Warning Bells Sound for Europe’s Big Exporter

Warning Bells Sound for Europe’s Big Exporter

(Bloomberg) -- Europe’s largest economy is attracting bad news as companies are entering the earnings season. While Germany’s DAX Index has managed to shrug off bad economic indicators and trade worries that had hit shares in May, yesterday’s profit warning from BASF was harder to ignore. And dividend futures indicate traders are pricing in payout cuts at companies such as BASF, Bayer and Lufthansa.

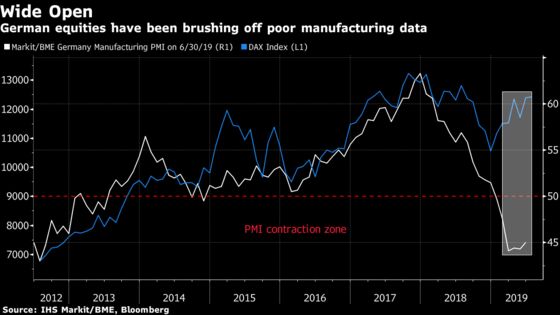

The DAX’s performance has broken away from macro fundamentals this year. Within the main European economies, Germany is the bottom country when it comes to manufacturing PMI, with data indicating a contraction since January. Yet, the equity benchmark has climbed near a one-year high and has entered a bull market again.

Although trade tensions have faded for now amid bets of looser monetary policy, no resolution has been reached between the U.S. and China. Given the German gauge is a manufacturing-heavy index, and suffered more than peers as tariff worries grew last year, any new developments will be keenly watched.

While the DAX is a total return index, looking at its performance minus the dividend effect shows it’s actually underperforming most of the main European indexes this year, with the exception of U.K. and Spanish benchmarks.

Carmakers BMW and Daimler have already warned about their outlook earlier this year and underwhelming results from Geely yesterday did not bode well for the auto sector. BASF’s profit warning surprised analysts with its magnitude and rippled through the sector. Unfortunately for the DAX, autos and chemicals account for more than a quarter of the index.

Since dividend levels are very relevant to the benchmark, they should be closely monitored as warnings accumulate for high dividend yield shares. Deutsche Bank already said it will omit a payout next year after restructuring, while swaps show Lufthansa’s dividend could be at risk as its outlook is darkening. More bad news could end up weighing on the DAX’s performance. The dividend swap market has started to price a potential cut for BASF, while Covestro could also be impacted. The table below shows the difference between dividend swaps and estimated dividends.

| DAX Members Among Highest Dividend Yield Payers | ||||

| Name | Indicated Dividend Yield | Est. Dividend (euro) | 2020 Dividend Future (euro) | Spread |

| Daimler | 6.5% | 2.7 | 2.62 | -1.1% |

| BASF | 5.4% | 3.3 | 3.03 | -8.2% |

| Lufthansa | 5.0% | 0.8 | 0.75 | -6.3% |

| BMW | 4.9% | 2.8 | 2.71 | -1.5% |

| Bayer | 4.9% | 2.7 | 2.44 | -9.6% |

| Source: Bloomberg | ||||

Another potential warning to watch is the Rhine level. Last week, Germany’s Transport Minister Andreas Scheuer said lower water levels may again become a problem for the German industry, while ThyssenKrupp says Rhine levels are a matter of survival for the company. Last year’s drop to a historically low level had dented German growth, and an earlier-than-usual dry spell in June this year could prove a challenge.

In the meantime, Euro Stoxx 50 futures are trading little changed ahead of the open.

- Watch Mexico-exposed stocks after the country’s finance minister resigned on Tuesday, casting doubt on the government’s ability to stave off economic and financial challenges it faces and caused the Mexican peso to drop. Watch BBVA, Santander, Telefonica, Iberdrola among others.

- Watch U.K. stockssensitive to Brexit newsflow after U.K. lawmakers passed a measure aimed at stopping the next prime minister from forcing the country out of the European Union without a deal. Watch housebuilders, commercial-property names, domestic lenders, retailers and government contractors.

COMMENT:

- “Q2 earnings are unlikely to impress, and despite lowered expectations, stocks may not all be immune to disappointment,” Barclays strategists write in note. “We advise caution on cyclicals, and more particularly on the Growth/Quality names priced for perfection. The central banks’ put provides a backstop to equity valuations, but we believe that further material market upside is contingent on EPS momentum turning positive, which looks hypothetical for now.”

COMPANY NEWS AND M&A:

- GAM Holding Sees First Half Net Loss as Asset Shrinkage Bites

- Airbus to Check for Cracks on Emirates, Qantas A380 Wings (1)

- Glaxo Builds Up AI Team With Another Hire From Biotech Hotbed

- U.K. Utilities: Labour Pledge Derails Electricity North West GBP2b Sale: FT

- Danske Bank Wedged in a Tight Spot to Find Ways to Boost Returns

- Bankers’ Union in Denmark Sees Limited Danske Cuts: Borsen

- Baloise Sees ’Exceptionally Strong’ Results for 1H

- Tryg Second Quarter Pretax Profit 3.1% Below Estimates

- Orange Belgium CEO Sees Profitability on Telco Offers: L’Echo

- Acacia Mining Says It’s Worth Far More Than Barrick Offered (1)

NOTES FROM THE SELL SIDE:

- Outotec is upgraded to buy from underperform at Jefferies after news of plans to combine with Metso Minerals, as deal means its shares expose the investor to both self-help potential, merger synergies and Metso Minerals. Broker’s analysis implies 40% upside in Outotec shares vs 15% in Metso.

