Wary Global Bond Markets Brace for the Supply Floodgates to Open

The amount of government bonds hitting the private sector is set to swell in 2022, adding pressure on yields to rise further.

(Bloomberg) -- The amount of government bonds hitting the private sector is set to swell in 2022, adding pressure on yields to rise further as investors across most major markets absorb much larger helpings of debt.

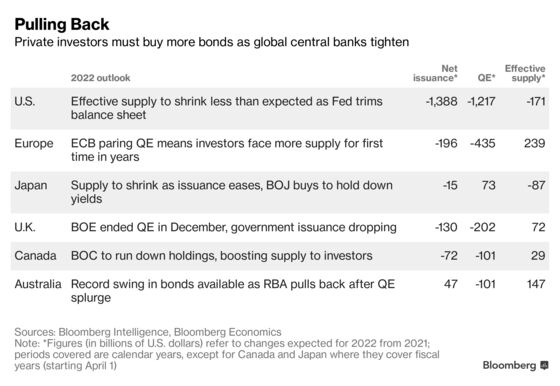

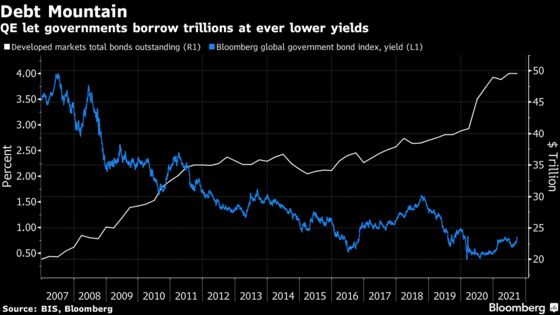

While governments are set to pare borrowings as fiscal outlays ease, the $2 trillion drop in central banks’ net demand will provide a risky real-world test of how much private demand exists. With inflation driving most policy makers to err on the side of tighter settings -- some central banks already plan to start trimming their balance sheets -- investors will need to absorb an increase in effective supply of about $230 billion.

“The inflation genie may well be out of the bottle, and in that case the extra bond supply threatens to become part of a vicious cycle that sends yields grinding higher because price pressures will force central banks to go on trimming QE,” said Stephen Miller, an investment consultant at GSFM, a unit of Canada’s CI Financial Corp.

The U.S. will see the biggest reduction in bonds heading to private hands, but the Federal Reserve’s readiness to hike interest rates and start reducing its debt holdings means the reduction in supply offers cold comfort at best for investors grappling with a host of headwinds for Treasuries.

The effective supply of bonds is on track to rise for the euro zone, the U.K., Australia and Canada, while Japan will see a reduction in bonds available as the central bank there acts to suppress yields. The figures are based on analysis from Bloomberg Intelligence and Bloomberg Economics, cross-referenced with historical issuance and QE figures and central bank guidance on 2022 plans.

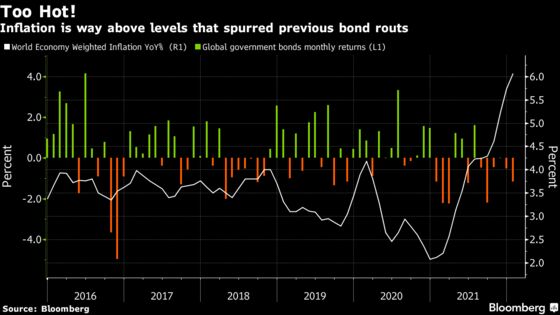

Treasuries have tumbled to their worst start to a year on record, underscoring the dangers as central banks attempt to unwind pandemic-era support.

Quantitative Tightening

The Fed accelerated plans to taper quantitative easing at its December meeting, cutting back bond purchases to $30 billion a month and putting it on pace to end the program early this year.

The central bank also discussed plans to trim its balance sheet aggressively. The Fed’s activity may cause the Treasury to issue just over $250 billion more than if the central bank kept its balance sheet steady -- all of which will need to be absorbed by the private sector in 2022, according to Ira F. Jersey, chief U.S. interest-rates strategist at Bloomberg Intelligence. The analysis cited in this article excludes bills, in order to allow for ready comparison across major developed economies.

