Treasury options set to expire Friday may dictate the bond market’s reaction to Federal Reserve Chair Jerome Powell’s long-awaited speech on the economic outlook.

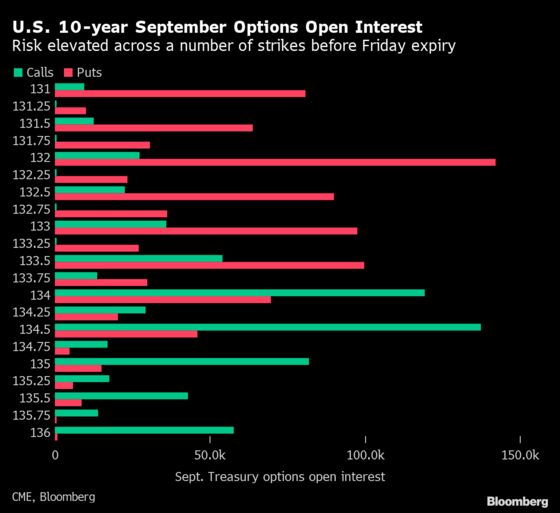

More than 2 million options in the September 10-year contract, which is 63% of total options open interest in Treasuries, expire by the end of trading Friday, raising the prospect for volatility in the wake of Powell’s remarks scheduled to start at 10 a.m. New York time.

For months, Treasury option traders have been amassing hedges against swings in 10-year yields, in part with this week’s Jackson Hole symposium in mind as a potential watershed moment for Fed policy. Yields briefly swung higher Thursday after some of the central bank’s leading hawks urged policy makers to move quickly to slow bond buying. Powell has struck a more patient tone.

As of Wednesday’s close, most risk is concentrated around several options structures that equate to 10-year yields of about 1.5%, 1.34% and 1.21%, compared with the current rate of around 1.34%. Those levels stand out as having potential to sway trading in the aftermath of Powell’s speech, should dealers and option holders trim their vulnerability to market movements leading up to the options expiry and move the price of 10-year futures close to the strike price.

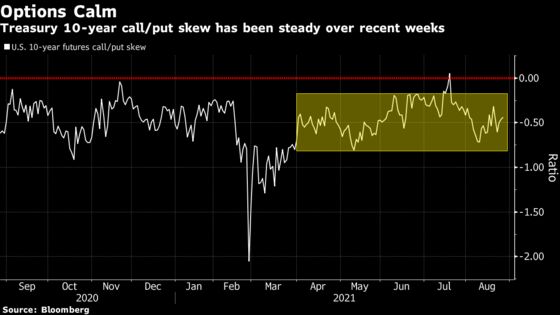

The market’s overall tilt leading into the Jackson Hole gathering appears relatively balanced. JPMorgan Chase & Co. data show that the bank’s clients have pulled back on short bets -- wagers on the reflation bear-steepener trade -- and are close to the most neutral stance in months. Meanwhile, options skew -- representing the relative appetite for put and call options on 10-year notes -- has been mostly calm.

While the market has shifted to a more neutral position, some strategists now see Treasuries as expensive. JPMorgan strategists, for example, in an Aug. 20 report recommended staying positioned for higher 10-year yields contingent on the latest virus wave subsiding without significantly damaging the economy. Those at Citigroup Inc. said a position that reflects a steeper 2- to 10-year curve makes sense, while Barclays Plc strategists pointed toward swaption data which suggest traders remain positioned for a selloff.

Treasury Strategists Weigh Taper Announcement: Research Roundup

One highlight of options activity before the Friday speech has been the first significant long volatility wager in weeks, targeting the U.S. 10-year yield to move beyond either 0.93% or 1.50% by the end of November. Other notable trades have included hedging a swift drop in 10-year yields to 1.15% by Sept. 3. A combined $13 million in premium was paid for these bets.

Traders’ takeaway Friday on the path of the Fed’s asset-purchase tapering also stands to influence bets on when the central bank will lift benchmark rates from near zero. Overnight swaps and eurodollar futures show that the first rate hike is expected around the start of 2023, with the second by June 2023.

In eurodollar options, a stand-out theme over the past week has been a hedge against three-month Libor dropping toward zero -- from around 0.12% now -- via March 2022 contracts. While it’s not an outright bet on rate cuts, it may be an indication of at least one speculator seeing the risk of a more dovish Fed policy than currently priced in.

©2021 Bloomberg L.P.