Wall Street’s Painful Lessons From a Year of Epic Debt Fights

Wall Street’s Painful Lessons From a Year of Epic Debt Fights

(Bloomberg) -- From the collapse of storied retailers to the fall of a prominent hedge fund manager, 2020 offered a harsh reminder of what happens when the economy goes south.

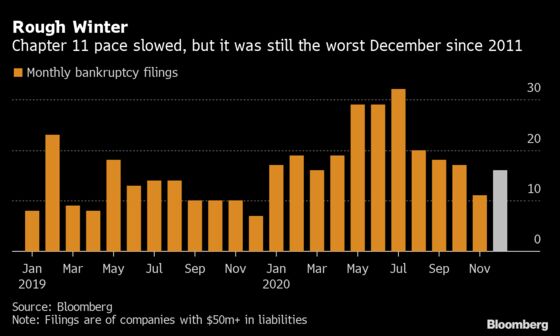

Bankruptcies reached levels not seen in a decade, distressed debt soared to almost $1 trillion and it may take years to repair the damage to airlines, restaurants and hotels. While 2020 may be over, the drama probably isn’t.

“If you don’t deeply cut debt and provide new cash to some of these companies, even restructuring won’t save them,” said Saul Burian, a senior member in Houlihan Lokey Inc.’s U.S. restructuring group. “All you’re really doing is changing ownership, and taking back a hobbled donkey does not make it a race horse.”

Here are some of the lessons learned in 2020.

1. It gets ugly fast

Litigation erupted in cases where select lenders moved up the repayment pecking order at the expense of others, a practice known as “priming.” Apollo Global Management and other lenders tried to block such a maneuver at Serta Simmons Bedding LLC, while Oaktree Capital drove a similar deal for restaurant supplier TriMark USA LLC.

“I never thought I’d hear myself say it but it has gotten quite extreme out there,” Apollo co-President Scott Kleinman said during a virtual panel at the Milken Institute Global Conference in October on this year’s “lender-on-lender violence.”

For some, the behavior went too far. Dan Kamensky, the founder and manager of Marble Ridge Capital, had a reputation for the kind of aggressive dealing that makes careers in distressed investing. But when he ordered Jefferies Financial Group Inc. to “stand DOWN” from its plan to bid against Marble Ridge for shares of a Neiman Marcus Group Inc. unit in the retailer’s bankruptcy, Kamensky was accused of securities fraud and extortion, and Marble Ridge ended up shutting down.

The irony was that Kamensky had long waged a campaign against the transfer of that unit out of creditors’ reach by Neiman’s owners, Ares Management Corp. and Canada Pension Plan Investment Board. The private equity sponsors ultimately had to give a chunk of it back to creditors for them to approve its bankruptcy plan.

2. Check the fine print

When the virus first spread across the U.S., a robust pipeline of mergers, acquisitions and financing agreements froze as panicked would-be buyers sought an escape hatch. Mergers and acquisitions worldwide fell by nearly a third by April versus the same period a year ago.

Among the contested deals were SoftBank Group Corp.’s $3 billion purchase of WeWork Cos. stock and Sycamore Partners’s $1.1 billion bid for a controlling stake in L Brands Inc., owner of the Victoria’s Secret lingerie chain. Courts flooded with lawsuits over canceled transactions. Bankrupt companies weren’t immune: a judge in March nullified a court order allowing EP Energy Corp. to slash billions of dollars in debt from its balance sheet through a reorganization plan.

Corporate lawyers now are checking contracts twice -- and thrice -- for the fine print on “material adverse change,” or MAC clauses, which allow for legal deal exits under certain scenarios.

3. Don’t try to call the bottom

The initial boom in defaults and discounted debt didn’t last long. Intervention by the Federal Reserve, which pumped cash into the market, forestalled much of the fallout. Markets took the cue and offered credit far and wide, lifting the fortunes of shaky companies. By September, new corporate bond issuance set a record.

Even Carnival Corp. and its competitors in the cruise industry, with significant exposure to the pandemic downside, were able to raise billions of dollars after the pandemic hit. For investors who sought to profit from huge sell-offs, there was barely time to open their spreadsheets before the party was over.

Howard Marks, the co-founder of Oaktree, was uncannily prescient. He warned that it was “irrational” to try to time the downturn perfectly, but essentially managed to do it himself, saying in April that it was time to play offense.

4. The stock market isn’t a video game

Shares of bankrupt companies, which are typically wiped out during the court process, got red hot with individual investors -- who flocked to sites like Robinhood to day trade during the pandemic. The trading experience offered by the online brokerage and others like it in the smart phone era drew criticism for the “gamification” of investing.

The stock of Hertz Global Holdings Inc., for example, more than doubled even as it began the Chapter 11 proceeding that would likely render the investment worthless.

Hertz went so far as to try selling new shares during its bankruptcy as a way to raise the cash it needed to fund the process. That was enough for regulators to step in, and Hertz scrapped the plan.

5. The retail apocalypse is now

Roughly three dozen retail chains entered bankruptcy in the U.S. this year, according to data compiled by Bloomberg. Some like Pier 1 Imports Inc. and the owner of New York & Co. clothing never made it out.

Going out of business sales, typically a bright spot for revenue that helps companies keep operating and fund creditor recoveries, were far from a sure thing amid pandemic lockdowns, sending some chains into liquidation.

The “retail apocalypse” caught up to mall owners. None of the real estate investment trusts that operate shopping outlets had filed for bankruptcy since General Growth Partners in 2009.

This year two collapsed simultaneously -- Pennsylvania Real Estate Investment Trust and CBL & Associates Properties Inc. -- together accounting for about 87 million square feet of real estate across the U.S.

Three separate times, healthier landlords, Simon Property Group Inc. and Brookfield Property Partners LP, opted to buy their tenants in partnership deals for Forever 21 Inc., J.C. Penney Co. and Brooks Brothers Group Inc.

It’s a doubling down on retail, but also a bid to preserve the rental income of large tenants. Skeptics abound, but Simon has said that its first such experiment, the purchase of Aeropostale, was a financial success.

6. Mistakes are costly

Revlon Inc. sidestepped bankruptcy after completing debt deals, but the process proved costly for loan administrative agent Citigroup Inc. In one of the more memorable mistakes on Wall Street, the bank in August sent $900 million of its own money to Revlon lenders. It recouped around $400 million and sued 10 asset managers to get the rest back, arguing they knew the payment was in error.

A vice president at HPS Investment Partners said of receiving the payment: “As Steve Miller said, take the money and run.”

©2020 Bloomberg L.P.