“What’s got the markets’ attention is the Fed saying it may offload some of its holdings,” said Prashant Newnaha, an Asia-Pacific rates strategist at TD Securities in Singapore. “You could say the market is probably needing to absorb this supply earlier than they had anticipated.”

| Read more |

|---|

| Fed’s Runoff of Treasuries and MBS Has Several Design Options |

| Euro-Area Bond Supply Could Exceed 1 Trillion Euros |

| Slashed U.K. Borrowing Leaves QE/Net Supply Balanced |

| BoC Rate Hikes, Bond Unwind to Drive Canadian Yields in 2022 |

| Australia Bond Markets Face Supply Shock This Year |

Some investors are wary, with J.P. Morgan Asset Management hunkering down in cash on concern the Fed’s tightening path will kill returns on bonds.

“Without the central-bank purchases and with cash now offering some yield, let’s see how willing investors are to continue to purchase long-duration government debt at significantly negative real yields,” Bob Michele, J.P. Morgan Asset’s fixed-income chief, and colleague Kelsey Berro, wrote in a note. There’s a potential for U.S. 10-year yields to rise as high as 3% this year, they said.

The likely increase in effective global supply will offer a keen test for the savings glut that helped bring yields down at least twice last year. Fed Chairman Jerome Powell highlighted the role of deep-pocketed foreign investors in repressing longer-dated yields just after December’s policy meeting.

Of course, central bankers’ plans are written in pencil, not ink. A disorderly move higher in rates, and the subsequent tightening of financial conditions that would ensue, or another severe flareup of the Covid-19 pandemic could cause policy makers to change course.

The willingness of the European Central Bank and the Bank of Japan to continue holding down yields will be a pivotal factor, as traders are betting that all the other major markets will see central banks raise benchmark interest rates at least 75 basis points this year. The BOJ is likely to boost bond purchases around the same time the Fed starts to raise the policy rate, according to Bloomberg Economics’ Yuki Masujima, who therefore projects a decrease in net supply for Japan this year.

GSFM’s Miller said it’s possible the extra bonds heading to private hands won’t have a major impact, but that would only be the case if the inflation environment ends up being a benign one, something he rates as a one in four chance.

“The rosier scenario for bonds would be if central banks can convince investors that they have inflation under control,” he said. “In that instance, the boost in bonds available will not have much impact as markets believe that a lack of price pressures opens the door to a re-engagement with QE in the event of an emergency.”

The Breakdown

Here’s how the supply dynamic shakes out in the world’s major economies, ordered by market size:

- The U.S. will see the biggest drop in net government issuance as the $22 trillion market’s expansion peaks, but it will also see the largest reduction in central bank easing. The Fed will shift from 2021’s $960 billion of Treasuries purchases to about $60 billion of buying and then run down its balance sheet by about $300 billion or more, starting in July, Jersey estimates

- The euro zone is likely to see effective supply rise 100 billion euros ($114 billion), partly as the ECB gradually trims bond buying, according to Bloomberg Intelligence’s Huw Worthington. France, Italy and Spain will all need to rely on sizable purchases by investors. That could place extra stresses on those markets relative to Germany, where net supply is expected to shrink

- Japan’s available bonds will ease down as a slight uptick in redemptions brings down net government issuance and the BOJ defends its target for 10-year yields

- U.K. issuance will drop, but investors will face an increased burden after Bank of England ended its QE program in December

- Canada will see a surge in net supply as the Bank of Canada moves to reduce its balance sheet fairly rapidly following the decision in October to end asset purchases, according to Angelo Manolatos, a senior associate analyst for BI

- Australia will see a surge in supply to private investors as the central bank plans to gradually end purchases after snapping up about three bonds for every one the government added to the market in 2021. That means about A$76 billion ($55 billion) more debt will be available to investors this year, according to Bloomberg Economics’ James McIntyre, the most for any year outside 2020’s pandemic-induced surge. Effective supply shrank A$128 billion last year

©2022 Bloomberg L.P.