Growth Stocks Haven't Been This Expensive Since the Dot-Com Peak

For students of market history, the third month of the 21st century is infamous.

(Bloomberg) -- For students of market history, the third month of the 21st century is infamous.

March 2000 was when the Nasdaq Composite Index marked a peak in the dot-com bubble. By the end of the year, it fell by more than 50 percent, with more losses to follow.

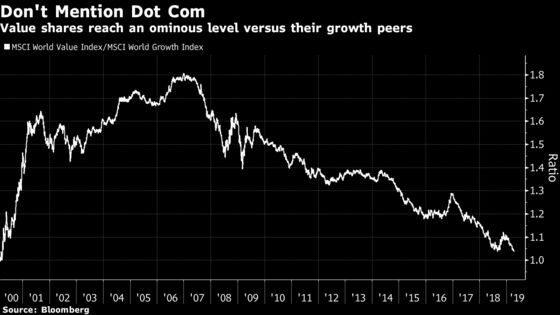

That month was one of the last times the world’s cheapest companies looked this sickly versus their pricey peers.

As of Friday, the MSCI World Value Index was flirting with a 19-year low against its growth counterpart at less than half a basis point from its dot-com nadir. That should be a gut check for equity investors in this unloved rally, bringing with it two questions: How much crowding can growth stocks sustain? And can value shares stay this cheap?

“The issue with value is that it requires a belief in the future,” Markus Rosgen at Citigroup Inc. wrote in a research note on Friday. “The world will grow and in good time value will be realized. Yet that has been missing from investor mindsets. End-is-nigh discussions still dominate.”

Fears for the economic outlook prompted a dovish pivot by the world’s major central banks in the first quarter. Easier monetary policies punish value stocks because the group includes beaten-up industries like banks, which are more sensitive to rates, while a weaker economy makes it less likely cyclical shares like industrials will catch up. The same environment makes firms that can post reliable profits throughout the business cycle even more attractive.

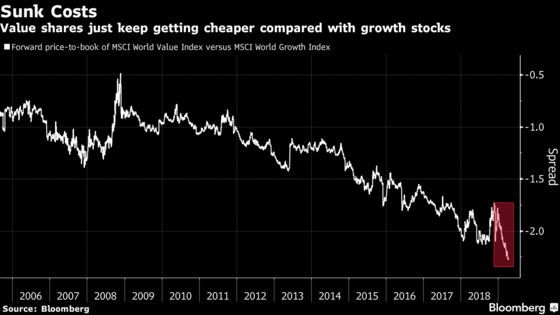

That’s all prompted the surging valuation gap between value and growth stocks. The monetary pivot compounded a long-term trend, of course. Cheap equities have underperformed since the eve of the global financial crisis, as investors relentlessly snubbed less reliable business models.

Rosgen at Citi is among a cohort of sell-side strategists who figure the divergence is extreme and ripe for a tentative reversal. The quantitative strategists at Societe Generale led by Andrew Lapthorne reiterated last week that they see “strong upside potential” for value shares thanks to their attractive relative valuations.

“For value to do well, economic data and earnings revisions need to be improving,” Rosgen wrote. “Here the news is encouraging.”

After a rough few months, the Citi Global Economic Surprise Index is showing signs of a turnaround. Friday’s export and credit data from China beat expectations, raising optimism over trade and the strength of the world’s second-biggest economy. On the earnings front, the number of analyst downgrades in the U.S. has eased as we head into results season. The first two big banks to report, JPMorgan Chase & Co. and Wells Fargo & Co., both beat expectations on Friday.

For Inigo Fraser-Jenkins and his team of quants at Sanford C. Bernstein, a long-term rebound of value stocks isn’t in the cards. But they also see short-term opportunities emerging thanks to their current beaten-up state.

“Can value stocks rally when the yield curve is flat? Not in the long term, but that does not prevent tactical rallies, and we see a case for that,” Fraser-Jenkins said.

The valuation gap flirted with these levels last year, before pulling back during the fourth quarter sell-off.

Tech Boom

Meanwhile, for the doom-mongers out there, other dot-com parallels are on offer. Technology stocks are on the cusp of another record high even as bad news assails the industry, while a frenzy surrounds IPOs in the sector. Loss-making Lyft Inc. raised more than $2 billion last month and shares surged in the first day of trading. They have subsequently slumped after rival Uber Technologies Inc. said it’s joining the party.

Even the dovish Fed tilt harks back to the late 1990s, when rate cuts helped fuel the bubble. Yet, speaking after the central bank’s March meeting, Chairman Jerome Powell brushed off concerns, arguing policy makers are much more attuned to the risks.

”Long-duration growth shares benefit from this environment, but one has to balance that against the multiple that they trade at,” Bernstein strategists wrote.

To contact the reporter on this story: Samuel Potter in London at spotter33@bloomberg.net

To contact the editors responsible for this story: Samuel Potter at spotter33@bloomberg.net, Sid Verma, Cecile Gutscher

©2019 Bloomberg L.P.