Warning to Bond Traders: Consensus Trades Usually End Badly

Warning to Bond Traders: Consensus Trades Usually End Badly

(Bloomberg) -- Bond strategists are almost unanimous about the outlook for global yield curves: The risk is a one-sided trade.

The most influential names on Wall Street are almost as one in predicting the U.S. curve will steepen as the Federal Reserve cuts interest rates, while those in other developed markets will flatten as global growth slows. Speculation about a possible return to quantitative easing in Europe last week gave a big boost to the outlook for flatter curves there.

So far the trades recommended by strategists have been on the money, and this has led to the positions growing crowded. Given the one-sided tilt, there’s a risk that any upturn in global sentiment may set off a squeeze as traders attempt to cash out at the same time. Such things have happened before: recall the spike in the Cboe Volatility Index last year.

That said, here is what strategists are recommending for major markets:

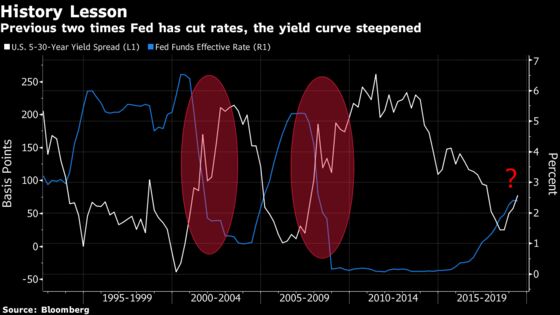

U.S. Treasuries: Trading the Fed

Bank of America, Barclays Plc, Goldman Sachs Group Inc., JPMorgan Chase & Co., Morgan Stanley, NatWest Markets Plc and TD Securities Inc. are all recommending some form of trade that will benefit from a steeper U.S. yield curve.

The Fed at its June 18-19 meeting dropped its reference to staying “patient” on rates due to uncertainties about growth and signaled it was ready to cut borrowing costs. Following the decision, strategists who were already advocating bets on a steeper curve reaffirmed their view, while JPMorgan shifted to join them.

One of the most popular parts of the yield curve to place steepener bets on is between five- and 30-year Treasuries. The spread between the two expanded to 80 basis points on Monday, the widest since November 2017, from as little as 33 basis points in December. A yield curve steepens when the spread between shorter-maturity yields and longer-dated ones increases, while a flattening is the reverse.

European Bonds: QE Revival

European exporters are being pummeled by slowing global growth and escalating trade tensions -- and this is putting policy easing back on the agenda. Given the European Central Bank’s deposit rate is already minus 0.4%, there’s little room to push it any lower. One alternative being discussed is a revival of QE. Strategists are now touting their favorite crisis trades: Bet longer-maturity bonds will outperform shorter-dated ones, and buy the debt of non-core nations such as France, Spain and Italy.

If the ECB increases purchase limits for each issuer, flattening trades are likely to become “turbo-charged,” Citigroup Strategist Jamie Searle in London wrote last week in a client note. The spread between 10- and 30-year Spanish bonds is the best approach, and may shrink another 20 basis points, he said.

Japanese Bonds: Staying Home

Japanese investors are known for their deep pockets and search for higher yields. Unfortunately for them, yields on many of their favorite foreign bonds have tumbled in recent months, meaning they are increasingly likely to stay at home and choose longer-maturity JGBs instead.

“Super-long JGB and JPY swap curves have the potential to flatten further,” HSBC’s Asia Pacific Rates Strategist Dayeon Hong wrote in a research note. Demand for the longest maturities will also be supported by the prospect of further Bank of Japan stimulus, and that fact that all local debt up to 10 years has negative yields, she said.

Goldman Sachs is also recommending 10-to-30-year JGB flatteners in a note published Sunday, while Morgan Stanley strategists have been recommending 20-40-year ones. JPMorgan said it took profit on a 20-30-year version of that trade last week, but retains a medium-term flattening bias.

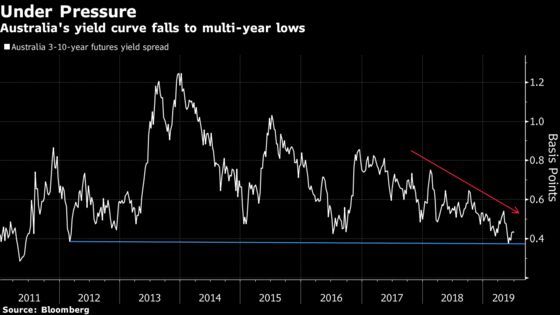

Aussie Bonds: Further Easing

The Reserve Bank of Australia has cut rates once and the market is pricing in a more than 80% chance of a second one for July. With further easing already factored into shorter maturities, the scope for further declines in the front-end is limited, whereas falling yields overseas are expected to compress the longer end of the curve.

Read more: bet Australia’s bond yield curve will flatten

Strategists are united in recommending flattening trades in Australia. JPMorgan and Australia & New Zealand Banking Group Ltd. prefer targeting the three-to-10-year spread, while HSBC is looking out further along the curve. Citigroup and BofAML express the view with offsetting bets on steepening on the U.S. curve.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Nicholas Reynolds, Joanna Ossinger

©2019 Bloomberg L.P.