Wall Street's Top Equity Bull Warns Over Quant-Driven Selling

Wall Street's Top Equity Bull Warns Over Quant-Driven Selling

(Bloomberg) -- The spike in market volatility risks turning one of this year’s biggest stock buyers into a seller, according to Wall Street’s top equity bull.

Computer-driven traders, who make bets based on momentum and volatility signals, may dump more than $70 billion of shares in coming weeks should the market turbulence persist, estimates Binky Chadha, chief global strategist at Deutsche Bank, whose year-end target for the S&P 500 is the highest among those tracked by Bloomberg.

Chadha offered his warning ahead of Monday’s sell-off in U.S. stocks -- and just after their worst week in 2019 and the VIX spiked the most since early 2018. The sudden rupture of volatility may trigger selling from quant-driven funds that have been partly lulled into buying amid steady equity gains since the fourth-quarter sell-off. At the end of July, the group’s equity exposure tracked by Deutsche Bank stood at one of the highest levels in the past decade.

Their exposure “is already at the top of its historical range and the risk, therefore, asymmetric,” Chadha wrote in a note to clients before today’s U.S. trading. “Extremely wide intra-day ranges in the S&P 500 like the ones experienced over the last three days have historically been followed by sustained increases in vol, which in turn would lead to systematic funds reducing equity exposures.”

That’s not good news for a market where everyone else from individual investors to long-short hedge funds has been reluctant to embrace the equity rally. Positioning between quants and discretionary investors has been at odds that Deutsche Bank says one has to go back to the Chinese devaluation of its currency in 2015 to see a similar divergence.

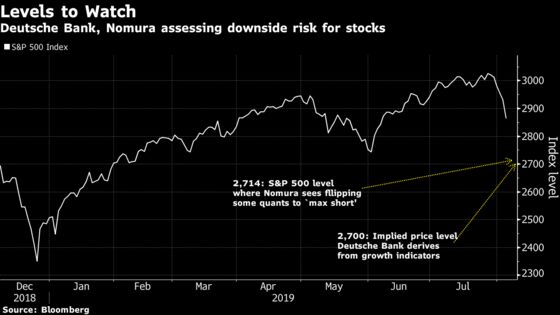

Deutsche Bank isn’t the only one that focuses on quant funds to gauge the market’s potential downside. At Nomura, Charlie McElligott, a cross-asset strategist, estimates that a decline in the S&P 500 to 2,830 would flip some funds to bet against stocks. A “maximum short” position would be triggered when the index falls below 2,714, he says.

The benchmark index dropped 3.3% to 2,835 as of 3:18 p.m. in New York.

Stocks sold off last week after Federal Reserve Chairman Jerome Powell played down his easing cycle and President Donald Trump slapped new tariffs on China. The double blows are forcing investors to reassess a rally that has lifted the S&P 500 up 13% this year even as corporate profits stagnate. A Deutsche Bank model suggested current economic growth indicators point to a price level of 2,700 for the S&P 500.

“Volatility across asset classes had been running much lower than implied by the slowdown in growth and has plenty of room to rise further,” Chadha said. “A resolution of the trade war, and not Fed easing, is key for a turn up in growth.”

Below is what Deutsche Bank says how various quant funds may react in response to continued elevation in volatility.

- Volatility control funds already started trimming equity allocations from maximum levels and their selling could reach $5 billion to $6 billion in the next couple of days. A reduction in equity exposure from 70% to 50% implies additional selling of about $50 billion in “a relatively short period of time.”

- Commodity trend advisors, or CTAs, could unload about $20 billion of shares in two to three weeks should a break in the uptrend signals force them to cut exposure to levels seen in mid July

- Risk parity funds are slow-moving and would require a more sustained increase in realized vol for a reduction in equity exposures

To contact the reporter on this story: Lu Wang in New York at lwang8@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Jeremy Herron, Dave Liedtka

©2019 Bloomberg L.P.