- Ashtead is cut to equal-weight (overweight) after a strong share price run, while price target is raised to 2,525p from 2,415p implying 10% upside vs a 19% average across broker’s overweight business services stocks, Morgan Stanley says.

TECHNICAL OUTLOOK for Stoxx 600 index:

- Resistance at 397.9 (May 2018 high); 403.7 (2018 high)

- Support at 385.7 (76.4% Fibo); 381 (50-DMA)

- RSI: 57.5

TECHNICAL OUTLOOK for Euro Stoxx 50 index:

- Resistance at 3,519 (76.4% Fibo); 3,596 (May 2018 high)

- Support at 3,412 (50-DMA); 3,404 (61.8% Fibo);

- RSI: 62.7

MAIN RESEARCH AND RATING CHANGES:

UPGRADES:

- Komplett Bank upgraded to buy at ABG; PT 11 Kroner

- MMK Group GDRs upgraded to overweight at JPMorgan; PT $11.50

- Outotec upgraded to buy at Jefferies

DOWNGRADES:

- Ashtead downgraded to equal-weight at Morgan Stanley

- Chemring Group downgraded to hold at Berenberg

- Covestro downgraded to reduce at AlphaValue

- Deutz downgraded to hold at Berenberg

- NLMK Group GDRs downgraded to neutral at JPMorgan; PT $28

- Pandora cut to sell at SEB Equities; Price Target 235 Kroner

- XXL cut to hold at Kepler Cheuvreux; Price Target 30 Kroner

INITIATIONS:

- Ferrovial rated new overweight at Barclays; PT 27 Euros

- Kering rated new sell at China Renaissance; PT 480 Euros

- LVMH rated new hold at China Renaissance; PT 390 Euros

- Luceco rated new add at Peel Hunt

- M&C Saatchi rated new hold at Peel Hunt

- Playtech rated new overweight at JPMorgan; PT 6.03 Pounds

- Watches of Switzerland Group rated new buy at Goldman

- Watches of Switzerland Group rated new overweight at Barclays

MARKETS:

- MSCI Asia Pacific down 0.3%, Nikkei 225 down 0.1%

- S&P 500 up 0.1%, Dow down 0.1%, Nasdaq up 0.5%

- Euro up 0.02% at $1.121

- Dollar Index up 0.02% at 97.51

- Yen down 0.02% at 108.87

- Brent up 1% at $64.8/bbl, WTI up 1.4% to $58.6/bbl

- LME 3m Copper up 0.6% at $5856.5/MT

- Gold spot down 0.3% at $1393.5/oz

- US 10Yr yield up 1bps at 2.08%

ECONOMIC DATA (All times CET):

- 8:45am: (FR) May Manufacturing Production MoM, est. 0.3%, prior 0.0%

- 8:45am: (FR) May Manufacturing Production YoY, prior 0.5%

- 8:45am: (FR) May Industrial Production YoY, est. 1.6%, prior 1.1%

- 8:45am: (FR) May Industrial Production MoM, est. 0.3%, prior 0.4%

- 10am: (IT) May Industrial Production MoM, est. 0.2%, prior -0.7%

- 10am: (IT) May Industrial Production WDA YoY, est. -1.5%, prior -1.5%

- 10am: (IT) May Industrial Production NSA YoY, prior 0.1%

- 10:30am: (UK) May Monthly GDP (MoM), est. 0.3%, prior -0.4%

- 10:30am: (UK) May Monthly GDP (3M/3M), est. 0.1%, prior 0.3%

- 10:30am: (UK) May Industrial Production MoM, est. 1.5%, prior -2.7%

- 10:30am: (UK) May Industrial Production YoY, est. 1.2%, prior -1.0%

- 10:30am: (UK) May Manufacturing Production MoM, est. 2.2%, prior -3.9%

- 10:30am: (UK) May Manufacturing Production YoY, est. 1.1%, prior -0.8%

- 10:30am: (UK) May Construction Output MoM, est. 0.1%, prior -0.4%

- 10:30am: (UK) May Construction Output YoY, est. 0.9%, prior 2.4%

- 10:30am: (UK) May Index of Services MoM, est. 0.1%, prior 0.0%

- 10:30am: (UK) May Index of Services 3M/3M, est. 0.1%, prior 0.2%

- 10:30am: (UK) May Visible Trade Balance GBP/Mn, est. £12.55b deficit, prior £12.11b deficit

- 10:30am: (UK) May Trade Balance Non EU GBP/Mn, est. £4.8b deficit, prior £4.6b deficit

- 10:30am: (UK) May Trade Balance GBP/Mn, est. £3.2b deficit, prior £2.74b deficit

* For a daily wrap on developments in European equity capital markets, click here

To contact the reporter on this story: Michael Msika in London at mmsika4@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Namitha Jagadeesh

©2019 Bloomberg L.P.