Watchdogs Can’t Handle Wall Street’s Riskiest Loans

Wall Street's Riskiest Loans Flash Dangers as Watchdogs Muzzled

(Bloomberg) -- Washington rewrote the rulebook for Wall Street after the 2008 financial crisis, but dangerous lending is still eluding regulators.

Take Bomgar Corp., which just lined up $439 million in loans. The deal marked the software company’s third trip to the debt markets this year. By one estimate, Bomgar’s leverage could soon spike to 15 times its earnings, raising questions about whether the firm could ever pay it off.

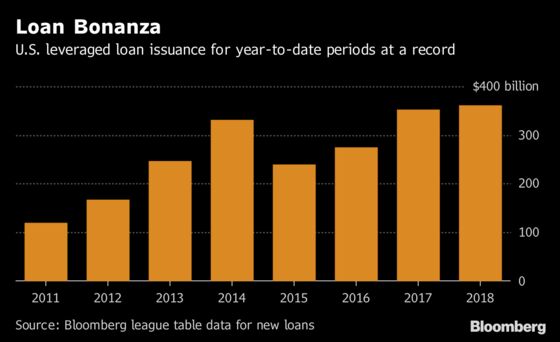

These kinds of transactions are increasingly common in the U.S.’s more than $2 trillion market for leveraged loans and junk bonds, and agencies including the Federal Reserve can’t do much about it. That’s because some of the most aggressive financing is being done outside the traditional banking sector.

“Regulators should sound the alarm,” former Fed Chair Janet Yellen said in an interview. “They should make it clear to the public and the Congress there are things they are concerned about and they don’t have the tools to fix it.’’

If regulators can’t maintain safe standards, it’s not just Wall Street’s over-levered corporate clients that might be at risk. Thousands of jobs could be at stake should companies start defaulting on their loans.

Right now, watchdogs don’t see any perils from leveraged loans that could threaten the financial system the way the collapse of the housing market did a decade ago. The market is much smaller and any excessive borrowing is concentrated among companies, not millions of U.S. households. Banks also are much better capitalized then they were before the crisis.

Fed Chairman Jerome Powell said Wednesday that the “overall vulnerabilities” are “moderate.” Speaking at a press conference, he also noted that the banks directly overseen by the Fed “take much less risk than they used to” in leveraged lending.

But in addition to heavily-regulated banks, Bomgar’s lenders include Jefferies Financial Group Inc. and Golub Capital BDC Inc. -- firms outside the Fed’s reach. While Moody’s Investors Service has predicted an outsized debt load, Bomgar said its leverage will be manageable at about seven times earnings. But even that level exceeds what regulators have typically considered prudent.

If Bomgar does run into trouble, Jefferies and Golub may not take a hit. That’s because leveraged loans are usually either bought by mutual funds and other fund managers or packaged into securities that are sold to investors.

Bomgar, Jefferies and Golub didn’t respond to requests for comment.

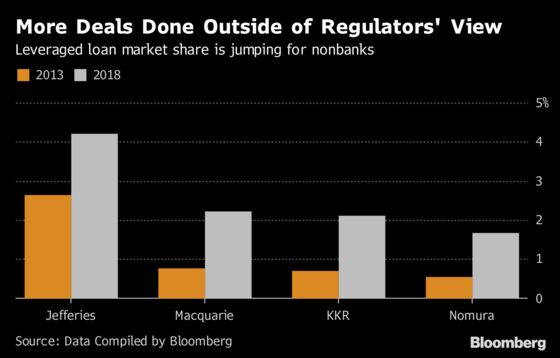

An effort by federal agencies to strengthen loan standards triggered some of the market’s shift from banks to less-regulated lenders, including Jefferies, KKR & Co. and Nomura Holdings Inc.

Back in 2013, the Fed, Office of the Comptroller of the Currency and Federal Deposit Insurance Corp. issued guidance that schooled banks on what was acceptable leverage, restricting firms such as JPMorgan Chase & Co. and Bank of America Corp. from participating in the riskiest deals. When Powell was a Fed governor in 2015, he said the guidelines would prevent “a return to pre-crisis conditions.”

Amid strong opposition from Wall Street lobbyists, Republican lawmakers and Trump administration officials, the guidance suffered a fatal blow last year when the Government Accountability Office declared it an overreach by regulators. That left Powell and other industry watchdogs in a bind. They said they still believed in their tough standards, but wouldn’t use them to punish banks.

With the hammer gone, banks have more leeway to compete with their less-regulated cousins. Already, Goldman Sachs Group Inc. and Credit Suisse Group AG are among firms that have arranged financing that previously might have run afoul of the Fed and other agencies.

Investors including mutual funds, insurance companies, hedge funds and banks have snapped up leveraged loans in recent years because the debt produces much better returns than safer assets such Treasuries.

But despite a slide in loan quality, yields aren’t rising much -- meaning investors may not be getting fully compensated for the risk they’re taking on. That echoes what happened with subprime-mortgage securities 10 years ago, when holdings labeled low risk triggered billions of dollars of losses.

“Money is chasing looser and looser projects, and from one day to the next the spring uncoils,” said Torsten Slok, chief international economist at Deutsche Bank AG in New York. “What exactly do you do when you see tight credit spreads, low quality and significant issuance -- how do you slow that down gradually?”

So far, regulators appointed by President Donald Trump don’t seem focused on slowing things down.

Joseph Otting, the former banker who leads the Office of the Comptroller of the Currency, said in a February speech that “institutions should have the right to do the leveraged lending they want as long as they have the capital and personnel to manage that.” Early last year, the OCC downgraded leveraged lending in its twice-yearly risk report from a “key risk” to something meriting “continued monitoring.”

“There isn’t anything going on in the market right now that would cause us to increase our supervision of that because we are always looking at that type of portfolio,” Richard Taft, the OCC’s deputy comptroller for credit risk, said in an interview this month.

Taft added that the agency has seen improved risk-management by lenders. But he granted that OCC supervisors have no say over the financing offered by nonbanks, which have engaged in transactions that the regulator wouldn’t “normally consider to be within safe and sound practices.”

If there’s a part of the government that could take away the punch bowl, it might be the Financial Stability Oversight Council, which was set up through the 2010 Dodd-Frank Act to monitor threats that could lead to another crash.

The group of financial regulators -- including the heads of the Fed, OCC, FDIC and Securities and Exchange Commission -- didn’t broadcast any warnings about leveraged lending in its most recent annual report. In fact, the document said the number of leveraged loans trading at distressed levels had been falling.

The International Monetary Fund has a different view. Its analysis from April found a lot of market excesses and declining protections for investors, noting that a “share rise in defaults following a tightening of financial conditions, or a shutdown of the market at the extreme, could have large negative implications for the real economy.”

Tobias Adrian, a former senior vice president at the New York Fed who’s now the IMF’s financial markets chief, said in an interview that “supporting growth is important, but future downside risks also need to be considered.” He said regulators have “limited tools to rein in nonbank credit,” so the Fed may need to use monetary policy to cool down lending.

Yellen agrees that the government’s hands are tied.

“Dodd-Frank didn’t go far enough to give regulators power to deal with this,” she said.

--With assistance from Lisa Lee and Ben Bain.

To contact the reporters on this story: Jesse Hamilton in Washington at jhamilton33@bloomberg.net;Craig Torres in Washington at ctorres3@bloomberg.net;Sally Bakewell in New York at sbakewell1@bloomberg.net

To contact the editors responsible for this story: Jesse Westbrook at jwestbrook1@bloomberg.net, ;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Gregory Mott

©2018 Bloomberg L.P.